Here’s a hard truth: You probably lost money on your last transfer to India. Maybe it was ₹500, maybe it was ₹5,000. But if you relied solely on your bank’s default rate without doing the math, you paid a “convenience tax.”

For Non-Resident Indians (NRIs), sending money home isn’t just a transaction; it’s a lifeline. It’s tuition fees, medical bills for aging parents, or property investments in a booming Indian economy. Yet, in 2026, millions of dollars are still lost annually to opaque exchange rates and hidden spreads.

I’ve spent over a decade analyzing fintech markets and cross-border payments. I’ve seen the backend of how banks price these transfers. The gap between the rate you see on Google and the rate you get in your app is where the game is played.

This isn’t just another generic article. This is your playbook for 2026. We’re going to dismantle the fee structures, show you exactly how to use a forex currency converter to your advantage, and ensure more of your hard-earned currency makes it to the rupee account waiting on the other side.

📑 What You’ll Learn

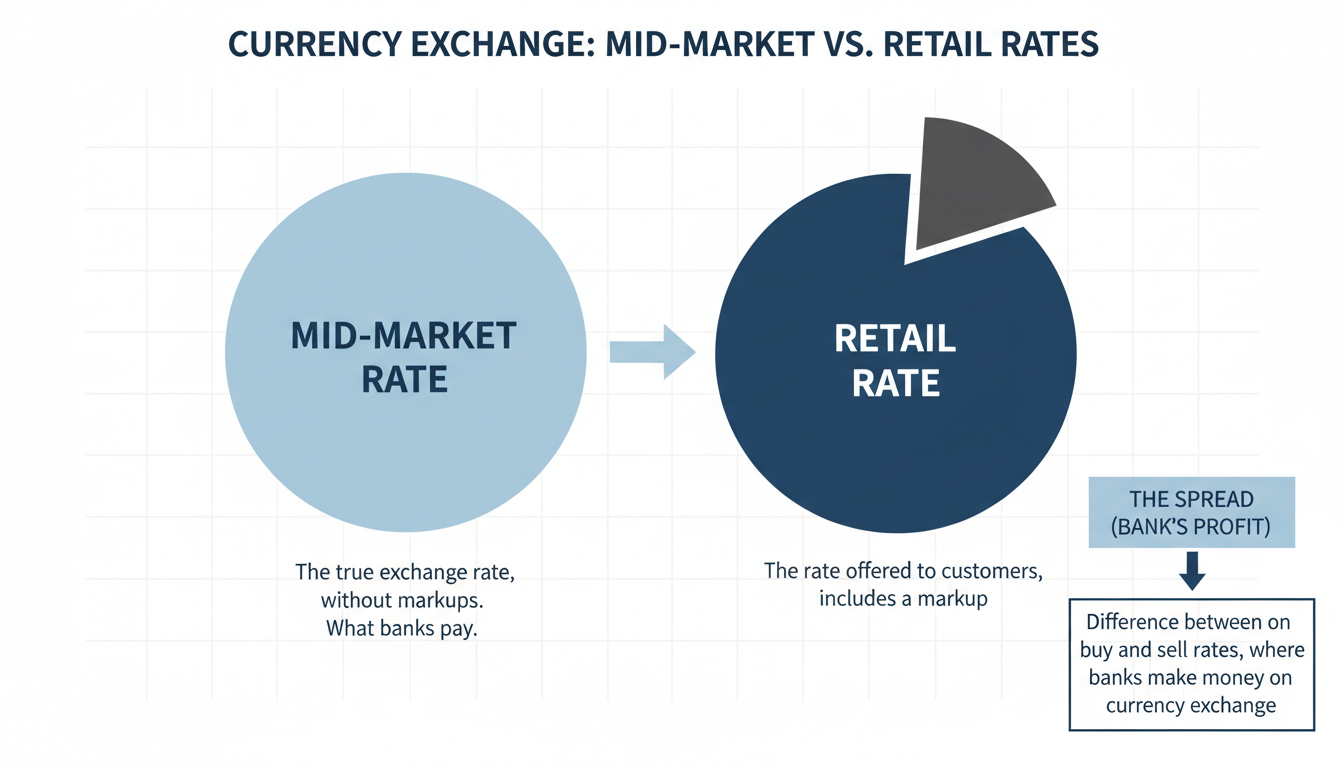

The “Real” Rate vs. The “Retail” Rate

Open a new tab. Search for “USD to INR” (or your local currency). The number you see? That’s the Mid-Market Rate (also known as the interbank rate). It’s the wholesale price banks charge each other when trading millions of dollars instantly.

Here is the thing: You will almost never get this rate.

Unless you are moving millions like a multinational corporation, you are a retail customer. Retail customers get the “Retail Rate.” The difference between the Mid-Market Rate and your Retail Rate is the “Spread.”

In our experience testing dozens of platforms, traditional banks often mark up the exchange rate by 2% to 5%. On a $10,000 transfer, a 3% markup means you just paid $300 in hidden fees, even if the bank advertised “$0 Transfer Fees.”

🎯 Key Takeaway

Never trust a “Zero Fee” claim blindly. If the transfer fee is zero, the profit is hidden in the exchange rate markup. Always compare the offered rate against the live mid-market rate to calculate the true cost.

Decoding the Spread: Where Your Money Goes

