In the world of finance, few concepts are as foundational yet frequently misunderstood as interest. Whether you are taking out a loan, investing for retirement, or just managing a savings account, the way interest is calculated determines the trajectory of your money. To truly master personal finance, you must first master the mathematical distinction: the simple interest vs compound interest formula.

While simple interest is linear and calculated only on the initial principal, compound interest is exponential, calculating interest on both the principal and the accumulated interest from previous periods. Understanding this core difference is not just academic; it’s the key to making informed decisions that can save you thousands on debt or dramatically accelerate your wealth accumulation.

Understanding the Fundamentals of Simple Interest

Simple interest is the easiest form of interest to calculate and understand. It is a fixed rate applied only to the initial principal amount over a specified period. This type of interest is commonly used for short-term loans, basic savings accounts, and certain types of bonds.

Defining the Simple Interest Calculation

The beauty of simple interest lies in its straightforward nature. The calculation remains consistent throughout the life of the loan or investment. It does not factor in the interest earned (or charged) in previous periods.

The core components required for the calculation are:

- P (Principal): The initial amount of money borrowed or invested.

- R (Rate): The annual interest rate (expressed as a decimal).

- T (Time): The duration of the loan or investment, usually measured in years.

The formula for calculating the interest earned (I) is:

I = P × R × T

To find the total future value (A), you simply add the interest earned to the principal: A = P + I.

Key Characteristics of Simple Interest

Interest is calculated strictly on the original principal amount.

Growth Pattern

Growth is linear; the amount of interest earned each period is exactly the same.

Common Applications

Short-term personal loans, installment loans, and specific types of business credit.

Decoding the Simple Interest vs Compound Interest Formula

When comparing the mechanics of financial growth, the contrast between the simple interest vs compound interest formula highlights a fundamental divergence in how money multiplies. While simple interest provides predictable, steady returns, compound interest offers exponential growth potential.

As the renowned physicist Albert Einstein reportedly said, "Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it." This quote underscores why understanding both formulas is paramount.

Let’s examine the underlying structure of each formula before diving into detailed examples.

Simple Interest Formula (I = PRT)

Focuses on the initial capital. The interest earned in the first year is exactly the same as the interest earned in the tenth year, assuming the principal remains unchanged.

Compound Interest Formula (A = P(1 + r/n)^(nt))

Focuses on the growing capital base. Interest is added back to the principal (it "compounds"), meaning subsequent interest calculations are based on a larger and larger sum.

Deep Dive into the Simple Interest Formula and Mechanics

To truly appreciate the concept, let’s walk through a practical scenario using the simple interest calculation.

