Here’s a scary thought: You might be voluntarily handing over ₹50,000 or more to the government this year simply because you ticked the wrong box on your tax declaration form.

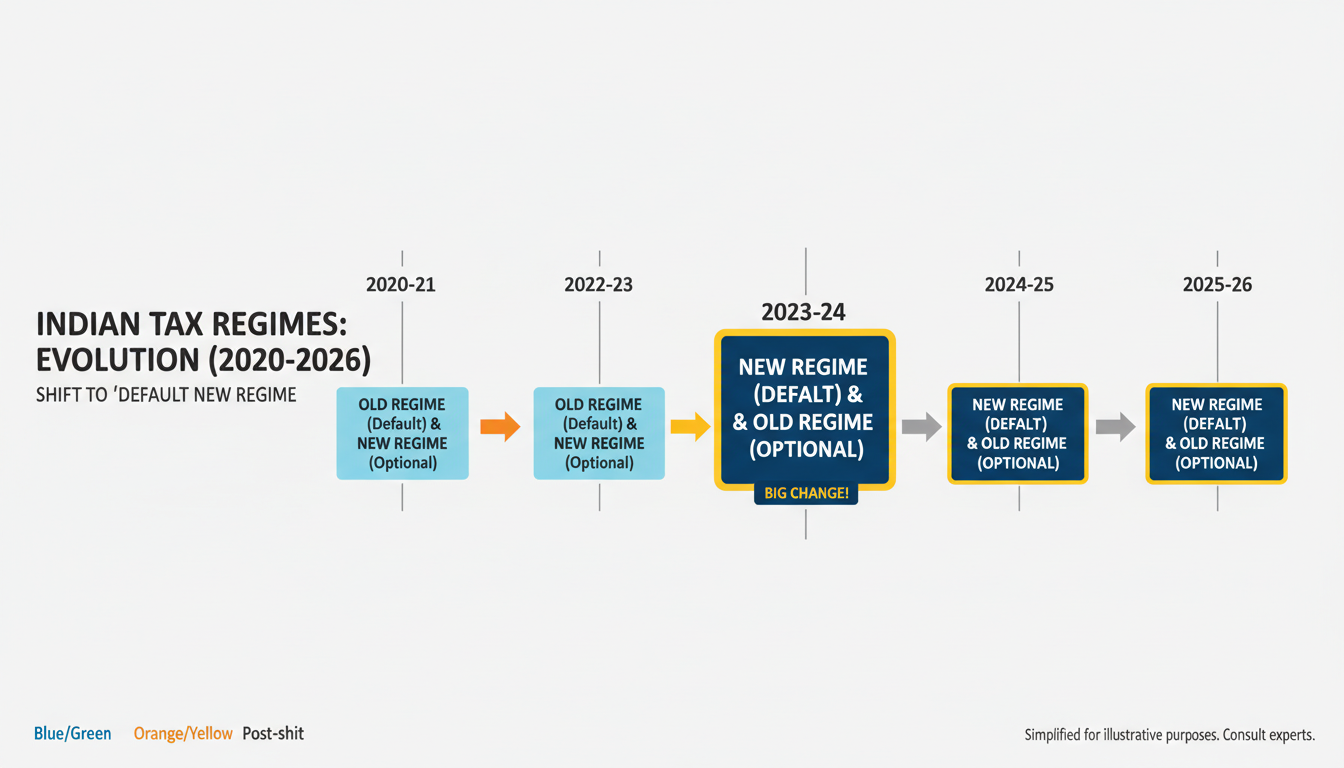

It happens more often than you think. Since the government made the New Tax Regime the “default” option, millions of Indian taxpayers have sleepwalked into a tax structure that might not actually benefit them. On the flip side, stubborn loyalists to the Old Regime are often clinging to deductions that no longer move the needle enough to beat the slashed rates of the new system.

So, which one wins in 2026? The answer isn’t a simple “yes” or “no.” It’s a math problem.

In this deep dive, we aren’t just going to list tax slabs. We’re going to show you exactly how to use an income tax calculator new regime vs old regime to find your personal “break-even” point—the magic number where switching regimes saves you hard-earned cash.

📑 What You’ll Learn

The 2026 Tax Landscape: What Changed?

Let’s set the stage. As we navigate FY 2026-27, the government’s push toward the New Regime has become aggressive. The goal? A simplified tax code with zero exemptions. To sweeten the deal, they have widened the slabs and increased the basic exemption limits significantly over the last few budgets.

However, the Old Regime hasn’t been abolished. It’s still there, lurking in the background, acting as a safe harbor for those with heavy financial commitments like home loans and insurance policies.

