Ever seen a transaction fail and wondered why? Sometimes, it’s a simple typo. But often, it’s a bug that could have been caught. And here’s the secret: the tool developers use to catch those bugs is, ironically, a “fake” credit card number.

The phrase ‘targeta de credito falsa generar’ sounds like something from the dark web, but it’s one of the most misunderstood—and essential—tools in modern software development. It’s the key to building the secure, seamless e-commerce experiences we all depend on.

Forget the myths. This isn’t about fraud. It’s about precision engineering.

In this deep dive, you’ll learn exactly what these tools are, how the underlying technology works, and the crystal-clear line between legitimate, essential testing and serious, life-altering crime. We’ll give you the playbook for using them responsibly and show you why trying to cheat the system is a fool’s errand. Let’s get started.

📑 What You’ll Learn

The Developer’s Dilemma: Why ‘Fake’ Credit Cards Are Essential

Imagine you’re building a brand-new online store. You need to test the checkout process. Not once, not twice, but thousands of times. Do you use your personal Amex? Your company card? Of course not. That would be a security nightmare and a logistical mess, triggering fraud alerts and creating a mountain of refunds.

This is the problem that credit card generators solve. They don’t create counterfeit credit cards. They create mathematically valid strings of numbers that look and feel like real card numbers to a web form but are completely disconnected from any financial institution.

Think of it like a crash test dummy. It has the shape and weight of a person, allowing engineers to test safety systems without putting a real human at risk. In the same way, a generated card number lets a developer test a payment system without touching real money.

From our experience building and scaling e-commerce platforms, these tools are non-negotiable for:

- E-commerce Sanity Checks: Simulating thousands of transactions to ensure the payment flow—from cart to confirmation—is flawless.

- Payment Gateway Integration: Making sure your site communicates perfectly with services like Stripe, PayPal, or Adyen before a single real customer arrives.

- Form Validation & UX Testing: Confirming that the system correctly identifies a Visa from a Mastercard, flags an incorrectly typed number, and provides helpful error messages to the user.

💡 Pro Tip

Major payment gateways like Stripe provide their own sets of test card numbers designed to trigger specific responses. For example, one number will always process successfully, another will always be declined for “insufficient funds,” and another will trigger a CVC error. Using these official test cards is the gold standard for testing specific gateway integrations.

Under the Hood: The Tech Behind Test Card Numbers

So, what makes these numbers “work” for testing but fail for actual purchases? It’s all about passing the first, most basic check, but failing all the important ones that follow. The magic is in an algorithm that’s been around since the 1950s.

