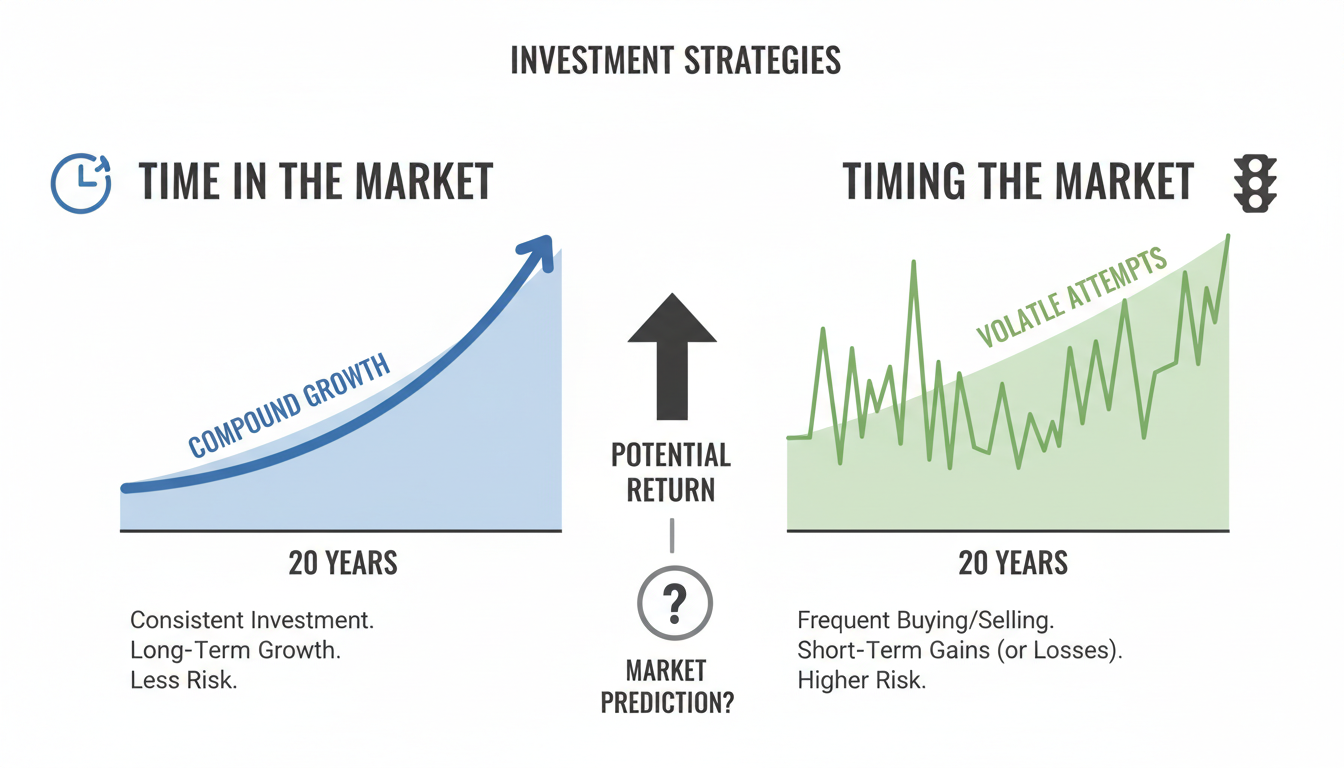

Here’s the brutal truth: trying to time the market is a loser’s game. I’ve sat across the table from brilliant doctors, engineers, and entrepreneurs who are absolute geniuses in their fields, yet they lose sleep—and money—trying to guess if the Nifty or S&P 500 has hit bottom.

It rarely works. In fact, most professionals can’t do it consistently either.

But here is the good news. You don’t need a crystal ball to build serious wealth in 2026. You need a system. A boring, reliable, automated system that works harder when the market is crashing.

In this guide, I’m going to walk you through the exact SIP strategies without market timing fails that I’ve used to help clients construct resilient portfolios. We aren’t just talking about “investing monthly.” We are talking about engineering your SIPs to capture volatility, compound faster, and protect your downside.

📑 What You’ll Learn

The Mathematics of Why Timing Fails

Let’s get the elephant out of the room. Why is “buying low and selling high” such bad advice for the average investor? Because it requires you to be right twice: once when you sell, and again when you buy back in.

According to data from S&P Dow Jones Indices, over a 15-year period, nearly 90% of active fund managers underperform the market index. If the pros with Bloomberg terminals and algorithmic trading bots can’t time it, what chance do we have?