Here is the reality: If you do nothing, your employer will automatically calculate your TDS based on the New Regime. If you want the Old Regime, you have to explicitly ask for it. This “opt-out” mechanism is where many people mess up.

New vs. Old: The Core Differences

Think of the Old Regime as a “coupon clipper” system. You pay higher headline rates, but you get to use coupons (deductions) to lower the bill. The New Regime is the “everyday low price” model—lower rates, but no coupons allowed.

To make an informed choice using an income tax calculator new regime vs old regime, you need to know what you’re gaining and what you’re giving up.

| Feature | New Regime (2026 Default) | Old Regime (Traditional) |

|---|---|---|

| Tax Rates | Lower, spread across more slabs. | Higher, fewer slabs. |

| Section 80C (PPF, LIC) | ❌ Not Available | ✅ Up to ₹1.5 Lakh |

| HRA Exemption | ❌ Not Available | ✅ Available |

| Home Loan Interest (Sec 24) | ❌ Not Available | ✅ Up to ₹2 Lakh (Self-occupied) |

| Standard Deduction | ✅ Available (₹75,000) | ✅ Available (₹50,000) |

| 80D (Health Insurance) | ❌ Not Available | ✅ Available |

🎯 Key Takeaway

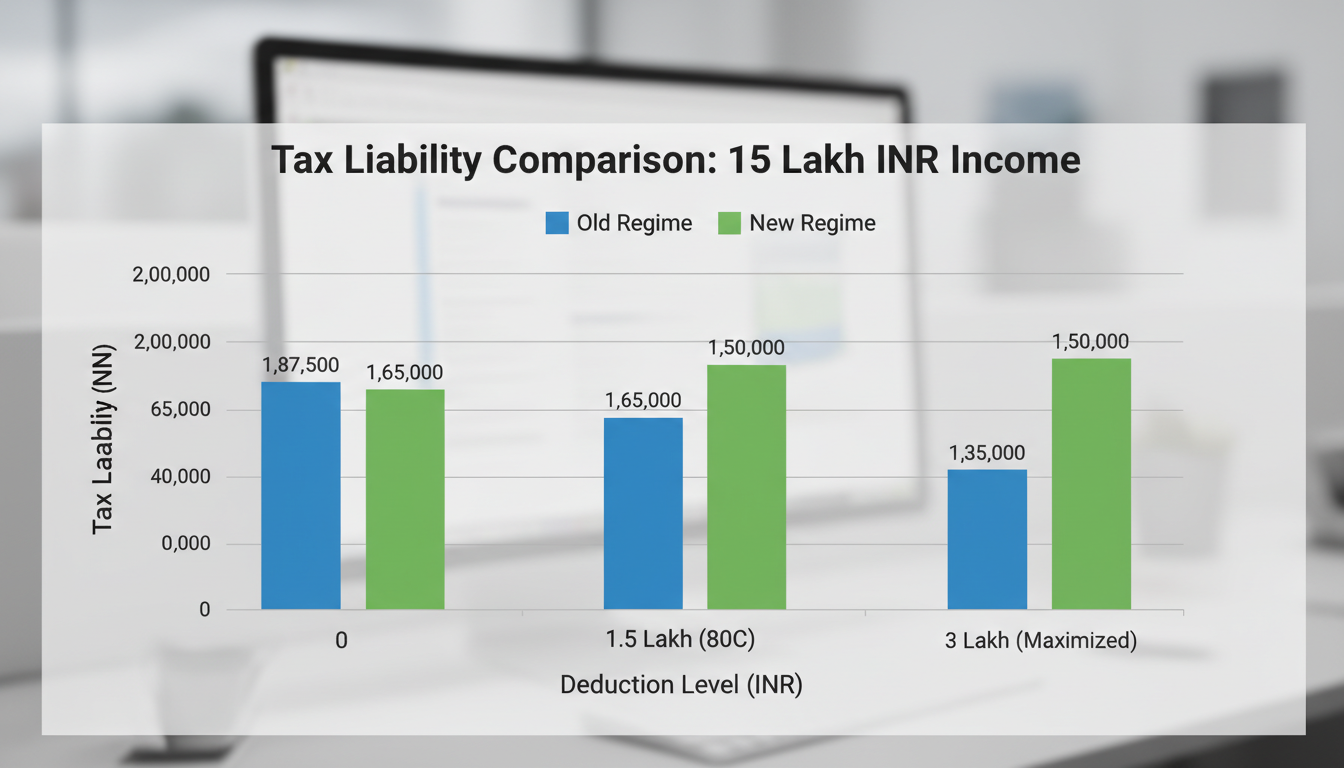

The New Regime is generally better for incomes up to ₹7.5 Lakh due to the rebate. However, once you cross ₹10-15 Lakh, the Old Regime often fights back if you have a home loan and maximize your 80C investments.

