Here is the brutal truth: Most people treat their retirement planning like a lottery ticket. They throw money into an account, cross their fingers, and hope it turns into a million dollars by the time they turn 65. But hope isn’t a strategy. Math is.

If you want to know why some investors retire early while others work until they’re 75, it usually comes down to one simple habit: they ran the numbers. They didn’t just save; they engineered their wealth using an investment calculator.

In my experience analyzing hundreds of financial portfolios, the biggest gap between the wealthy and the aspiring isn’t income—it’s clarity. An investment calculator acts as a time machine. It lets you visit your financial future, see the results of your current habits, and come back to the present to fix them before it’s too late.

This isn’t just about punching numbers into a form. It’s about understanding the mechanics of wealth. In this guide, we’re going to strip away the jargon and show you exactly how to use this tool to accelerate your path to financial freedom.

📑 What You’ll Learn

Why Math Beats Luck Every Time

We humans are terrible at exponential thinking. We think linearly. If we save $10,000 this year, we assume we’ll have roughly $10,000 more next year. But money doesn’t move in straight lines—it curves upward. This is where an investment calculator becomes your most valuable asset.

It bridges the gap between “I think I’m saving enough” and “I know exactly when I can quit my job.”

When you use a calculator effectively, you stop guessing. You can answer the terrifying questions that keep most people awake at night: “Am I going to run out of money?” or “Can I actually afford that vacation home?”

🎯 Key Takeaway

An investment calculator is not just a math tool; it is a behavior modification device. By seeing the massive long-term impact of small short-term sacrifices, you are psychologically more likely to stick to your savings plan.

The “Eighth Wonder”: Visualizing Compound Interest

You’ve heard it before: start early. But until you see the data, it’s just advice. Let’s look at the numbers. The primary function of an investment calculator is to demonstrate the snowball effect of compound interest.

Here is a scenario I’ve seen play out dozens of times. Let’s compare two investors: “Early Ella” and “Late Larry.” Both want to retire rich, but their timelines are different.

| Investor Profile | Age Started | Age Stopped | Monthly Investment | Total Cash Invested | Value at Age 65 (7% Return) |

|---|---|---|---|---|---|

| Early Ella | 25 | 35 (Invests for 10 years only) | $500 | $60,000 | $787,000+ |

| Late Larry | 35 | 65 (Invests for 30 years) | $500 | $180,000 | $610,000 |

Look at that table again. Ella stopped saving at 35. She never put another dime in. Yet, she crushed Larry, who saved for three straight decades. That is the power of time, and that is exactly what an investment calculator reveals. If you aren’t running these scenarios, you are flying blind.

💡 Pro Tip

Don’t just calculate for “Retirement.” Use the calculator for intermediate goals too. Want to buy a house in 7 years? Run the numbers to see how much risk you can afford to take. Short-term goals usually require safer, lower-return assumptions.

Garbage In, Garbage Out: Mastering the Inputs

An investment calculator is only as smart as the person using it. If you tell it you’re going to earn 15% a year for 40 years, it will tell you you’re going to be a billionaire. Spoiler alert: You probably won’t be.

To get a result you can actually bank on, you need to understand the four pillars of the calculation.

1. The Principal (Starting Amount)

This is your seed money. While a large lump sum helps, don’t be discouraged if this number is zero. The “Monthly Contribution” variable is far more powerful over long horizons.

2. The Rate of Return (The “R” Factor)

This is where most people mess up. They look at the S&P 500’s best year (up 29%) and plug that in. That is dangerous. In our analysis of long-term market trends, a safe, inflation-adjusted estimate for stocks is typically between 6% and 8%. For bonds, it’s lower.

3. Time Horizon

How long will the money grow? Be precise. If you are planning to retire at 65, but you might be forced out of the workforce at 60 due to health or layoffs (a common occurrence), run the calculator for age 60. It’s better to be pleasantly surprised than caught short.

4. Compounding Frequency

Most calculators default to “Annually,” but in the real world, dividends are often reinvested quarterly, and you likely contribute monthly. Switching your calculator to “Monthly” compounding will give you a slightly more accurate (and usually higher) projection.

Step-by-Step: How to Project Your Wealth

Ready to build your roadmap? Don’t just read this—open a tab with a calculator and follow along. Here is the workflow professional planners use.