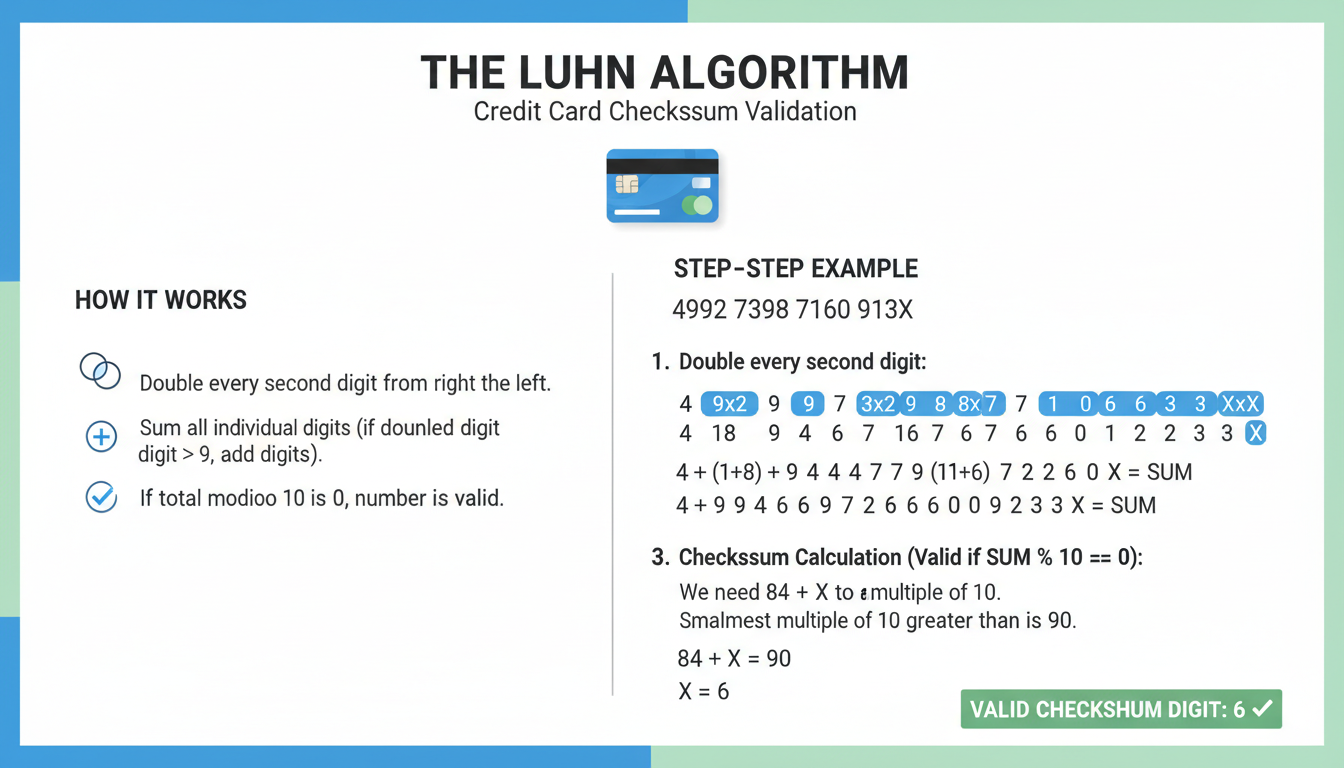

The Luhn Algorithm: The Gatekeeper’s First Question

At the heart of every generated card number is the Luhn algorithm, also known as the Modulo 10 or Mod-10 algorithm. It’s a simple checksum formula used to validate identification numbers. It doesn’t prove a card is real; it only proves the number sequence isn’t gibberish.

Here’s the gist:

- It takes the digits of the card number.

- It performs a series of multiplications and additions.

- If the final sum is perfectly divisible by 10, the number is considered “valid” by the algorithm.

A ‘targeta de credito falsa generar’ tool simply creates a number that is guaranteed to pass this initial check. This is crucial for front-end validation—the kind that happens in your browser before anything is even sent to the server. It weeds out simple typos instantly.

The Anatomy of a Test Number

A generated number isn’t random. It’s built just like a real one:

- Issuer Identification Number (IIN): The first 6-8 digits. This prefix identifies the card network. For example, Visa cards start with a 4, Mastercard with a 51-55, and American Express with a 34 or 37. Generators use these real prefixes to create realistic numbers.

- Account Identifier: The middle digits that would normally link to your specific account.

- Check Digit: The final digit, calculated using the Luhn algorithm to make the whole sequence valid.

But here’s the real kicker. This is where the road forks. A generated number has none of the things required for a real transaction: no valid expiration date, no correct CVV code, no cardholder name, and—most importantly—no link to a real bank account with actual funds. When the payment request hits the real banking network, it’s an instant dead end.

The Bright Line: Legitimate Use vs. Felony Fraud

Let’s be blunt. The line between using these tools ethically and committing a crime is not blurry. It’s a razor-sharp, uncrossable boundary. Using a generated number in a sandboxed, internal development environment is a standard industry practice. Attempting to use one to obtain goods or services is fraud.

The consequences are not a slap on the wrist. They are severe and can include hefty fines, prison time, and a permanent criminal record that can derail your life. According to legal frameworks like the U.S. Code on wire fraud, the mere attempt to use deceptive means over electronic communications to obtain something of value can be a federal crime.

| Scenario | Intent & Environment | Legality & Outcome |

|---|---|---|

| ✅ Legitimate Use | A developer enters a generated Visa number into their own e-commerce site running on a local test server to see if the payment form validates the input correctly. | Perfectly Legal. This is the intended purpose. The test is isolated, no real transaction is attempted, and it improves software quality. |

| ❌ Illegal Misuse | A person generates a Mastercard number and tries to use it on a live retail website to buy a new pair of headphones. | Illegal (Fraud). This is a criminal act. The transaction will be instantly declined by the payment gateway, and the attempt will be logged with the user’s IP address and other identifiers. |

⚠️ Watch Out

The myth of online anonymity is just that—a myth. Modern fraud detection systems, employed by every major retailer and payment processor, use sophisticated AI to track behavior. Repeated failed payment attempts from the same IP address, device fingerprint, or email address will get you flagged and blacklisted instantly. Law enforcement has extensive tools to trace digital activities back to their source.