The strategies below remove the “human error” element. They rely on math, not gut feelings.

1. The Step-Up SIP: Turbocharging Your Returns

Most investors set a SIP amount—say, $500 or ₹10,000—and forget it for a decade. That’s a mistake. It ignores your career trajectory. As your income grows in 2026 and beyond, your investment must keep pace to fight lifestyle inflation.

A Step-Up SIP (or Top-Up) automatically increases your contribution by a fixed percentage annually. It sounds small, but the compounding effect is massive.

Look at the difference a simple 10% annual increase makes over 20 years:

| Scenario | Monthly Start | Annual Increase | Total Invested | Est. Value (12% Return) |

|---|---|---|---|---|

| Static SIP | $500 | 0% | $120,000 | $499,574 |

| Step-Up SIP | $500 | 10% | $343,650 | $1,068,000 |

By simply clicking “yes” on the Step-Up option, you potentially double your corpus. You won’t miss the extra money because it coincides with your annual raise.

💡 Pro Tip

Don’t wait for your raise to hit your bank account before increasing your SIP. Set the Step-Up instruction with your broker now to trigger automatically on the same month you usually receive your appraisal or bonus. This removes the temptation to spend the extra cash.

2. Weaponizing Volatility: Rupee Cost Averaging

When the market drops 10%, do you panic? Most people do. But seasoned investors see a sale.

Rupee Cost Averaging (RCA) is the engine behind all successful SIP strategies without market timing fails. It’s simple arithmetic: when prices are high, your fixed SIP amount buys fewer units. When prices crash, that same amount buys more units.

Think of it like buying apples. If apples are usually $2, you get 50 for $100. If the price crashes to $1, you get 100 apples. When the price recovers to $2, your portfolio value explodes because you accumulated so much volume at the bottom.

🎯 Key Takeaway

Volatility is the friend of the SIP investor. The deeper the market dip during your accumulation phase, the higher your eventual returns will be—provided you do NOT stop your SIP.

