Here’s a terrifying statistic: On a typical 20-year home loan in India, you might end up paying the bank more in interest than the actual cost of the house itself.

Let that sink in. You buy a house for ₹50 Lakhs, but by the time you’re done in 2046, you’ve paid the bank ₹90 Lakhs or more.

Most borrowers sign the dotted line, look at the monthly figure, and think, “I can afford this.” But they rarely look under the hood. In my experience working with financial planning strategies, the borrowers who understand the math are the ones who get out of debt five, sometimes ten years early.

If you are planning to buy property in 2026, knowing how to calculate home loan emi india isn’t just a math problem—it’s a survival skill. It gives you the leverage to negotiate, the foresight to plan prepayments, and the clarity to avoid the “interest trap.”

In this guide, we’re ditching the jargon. I’m going to show you exactly how the formula works, how to do it in Excel (because who uses a calculator anymore?), and the insider tricks banks don’t usually advertise.

📑 What You’ll Learn

The “Interest Trap”: Why You Must Calculate It Yourself

You might be thinking, “Why bother? There are a million online calculators.”

You’re right. But here’s the thing: online calculators are sales tools. They are designed to show you the lowest possible number to get you to click “Apply.” They often default to the longest tenure (30 years) to make the monthly payment look tiny, hiding the massive interest burden.

When you understand the mechanics of the Equated Monthly Installment (EMI), you understand the Amortization Schedule. This is the roadmap of your loan. In the first few years, a shocking percentage of your money—sometimes up to 80%—goes purely toward interest. You barely touch the principal.

🎯 Key Takeaway

Your EMI is composed of Principal + Interest. However, the ratio changes every month. In the early years, you are mostly paying interest. Understanding this calculation helps you realize why making prepayments early in the loan tenure is the secret to saving lakhs.

The Big Three: P, R, and N Explained

Before we plug numbers into a formula, we need to clean up the data. If you get one of these wrong, your calculation will be off by thousands of rupees. Trust me, I’ve seen people panic because they used the annual rate instead of the monthly rate.

Here is the breakdown of the variables used in the Indian banking system:

- P (Principal): The loan amount you are borrowing. (e.g., ₹50,00,000).

- R (Rate of Interest): This is the tricky one. Banks give you an Annual rate (like 8.5%). The formula needs a Monthly rate.

- N (Tenure): The duration of the loan in Months, not years.

⚠️ Watch Out

The “R” Mistake: Never use the annual percentage directly in the formula. You must divide the annual rate by 12 and then divide by 100. For example, if the rate is 9% p.a., your ‘R’ is not 9. It is (9/12)/100 = 0.0075.