To secure the NRI remittance best rates, you have to stop looking at the transaction fee and start looking at the Total Cost of Ownership of the transfer. The formula is simple, yet often ignored:

(Amount Sent × Exchange Rate) – (Transfer Fees) = Amount Received

However, the “Exchange Rate” variable is where 90% of the cost hides. Let’s break down the three layers of cost you face in 2026:

- The Spread (The Invisible Tax): As mentioned, this is the markup. If the USD/INR mid-market rate is 84.00, and your bank offers 82.50, that 1.50 difference per dollar is the spread.

- The Transfer Fee (The Visible Tax): A fixed fee (e.g., $5, £3) or a percentage. Fintech apps are transparent about this; banks often aren’t.

- Correspondent Bank Fees (The Nasty Surprise): If you use the SWIFT network (common with old-school bank transfers), intermediary banks can take a cut while the money is in transit. You might send $1,000, but only $985 arrives because a bank in New York took a handling fee.

⚠️ Watch Out

Avoid “SWIFT” transfers for amounts under $5,000 if possible. They are slow (3-5 days) and prone to unpredictable intermediary fees. Look for providers using “local rail” networks for faster, cheaper settlements.

Comparison: Banks vs. Modern Transfer Apps

The landscape has shifted dramatically. In 2026, specialized Money Transfer Operators (MTOs) and fintechs have largely outpaced traditional banks for standard remittances. But don’t just take my word for it. Let’s look at the data.

Here is a comparison based on a hypothetical transfer of $1,000 to India.

| Feature | Traditional Banks | Modern Fintechs (Wise, Remitly, etc.) | Forex Brokers |

|---|---|---|---|

| Exchange Rate | High Markup (2-5% above mid-market) | Mid-Market or Low Markup (0.5-1.5%) | Negotiable (Best for very large sums) |

| Transfer Speed | 3-5 Business Days | Instant to 24 Hours | 1-2 Days |

| Transparency | Low (Hidden spreads) | High (Breakdown shown upfront) | Medium |

| Convenience | High (Already have an account) | High (App-based) | Medium (Requires account setup) |

| Best For… | Convenience over cost | Regular monthly remittances | Property purchase / Large Cap transfers |

As you can see, for the average NRI sending monthly maintenance or savings, fintech platforms usually win on pure mathematics.