Why Fraudulent Attempts Are Doomed to Fail

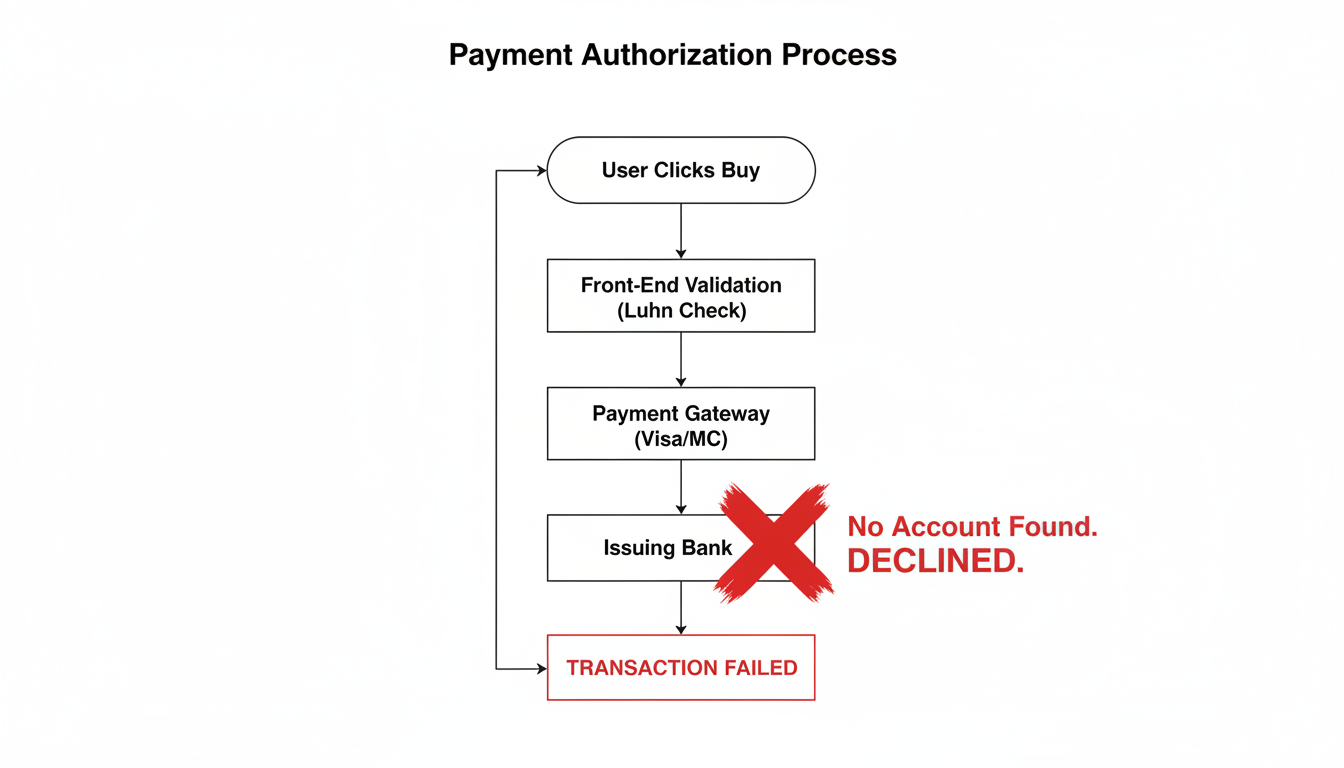

Even if you ignore the ethics and the law, trying to use a generated number for a real purchase is technically futile. The modern payment authorization process is a multi-layered fortress.

When you hit “buy,” your request goes on a journey:

- Gateway Check: The payment gateway (like Stripe) receives the data.

- Network Verification: The gateway sends the request to the card network (like Visa or Mastercard).