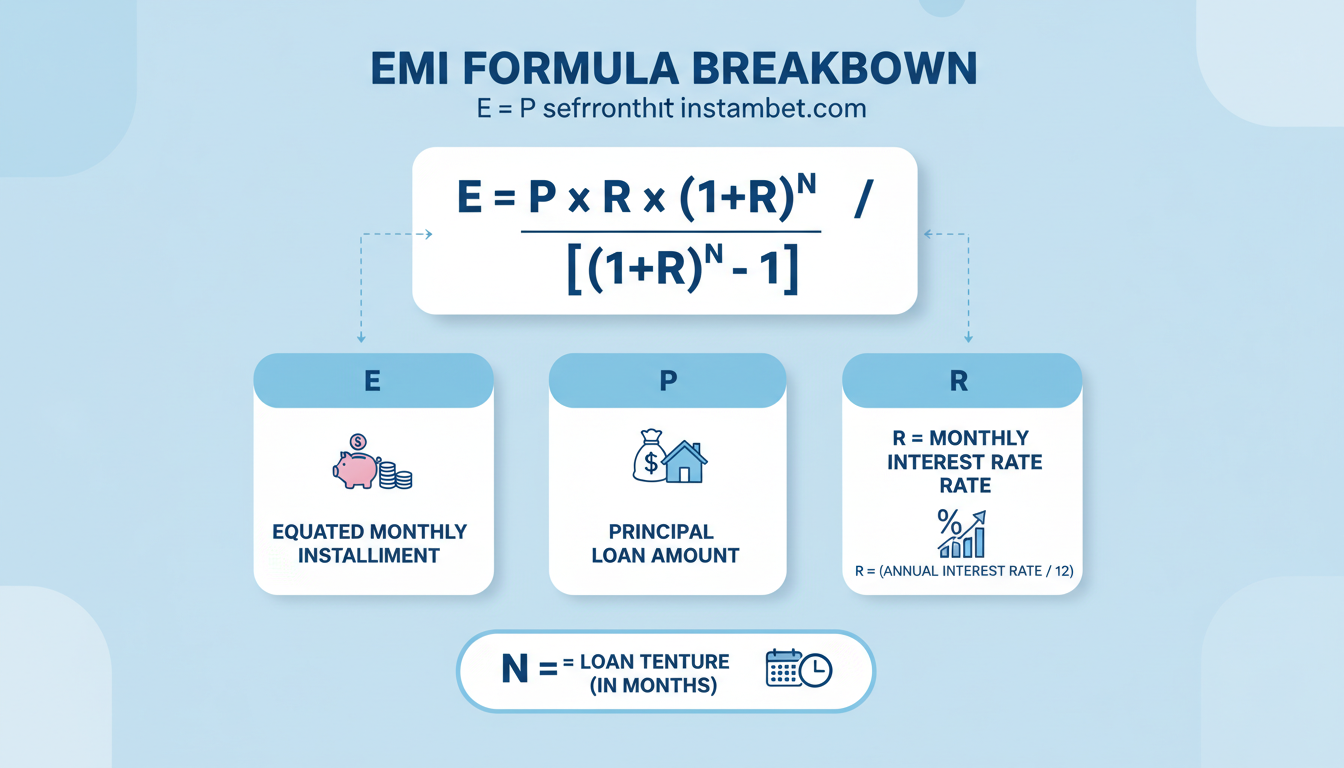

The Manual Formula: How to Calculate Home Loan EMI India

Okay, let’s get technical. This is the standard formula used by the Reserve Bank of India (RBI) and all major lenders. It uses the “reducing balance” method.

The Formula:

E = P x R x (1+R)^N / [(1+R)^N - 1]

It looks like high school algebra nightmares, right? Let’s break it down with a real-world scenario.

with color-coded arrows explaining each variable]

Step-by-Step Calculation Example

Let’s say you are buying an apartment in Bangalore.

- Loan Amount (P): ₹40,00,000

- Interest Rate: 8.5% per annum

- Tenure: 15 Years

Step 1: Convert the Rate (R)

8.5% divided by 12 months = 0.7083%.

Convert to decimal: 0.7083 / 100 = 0.007083.

Step 2: Convert the Tenure (N)

15 years x 12 months = 180 months.

Step 3: Calculate the Power Factor (1+R)^N

(1 + 0.007083) ^ 180 = 3.56 (approx).

Step 4: The Final Crunch

Numerator: 40,00,000 x 0.007083 x 3.56 = 1,00,865

Denominator: 3.56 – 1 = 2.56

EMI = 1,00,865 / 2.56 = ₹39,399

So, your monthly outflow is roughly ₹39,400.