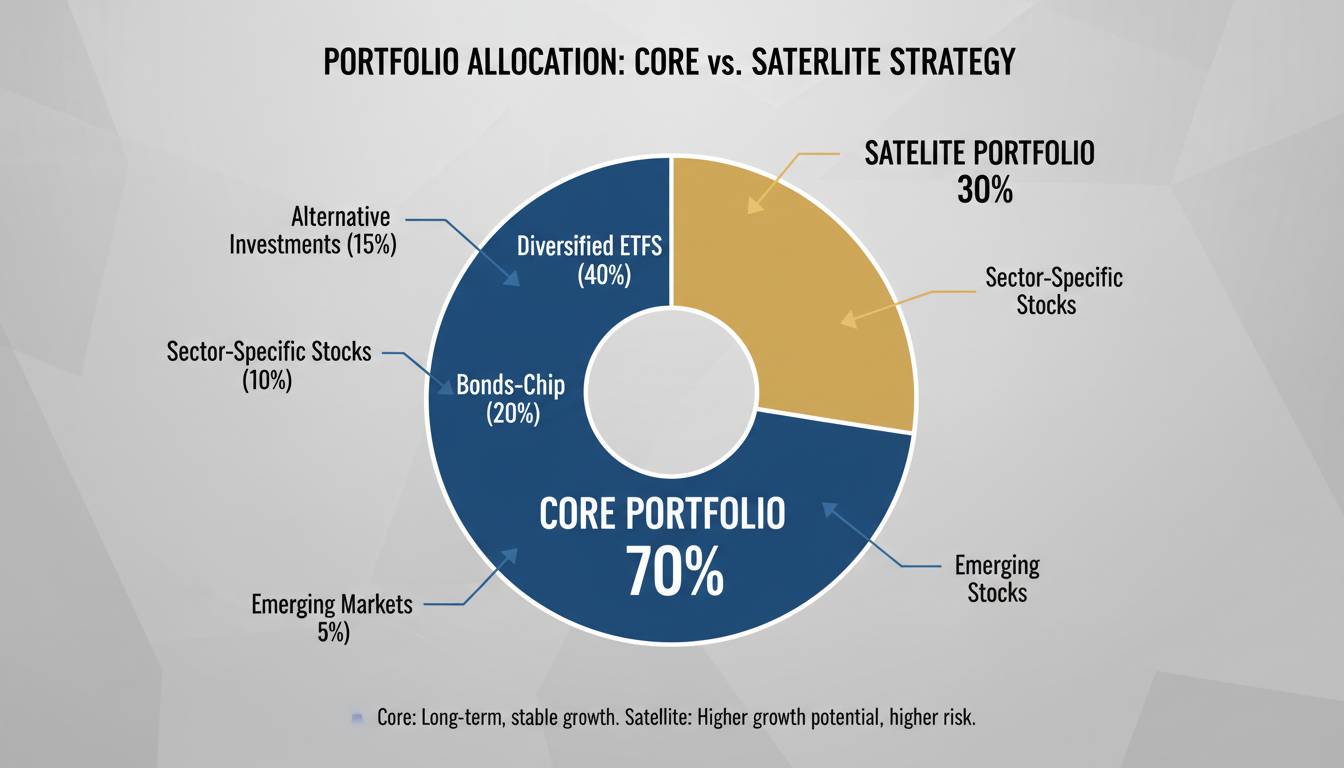

3. The Core & Satellite Approach

Diversification isn’t just about buying ten different funds. That often leads to “di-worsification,” where you own so many overlapping stocks that you’re just paying high fees for average performance.

In 2026, I recommend the Core and Satellite strategy to balance stability with aggressive growth.

The Core (70-80%)

This is your safety net. These funds should be boring. We’re talking about Index Funds (Nifty 50, S&P 500) or large-cap funds. They track the market and provide steady, reliable compounding.

The Satellite (20-30%)

This is where you chase “Alpha” (returns higher than the market). Use this portion for:

- Small-Cap Funds: High volatility, high potential reward.

- Thematic Funds: Sectors like AI, Green Energy, or Banking.

- Commodities: Gold or Silver ETFs for hedging.

⚠️ Watch Out

Never let your “Satellite” portfolio exceed 30% of your total allocation. These sectors can be cyclical. If a specific sector crashes (like Tech in 2022), you don’t want it to drag down your entire financial future.

4. The Systematic Transfer Plan (STP): How to Invest Lump Sums

Inherited money? Sold a property? Got a massive bonus? Dumping a large lump sum into the market all at once is terrifying. If the market crashes the next day, your portfolio takes a hit that could take years to recover from.

The solution is the STP. It bridges the gap between debt safety and equity growth.

Step-by-Step Guide to Setting Up an STP

- Park the Cash: Invest the entire lump sum into a Liquid Fund or Ultra-Short Duration Fund. These are low-risk and offer better returns than a savings account.

- Set the Instruction: Instruct the fund house to transfer a fixed amount (e.g., $5,000) from that Liquid Fund into an Equity Mutual Fund every week or month.

- Choose the Duration: For a large sum, spread the transfer over 6 to 12 months.

- Let it Run: You earn interest on the balance in the Liquid Fund while slowly averaging your entry into the stock market.

This is psychologically easier than a one-time investment and mathematically safer than holding cash in a bank account.

5. The Strategic Pause: Don’t Kill the Compounding

Life happens. Maybe you lost a job, or you have a medical emergency. The instinct is to cancel your SIPs. Don’t do it.

Canceling a SIP often requires new paperwork to restart, and inertia usually stops people from restarting for months or years. Instead, use the “Pause” feature.

Most platforms allow you to pause a SIP for 1 to 3 months. This keeps your folio active and your goals alive. It’s a temporary breather, not a full stop.

According to Investopedia, the power of compounding relies heavily on time. Interrupting that timeline for too long can drastically reduce your end corpus.