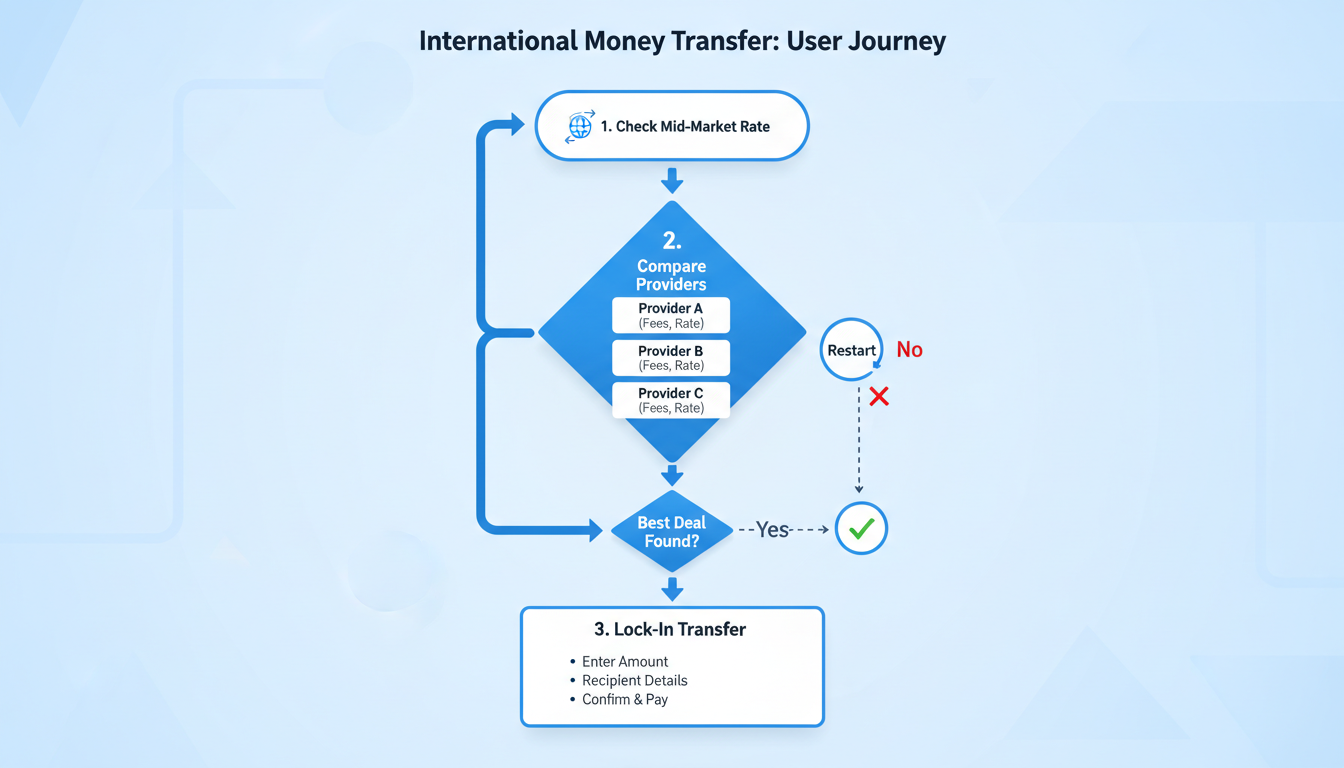

Step-by-Step: How to Get the Best Rate

You don’t need a finance degree to beat the system. You just need a process. Here is the exact workflow I recommend to clients to ensure they are getting the maximum rupee value.

1. Establish the Baseline

Before logging into your bank, go to a neutral currency converter (like Google Finance or XE) to check the live mid-market rate. Write it down. This is your “perfect world” number.

2. The “Two-Tab” Method

Open two remittance providers in separate browser tabs. Enter the exact same amount (e.g., 1,000 USD) into both.

- Tab A: Your traditional bank.

- Tab B: A specialized remittance service.

Ignore the fees for a second. Look strictly at the “Amount Receiver Gets” figure. This is the only number that matters. It accounts for the rate, the spread, and the fees combined.