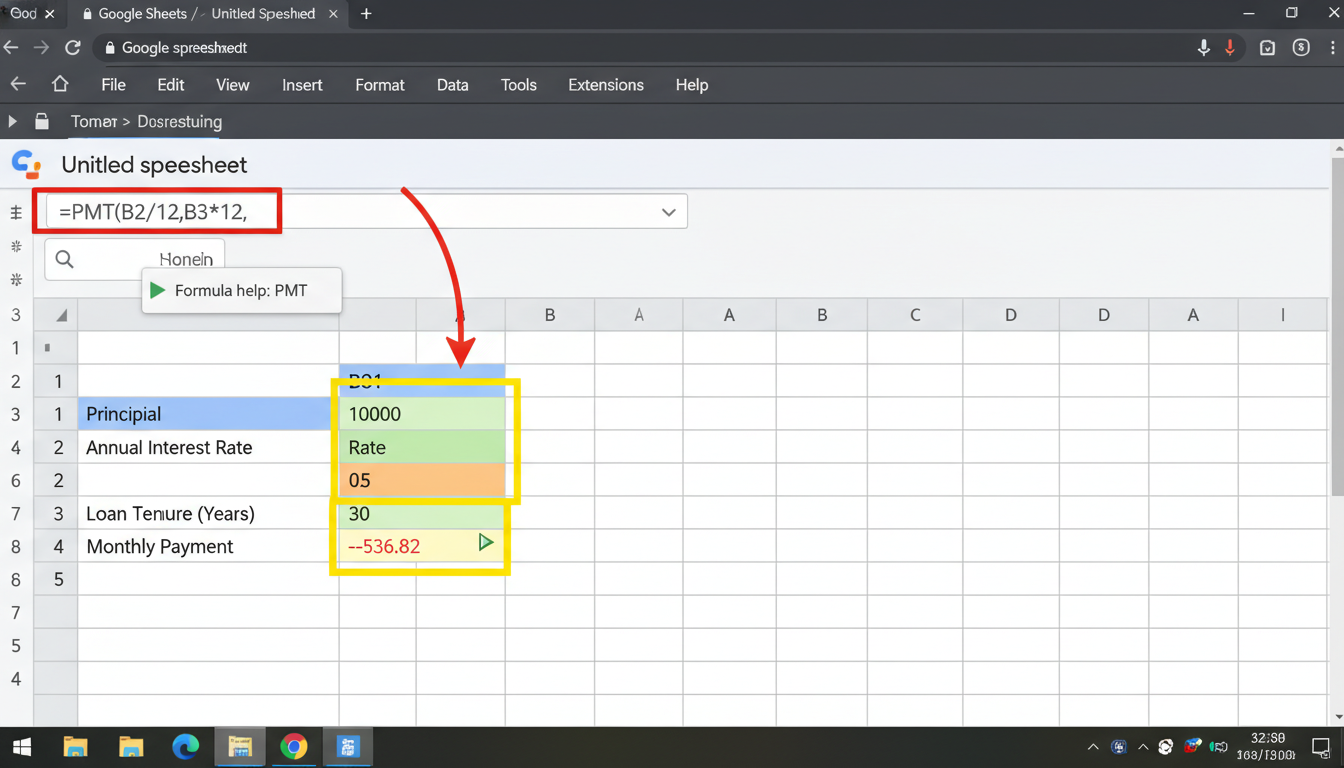

The Easy Way: Using Excel or Google Sheets

Let’s be honest—nobody does the above math on a napkin in 2026. If you have access to Microsoft Excel or Google Sheets, you can do this in 10 seconds. This is how financial analysts actually do it.

We use the PMT function. It stands for “Payment.”

💡 Pro Tip

Open a new Google Sheet and type this formula:

=PMT(rate/12, nper, pv)

Where:

rate = Annual Interest Rate (e.g., 8.5%)

nper = Total months (e.g., 180)

pv = Loan amount (e.g., 4000000)

Note: The result will be negative because it represents money leaving your pocket.

Comparison: Short vs. Long Tenure

This is where the rubber meets the road. When you ask a bank agent how to calculate home loan emi india, they will often push for a longer tenure. Why? Because it lowers your monthly commitment, making you feel richer.