The Break-Even Analysis: When to Switch

This is the most critical part of your tax planning. You don’t need to guess; you need to find your “Break-Even Point.”

The break-even point is the exact amount of deductions you need to claim under the Old Regime to pay the same tax as the New Regime.

- If your actual deductions are higher than the break-even point → Choose Old Regime.

- If your actual deductions are lower than the break-even point → Choose New Regime.

In our experience analyzing hundreds of tax files, here is a rough estimation of break-even points for FY 2026-27:

| Gross Income | Approx. Break-Even Deduction Amount |

|---|---|

| ₹10,00,000 | ₹2,50,000 |

| ₹12,50,000 | ₹3,12,500 |

| ₹15,00,000 | ₹3,75,000 |

| ₹20,00,000 | ₹4,00,000+ |

Look at the table above. If you earn ₹15 Lakhs, you need to find ₹3.75 Lakhs worth of deductions to make the Old Regime worth it. That usually means maxing out your 80C (₹1.5L), having a hefty Home Loan interest (₹2L), and throwing in some medical insurance (80D). If you are renting and don’t have a home loan, hitting that ₹3.75L figure is incredibly difficult.

💡 Pro Tip

Don’t forget Section 80CCD(1B). This allows an additional ₹50,000 deduction for contributions to the National Pension System (NPS) over and above the ₹1.5 Lakh 80C limit. This is often the “tie-breaker” that makes the Old Regime viable for high earners.

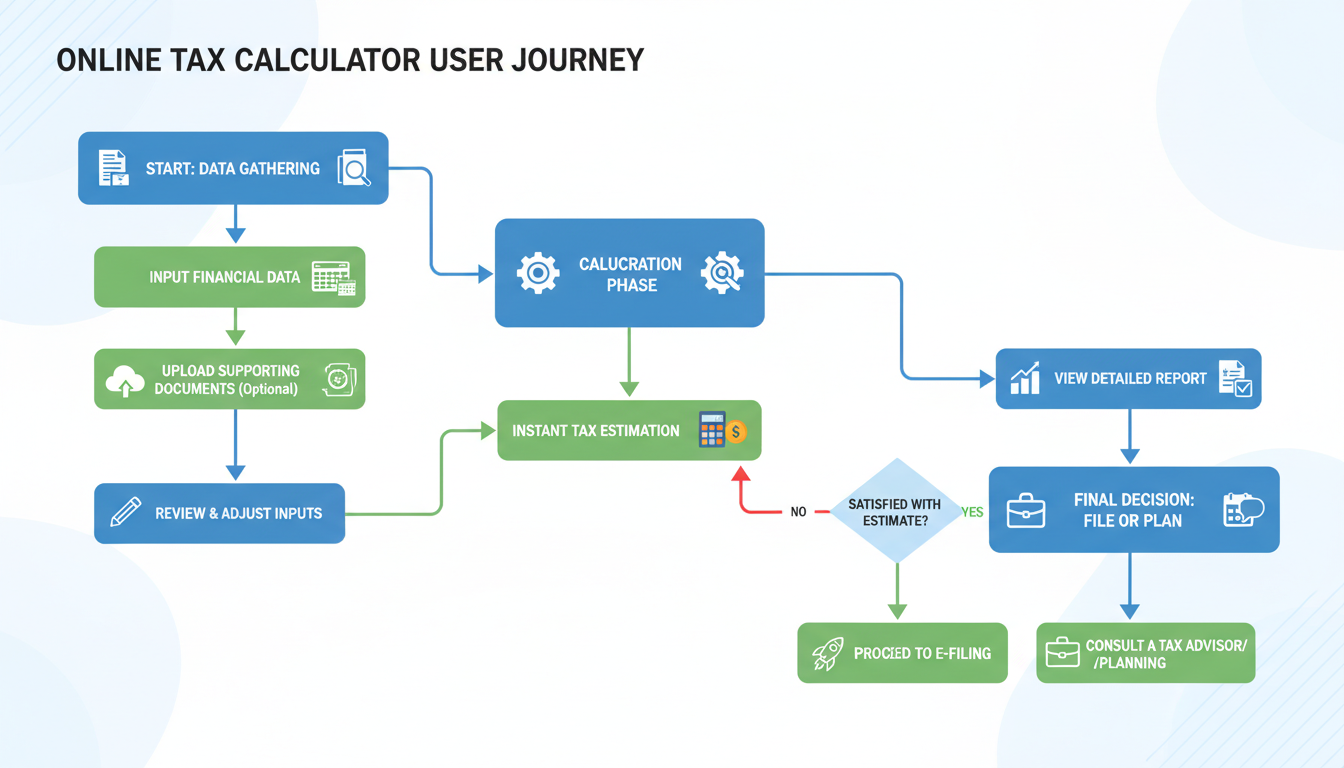

Step-by-Step: How to Use the Calculator Effectively

Using an online tool is easy, but garbage in equals garbage out. Follow this workflow to ensure your income tax calculator new regime vs old regime results are accurate.