3. Check for Coupons

Many services offer “First Transfer Free” or enhanced rates for new customers. A quick search for promo codes can save you the transaction fee.

4. Lock It In

Markets move fast. If you see a rate you like, lock it in. Modern apps allow you to lock a rate for 24-48 hours while you fund the transfer.

💡 Pro Tip

Set Rate Alerts. You don’t have to stare at the screen all day. Most apps allow you to set a target rate (e.g., “Notify me when USD/INR hits 84.50”). This lets you automate your timing strategy.

Timing the Market: When to Hit Send

Is there a “best time” to send money? Yes and no. While you can’t predict the future, you can understand volatility.

Currency markets are most volatile when major economic news drops. For the INR, this usually involves:

- RBI Monetary Policy Announcements: Decisions on interest rates in India.

- US Federal Reserve Meetings: Changes in the US dollar strength ripple globally.

- Oil Prices: Since India imports most of its oil, a spike in crude prices often weakens the Rupee.

According to data from Investopedia, market liquidity is highest when the London and New York trading sessions overlap (roughly 8:00 AM to 12:00 PM EST). Transferring during these windows can sometimes yield tighter spreads because the market is more active.

Avoid the Weekend Trap: Currency markets close on weekends. If you initiate a transfer on a Sunday, the provider will likely give you a “weekend rate”—which is usually lower to protect them against any market gaps that might happen when trading opens on Monday. Wait until Monday morning if you can.