But look at the cost. Here is a comparison for a ₹50 Lakh Loan at 9% Interest.

| Scenario | Tenure (Years) | Monthly EMI (₹) | Total Interest Paid (₹) | Total Cost of Loan (₹) |

|---|---|---|---|---|

| The “Comfortable” Option | 25 Years | ₹41,960 | ₹75,88,000 | ₹1.25 Crores |

| The “Aggressive” Option | 15 Years | ₹50,713 | ₹41,28,000 | ₹91.28 Lakhs |

| The Difference | 10 Years Saved | +₹8,753/mo | Saved ₹34.6 Lakhs | Saved ₹34.6 Lakhs |

Analyze the data: By paying just ₹8,700 more per month, you save nearly ₹35 Lakhs in the long run. That is the price of a brand-new luxury car or a fund for your child’s education.

Strategies to Slash Your EMI Burden

Now that you know the math, how do you beat the system? Based on current market trends in 2026, here are three strategies to keep your EMI low and your savings high.

1. The “Step-Up” Prepayment Method

You don’t need a lump sum to prepay. Simply increase your EMI voluntarily every year. If you get a 10% salary hike, increase your EMI by 5%. This small habit drastically reduces the ‘N’ (Tenure) variable in our formula.

2. Shop for the “Spread”

Interest rates in India are usually the Repo Rate + a “Spread” (margin). While the Repo Rate is decided by the RBI, the spread is decided by the bank. Negotiate the spread. A difference of 0.25% might seem small, but on a 20-year loan, it’s a fortune.

3. Use a Balance Transfer Calculator

If your current rate is 9.5% and another lender offers 8.5%, should you switch? Use the formula to calculate your new EMI. If the savings cover the processing fees (usually 0.5% of the loan) within 12 months, make the switch. You can read more about how amortization works on educational sites like Investopedia.

❓ Frequently Asked Questions

Does the EMI formula change for fixed vs. floating rates?

No, the mathematical formula remains exactly the same. However, with a floating rate loan, the ‘R’ (Rate) variable changes whenever the RBI adjusts the Repo Rate. This means your bank will either increase your EMI amount or, more commonly, extend your loan tenure.

Why is my EMI interest component so high in the beginning?

This is due to the “reducing balance” method. In month one, you owe the full principal, so interest is calculated on the whole amount. As you pay down the principal, the interest portion shrinks. This is why prepaying early in the loan tenure is 10x more effective than prepaying in the last few years.

Can I calculate EMI manually without a scientific calculator?

It is very difficult because of the exponential power function (1+R)^N. For a 20-year loan, you have to multiply a number by itself 240 times. It is highly recommended to use Excel, Google Sheets, or a specialized financial calculator app.

What happens if I miss one EMI payment?

Missing a payment attracts a late fee and penal interest (often 24% p.a. on the overdue amount). More importantly, it impacts your credit score. According to CIBIL, payment history is a significant factor in your creditworthiness, affecting your ability to get future loans.

Conclusion: Take Control of Your Debt

Learning how to calculate home loan emi india is about more than just numbers; it’s about financial freedom. The bank’s system is designed to keep you in debt for as long as possible. Your goal is to use the math to get out as fast as possible.

Start by running your numbers through the Excel formula I shared. Check how much interest you are really paying. Then, look at your budget. Can you afford to increase that EMI by even ₹2,000? If the answer is yes, do it today. Your future self in 2035 will thank you.

Read Also:

- Collage Hacks for Viral Visuals in 2026

- Text to Handwriting in 2026: The Ultimate AI & Font Guide

- Your 2026 Brand Naming Secret Weapon

- Stop Guessing: Your 2026 Torque Secrets

- Biological Age Test: What’s Your Real Age? (2026 Guide)

- Translate to Anglo-Saxon: An Expert’s Guide for 2026 – Visual Story

- How to Download from Hurawatch in 2026 (3 Methods & Risks)

- How to Change Case in Word: The Ultimate 2026 Guide

- Word’s Case Change Secret 2026

- Habit Trackers: Your 2026 Goal Crusher

- QR Code Generator: Boost Business Growth in 2024 – Visual Story