Step 1: Gather Your “Income from Other Sources”

Most people just put in their salary. Big mistake. You must include interest from savings accounts (yes, it’s taxable), fixed deposit interest, and any freelance income. According to the Income Tax Department of India, under-reporting interest income is a leading cause of automated tax notices.

Step 2: Calculate Your HRA Correctly

Don’t just input your actual rent paid. The HRA exemption is the lowest of three values:

- Actual HRA received.

- 50% of salary (metro) or 40% (non-metro).

- Rent paid minus 10% of salary.

You need to calculate this figure before entering it into the “Exemptions” field of the calculator.

Step 3: Run the Comparison

Input your Gross Salary. Then, in the deduction section, enter zero first to see the New Regime liability. Then, enter your 80C, 80D, and 24(b) amounts to see the Old Regime liability.

⚠️ Watch Out

The Surcharge Trap: If your income exceeds ₹50 Lakhs, the surcharge rates differ between regimes. The New Regime has capped the surcharge at 25% for super-high earners (above ₹5 Cr), while the Old Regime surcharge can go up to 37%. If you are a high-net-worth individual (HNI), the New Regime often wins by default due to this massive surcharge relief.

Real-World Scenarios: Who Wins?

Let’s look at two common profiles we see in 2026.

Scenario A: The “Renter” (Arjun, Age 28)

- Income: ₹12,00,000

- Investments: ₹1.5 Lakh in EPF/PPF (80C).

- Rent: Pays ₹15,000/month.

- Loans: None.

Verdict: The New Regime likely wins. Even with his 80C and HRA, his total deductions won’t cross the break-even threshold. The lower slab rates of the New Regime will leave him with more cash in hand.

Scenario B: The “Homeowner” (Priya, Age 42)

- Income: ₹18,00,000

- Investments: Maxed out 80C (₹1.5 Lakh).

- Home Loan: Pays ₹2.5 Lakh interest (claims max ₹2 Lakh).

- Health Insurance: Pays ₹30,000 for family (80D).

- NPS: Contributes ₹50,000 (80CCD(1B)).

Verdict: The Old Regime is the clear winner. Priya has stacked her deductions (Total: ₹4.3 Lakh+). This massive reduction in taxable income beats the lower rates of the New Regime. She saves roughly ₹15,000-₹20,000 by sticking to the Old Regime.

For a broader understanding of financial planning beyond just taxes, resources like Investopedia offer excellent guides on how tax planning fits into your overall wealth strategy.

Conclusion

The days of a “one-size-fits-all” tax strategy are dead. In 2026, the choice between the New and Old Regime is strictly a numbers game. The government wants you in the New Regime, and for many—especially those without home loans—it is genuinely the better option. But for the disciplined investor with a mortgage, the Old Regime is still a goldmine of savings.

Don’t guess. Don’t just do what your colleague is doing. Open an income tax calculator new regime vs old regime right now, input your latest salary slip figures, and check the bottom line. It takes five minutes, and it could save you the cost of a new iPhone.

❓ Frequently Asked Questions

Can I switch between regimes every year?

If you are a salaried employee, yes! You can choose the New Regime one year and the Old Regime the next, depending on what benefits you most. However, if you have business or professional income, once you opt out of the New Regime, you can only switch back once in your lifetime.

Is the ₹75,000 Standard Deduction available in the New Regime?

Yes. As of the latest updates for FY 2026-27, the Standard Deduction is available under both the New and Old Regimes. This leveled the playing field significantly.

Does the New Regime have any tax-saving sections left?

Very few. Apart from the Standard Deduction, you can claim employer contributions to NPS (Section 80CCD(2)) and deductions for Agniveer Corpus Fund. Most other popular sections like 80C, 80D, and HRA are gone.

What is the tax-free limit in 2026?

Under the New Regime, income up to ₹3 Lakh is exempt from tax. However, due to the rebate under Section 87A, if your total taxable income is up to ₹7 Lakh, you pay zero tax.

Where can I find the official calculator?

You can use the official calculator provided by the Income Tax Department e-Filing portal. It is the most accurate source for checking your liability.