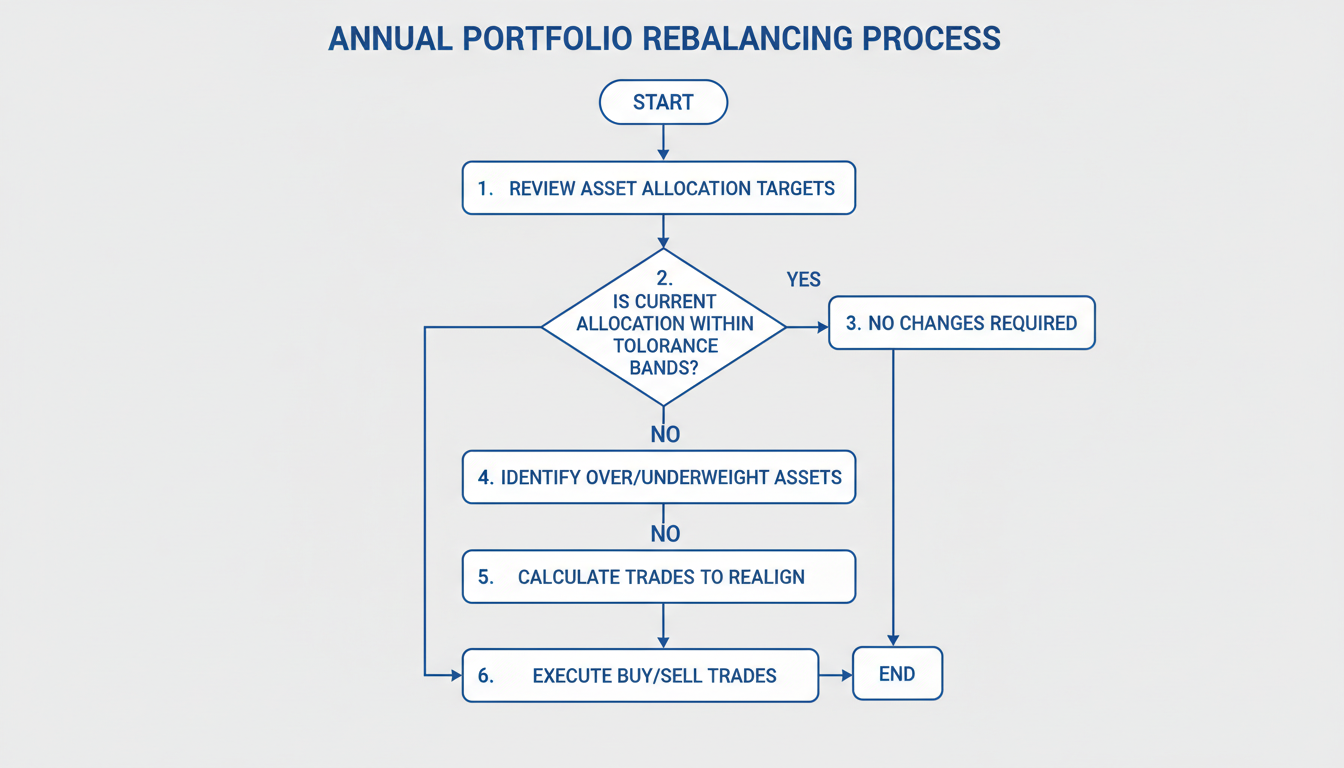

6. The Annual Rebalance (The Secret Sauce)

This is the strategy that separates the amateurs from the pros. Once a year—pick a date, like your birthday—check your asset allocation.

If equities have had a massive bull run, your portfolio might have shifted from a safe 60:40 (Equity:Debt) split to a risky 80:20. This exposes you to a crash.

| Asset Class | Target Allocation | Current (After Bull Run) | Action Required |

|---|---|---|---|

| Equity | 60% | 75% | Sell 15% Profit |

| Debt/Gold | 40% | 25% | Buy with Proceeds |

By rebalancing, you are forced to practice the golden rule: Sell High and Buy Low. You are skimming profits from the winner and buying the underperformer at a discount.

❓ Frequently Asked Questions

What is the best date for a monthly SIP?

There is no “lucky” date. However, practically speaking, schedule your SIP for 2-3 days after your salary credit date. This ensures the money is invested before you have a chance to spend it. This “pay yourself first” discipline is more valuable than trying to time a specific day of the month.

Should I stop my SIP when the market is at an all-time high?

No. Markets hit all-time highs frequently during bull runs. If you stop, you miss the momentum. Stick to your asset allocation. If the market is truly overheated, your annual rebalancing strategy will naturally take care of it by moving some profits into debt.

Can I lose money in a SIP?

Yes, in the short term. Equity markets are volatile. However, over periods longer than 7-10 years, the probability of negative returns diminishes significantly. SIPs reduce risk, but they do not eliminate it entirely.

How many funds should I have in my portfolio?

For most investors, 3 to 5 funds are sufficient. A large-cap index fund, a mid-cap fund, a small-cap fund, and perhaps an international fund. Owning 10+ funds usually leads to overlapping holdings and unnecessary complexity.

Final Thoughts: The Boring Path to Riches

The financial industry loves to sell complexity. They want you to believe you need complex algorithms and daily monitoring to succeed. But the most effective SIP strategies without market timing fails are surprisingly simple.

They rely on discipline, not intelligence. They rely on time, not timing.

If you implement the Step-Up SIP, stick to your Core/Satellite allocation, and use the STP for lump sums, you are already ahead of 95% of investors. Stop checking the ticker tape every morning. Let the system do the heavy lifting.

Ready to optimize your portfolio? Check out more resources on investment psychology at the CFA Institute Research Foundation to understand the behavioral side of money.