- Determine Your “Freedom Number”: Before you calculate growth, you need a target. A common rule of thumb is 25x your annual expenses. If you spend $60,000 a year, you need $1.5 million.

- Input Your Current Reality: Enter your current savings and your monthly contribution capacity. Be honest. If you can’t stick to $1,000 a month, don’t type it in.

- Set a Conservative Rate: Type in 7%. This is the historical average of the stock market after inflation. If you are a conservative investor (bonds/cash), use 4% or 5%.

- Run the “Gap Analysis”: Hit calculate. Are you hitting your Freedom Number by your desired age?

- If YES: Great. Now try it with a 5% return to stress-test your plan.

- If NO: You have three levers to pull: Save more now, retire later, or take on more risk (which isn’t always advisable).

- Adjust for Taxes: Remember, the calculator shows gross wealth. If this is a standard brokerage account, Uncle Sam will want his cut of the gains.

⚠️ Watch Out

Avoid the “Linear Fallacy.” Markets do not go up 7% every single year like a robot. You might be down 20% one year and up 30% the next. The calculator shows an average. Do not panic if your real-life account balance doesn’t match the calculator’s projection in year 3 or 4.

The Silent Killers: Inflation and Fees

If you ignore inflation and fees, your investment calculator is lying to you. A million dollars in 2050 will not buy what a million dollars buys today. It might buy what $400,000 buys today.

Most basic calculators show “Nominal” returns (the raw number). You need “Real” returns (purchasing power). The easiest way to handle this? Subtract inflation from your expected return.

The Formula:

Expected Market Return (8%) – Inflation (3%) = Calculator Input (5%)