- The Bank’s Verdict: The network asks the issuing bank, “Does this account exist, does it have funds, and do the CVV and expiration date match?”

A generated number fails at step 3. Spectacularly. There is no issuing bank. There is no account. The request hits a brick wall, and the transaction is declined in milliseconds.

A Step-by-Step Guide to Safe Checkout Testing

For developers and QA testers, using these numbers responsibly is a mark of professionalism. Based on hands-on testing from our own dev teams, here’s a simple, safe workflow.

- Isolate Your Environment: Never test on your live, production website. Always work in a dedicated “staging” or “development” environment. This is a clone of your site that is not accessible to the public and is not connected to real payment processing.

- Use Test API Keys: Your payment gateway provides two sets of API keys: “live” and “test” (or “sandbox”). Ensure your testing environment is configured only with the test keys. This guarantees no real transactions can ever be processed.

- Source Your Test Data: Whenever possible, use the official test card numbers provided by your payment gateway. These are designed to work perfectly on their platform and can simulate various scenarios. If you need to test form validation for different card formats, a reputable online generator is fine.

- Execute the Test: Run through your entire user flow. Add an item to the cart, proceed to checkout, and enter the test card number. Verify that the system behaves as expected (e.g., accepts a valid format, rejects an invalid one).

- Verify the Outcome: Check your payment gateway’s test dashboard. You should see a record of the successful or failed test transaction. This confirms your integration is working without ever touching a real bank network.

⚠️ Watch Out

A surprisingly common and catastrophic mistake is accidentally using “live” API keys in a development or staging environment. This can lead to real credit cards being charged during testing or, worse, exposing your live payment credentials in an insecure setting. Always double-check your environment variables.

🎯 Key Takeaway

The term ‘targeta de credito falsa generar’ refers to a critical developer tool for creating mathematically valid but financially inert card numbers for software testing. Its use is essential for building secure e-commerce systems. However, attempting to use these numbers for real purchases is a futile and serious crime with severe consequences.

❓ Frequently Asked Questions

Is it illegal to generate a fake credit card number?

No. The act of generating a number using a tool is not illegal. It’s a standard practice for software testing. The illegality comes from the intent and action of using that number to commit fraud—that is, trying to deceive someone to obtain goods or services without payment.

Can a generated credit card number actually buy anything in 2026?

Absolutely not. A generated number will fail 100% of the time when used for a real transaction. It lacks a valid expiration date, CVV, and, most importantly, is not linked to any real bank account. The multi-step authorization process used by all modern payment networks will instantly decline it.

What is the Luhn algorithm’s main purpose?

The Luhn algorithm is a simple checksum formula used as a first-pass sanity check on an identification number. Its primary purpose in payment forms is to catch accidental typos (like transposing two digits) immediately, right in the browser, before the data is even sent for processing. It cannot and does not verify if a card is real or has funds.

Who should be using these generator tools?

These tools are built for a specific professional audience: software developers, quality assurance (QA) engineers, cybersecurity researchers, and educators. They use them to test payment systems, validate input forms, and teach about data validation in a safe, controlled manner without exposing sensitive financial data.

Where can I find official test card numbers?

Nearly all major payment processors provide them. For example, Stripe’s documentation offers a comprehensive list of numbers that trigger different responses. The PCI Security Standards Council also provides guidance on securing payment data, which is a foundational concept for anyone working in this space.

What’s the difference between a test number and a stolen card number?

They are completely different. A test number is a mathematically constructed sequence with no real-world value, created for testing. A stolen card number is real, active financial data belonging to a real person, obtained illegally. Using stolen card numbers is a serious crime that directly harms individuals.

Final Thoughts: A Tool for Builders, Not Breakers

In the end, a ‘targeta de credito falsa generar’ tool is like a master key for a locksmith in training. In the right hands, it’s used to understand how locks work, how to build better ones, and how to test them for weaknesses. In the wrong hands, the intent is malicious, and the consequences are severe.

For the developers, testers, and builders out there, these tools are an indispensable part of your kit. Use them wisely, use them ethically, and continue building the secure and reliable digital world we all rely on.

Your next step? If you’re a developer, review your project’s testing protocols. Ensure you’re using dedicated test keys and isolated environments. It’s a simple check that upholds the integrity of your work and the security of your future customers.