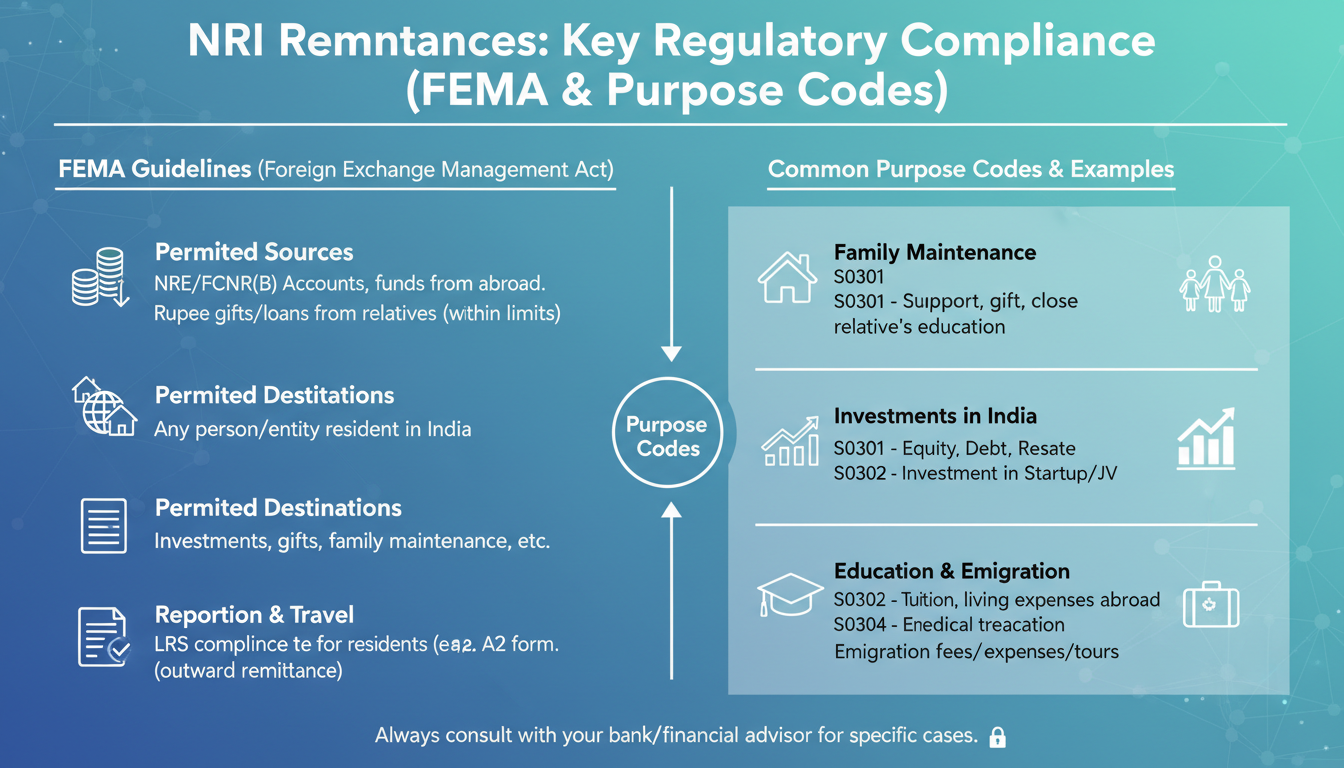

2026 Regulatory Landscape (FEMA & RBI)

Compliance isn’t the most exciting topic, but ignoring it can get your funds frozen. In India, inward remittances are strictly governed by the Foreign Exchange Management Act (FEMA).

As of 2026, here is what you need to keep in mind:

| Regulation | What It Means for You |

|---|---|

| Purpose Codes | You must declare the reason for the transfer (e.g., “Family Maintenance,” “Savings”). Incorrect codes can lead to tax scrutiny. |

| FIRA / FIRC | Foreign Inward Remittance Certificate. Essential if you plan to repatriate this money later. Ensure your bank issues this for large transfers. |

| Tax at Source (TCS) | While inward remittance is generally tax-free for the receiver (if a relative), sending money out of India falls under LRS limits. |

Always ensure you are using an “Authorized Dealer” (AD-I bank) or a fully licensed Money Transfer Operator. Using informal channels (Hawala) is illegal and puts your capital at 100% risk. For the official list of authorized entities, you can check the Reserve Bank of India (RBI) website.

❓ Frequently Asked Questions

Is it better to send money in a single large lump sum or smaller chunks?

Generally, sending a single large sum is cheaper. Many providers charge a fixed fee per transaction. By sending one large amount, you pay that fee once. Additionally, some providers offer “volume discounts” or better exchange rates for transfers over a certain threshold (e.g., $10,000+).

Do I have to pay tax in India on money sent from abroad?

In most cases, no. Under current Indian tax laws, money sent to “relatives” (as defined by the Income Tax Act) for personal use is not considered taxable income for the receiver. However, if the money is invested and generates interest, that interest is taxable.

Why is the rate on Google different from my bank’s rate?

Google displays the “mid-market rate”—the wholesale price banks pay each other. Banks charge retail customers a markup (spread) to make a profit. This is why your transaction rate is always lower than the Google rate.

How long does an NRI remittance take in 2026?

It depends on the method. Digital wallets and fintech apps can process transfers instantly or within a few hours using local payment rails (like UPI in India). Traditional SWIFT wire transfers via banks still take 2-5 business days.

Can I lock in an exchange rate for a future transfer?

Yes, this is called a “Forward Contract.” Many specialized forex brokers allow you to lock in today’s rate for a transfer up to 12 months in the future. This is excellent for managing risk if you are buying property or paying tuition.

Conclusion: Your Money, Your Rules

The days of blindly trusting your bank with your remittance are over. In 2026, you have the tools, the data, and the options to demand a better deal.

Finding the NRI remittance best rates isn’t about luck; it’s about friction. It takes two extra minutes to check a comparison tool, look at the spread, and choose the right provider. But those two minutes can save you hundreds of dollars over the course of a year.

Your next step? Don’t just hit “repeat” on your last transfer. Check the mid-market rate, compare it against your bank, and if the gap is too wide, switch providers. Your wallet will thank you.

For more global economic trends affecting currency, refer to the World Bank’s Financial Sector reports.