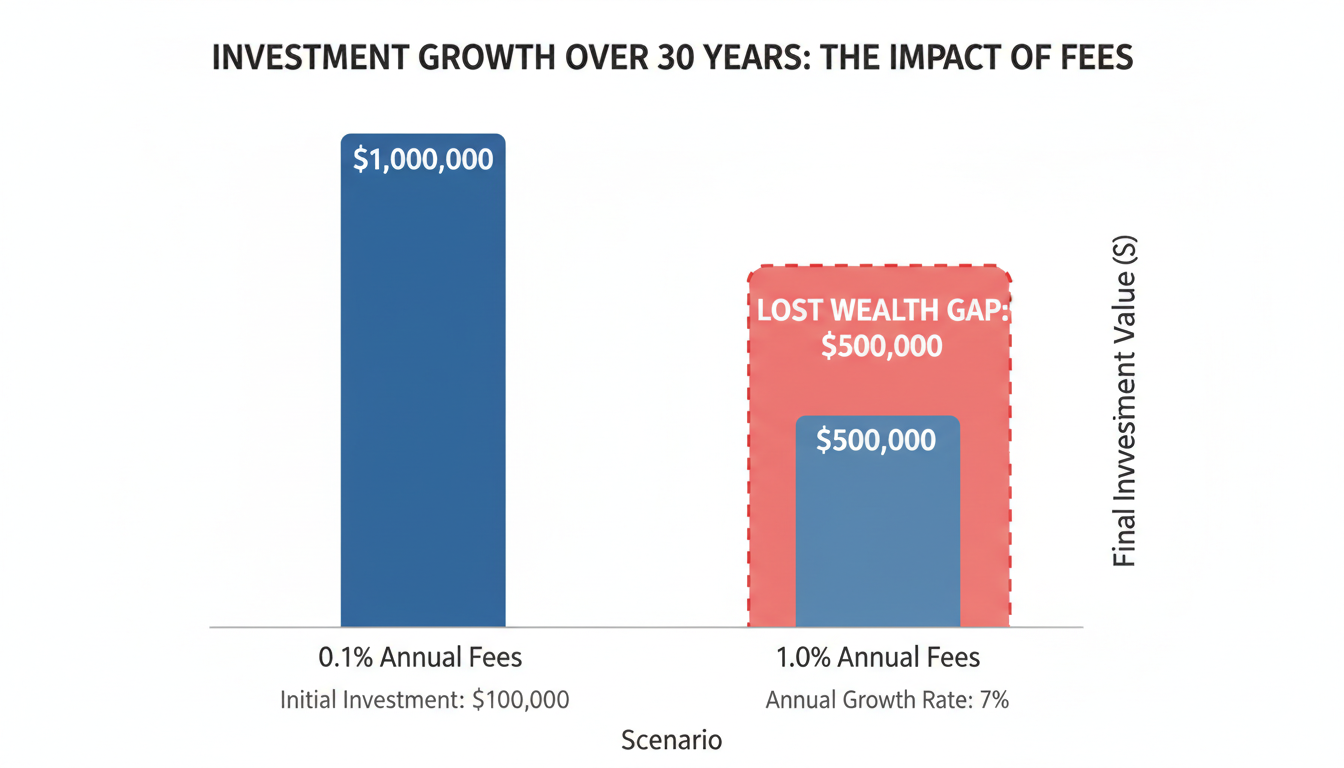

The Fee Drag

Investment fees are termites in your financial house. You don’t see them eating the foundation until the floor collapses. According to the SEC, a 1% fee difference can cost you over $100,000 over a lifetime.

Let’s look at how a seemingly small 1% fee impacts your final payout over 30 years on a $100,000 investment.

| Annual Return | Fee Charged | Net Return | Final Value (30 Years) | Amount Lost to Fees |

|---|---|---|---|---|

| 8% | 0.10% (Low Cost ETF) | 7.9% | $978,600 | ~$28,000 |

| 8% | 1.00% (Active Fund) | 7.0% | $761,200 | ~$245,000 |

That is a quarter of a million dollars lost to a “small” 1% fee. When using your calculator, always subtract the expense ratio of your funds from your expected return rate.

Advanced Strategy: Reverse Engineering

Most people use an investment calculator forward: “If I save X, what will I have?”

I want you to use it backward: “I need Y. What must I save to get there?”

This is called “Goal-Based Investing.” If you know you need $50,000 for a down payment in 5 years, play with the monthly contribution slider until the final number hits $50,000. That number is your new monthly bill. Pay it like you pay your rent. This shifts investing from “whatever is left over” to a non-negotiable obligation to your future self.

⚠️ Watch Out

Be careful with “Catch-Up” math. If you are starting late, the calculator might tell you to save 60% of your income to hit your goal. While mathematically correct, this might be behaviorally impossible. It is better to extend your timeline than to set a savings goal you will quit in two months.

❓ Frequently Asked Questions

How accurate are online investment calculators?

They are mathematically perfect but contextually blind. They calculate the math correctly, but they cannot predict market crashes, tax law changes, or personal emergencies. Use them for estimation and trend analysis, not as a guaranteed contract.

Should I include my home equity in the calculator?

Generally, no. Unless you plan to sell your home and downsize to fund your retirement, your home is a place to live, not a liquid asset you can withdraw from to buy groceries. Keep your investment calculations focused on liquid assets like stocks, bonds, and cash.

What is a “safe” rate of return to use?

For a diversified portfolio of stocks and bonds, 6% to 7% is a prudent, inflation-adjusted number. If you are 100% in stocks, you might use 8%, but be prepared for volatility. If you are in high-yield savings, use 3% to 4%.

Does the calculator account for taxes?

Most standard free calculators do not. They show pre-tax growth. If your money is in a 401(k) or Traditional IRA, remember that the government will take 20-30% of that final number when you withdraw it. Roth IRAs, however, are tax-free in retirement.

Why does the calculator show different results for monthly vs. annual contributions?

This is the power of compounding frequency. When you contribute monthly, that money starts earning interest immediately. If you wait to contribute a lump sum at the end of the year, you miss out on months of growth. Always set the calculator to “Monthly” for the most realistic scenario.

Conclusion: Your Future is a Math Problem (And You Can Solve It)

Financial freedom doesn’t happen by accident. It happens by design. An investment calculator is the blueprint for that design. It strips away the emotion and leaves you with the raw data you need to make decisions.

Here is my challenge to you: Don’t just close this tab. Find a calculator, input your real numbers, and look at the result. If you don’t like what you see, don’t panic. You have the power to change the variables. Increase your savings rate by 1%, work one year longer, or reduce your fees. Small tweaks today compound into massive differences tomorrow.

The best time to plant a tree was 20 years ago. The second best time is today. Run the numbers, set your plan, and let the math do the heavy lifting.