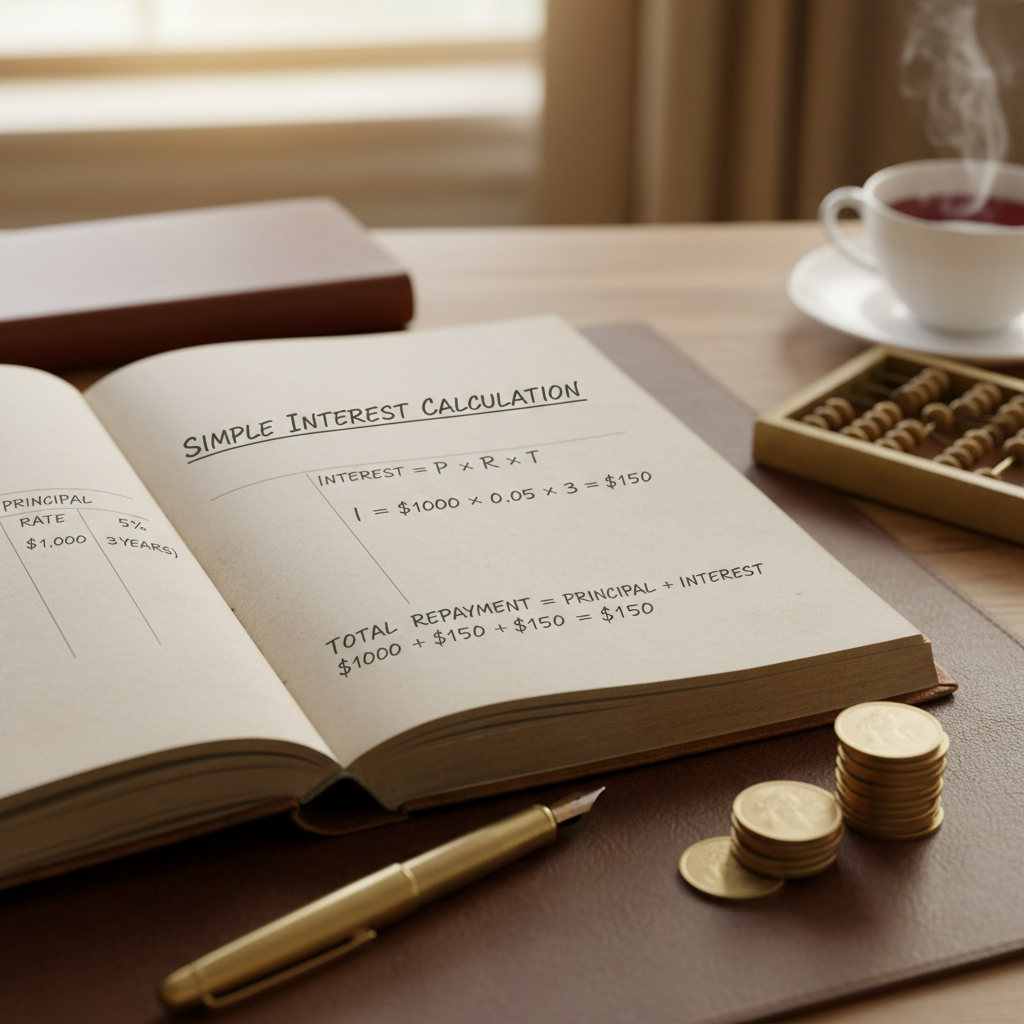

Example Calculation 1: The Basic Loan

Imagine you borrow $10,000 at a 5% annual simple interest rate for 3 years. We want to find the total interest paid and the total amount repaid.

- P (Principal) = $10,000

- R (Rate) = 0.05 (5% as a decimal)

- T (Time) = 3 years

Using the formula I = P × R × T:

I = $10,000 × 0.05 × 3 = $1,500

The total interest paid over 3 years is $1,500. The total repayment amount (A) would be $10,000 + $1,500 = $11,500.

If you need quick calculations for scenarios like this, utilizing a reliable Simple Interest Calculator can provide immediate results, helping you compare different interest rates and time horizons efficiently.

It is important to note that the amount of interest attributed to each year is $500 ($1,500 divided by 3 years). This fixed annual interest payment is the hallmark of simple interest.

Why Compound Interest Changes the Game

Compound interest is often referred to as "interest on interest." The key mechanism that differentiates it from simple interest is the compounding period. The more frequently interest is compounded (annually, semi-annually, quarterly, or daily), the faster the investment or debt grows.

The Compound Interest Formula Explained

Calculating compound interest is more complex than simple interest because the base (the principal) changes with every compounding period. The formula for the future value of an investment (A) that is compounded regularly is:

A = P(1 + r/n)^(nt)

- A: The final amount (Principal + Interest)

- P: The initial principal balance

- r: The annual interest rate (as a decimal)

- n: The number of times interest is compounded per year

- t: The number of years

Example Calculation 2: The Power of Compounding

Let’s take the exact same principal and rate: $10,000 invested at 5% annual interest for 3 years, but this time, it compounds annually (n=1).

- Year 1: $10,000 × 0.05 = $500 interest. New Principal = $10,500.

- Year 2: $10,500 × 0.05 = $525 interest. New Principal = $11,025.

- Year 3: $11,025 × 0.05 = $551.25 interest. New Principal = $11,576.25.

Total interest earned: $500 + $525 + $551.25 = $1,576.25.

Compare this to the $1,500 earned under simple interest. While the difference is small over three years, this discrepancy grows exponentially over longer time horizons, especially with high compounding frequency.

To understand the profound impact of compounding over time, especially for retirement savings, it is helpful to explore authoritative financial education resources like the definition of compound interest on Investopedia, which often illustrates the long-term benefit.

Practical Applications: When to Expect Simple Interest

While compounding dominates long-term savings and investments (like retirement accounts and complex loans), simple interest still plays a crucial role in several financial products. Knowing where to expect simple interest can help consumers evaluate costs accurately.

Payday Loans and Short-Term Debt

Many very short-term, high-interest loans calculate interest using the simple method. While the interest calculation is simple, the annualized rates are often extremely high, making repayment challenging.

Installment Loans (Some Types)

Certain installment loans, especially those structured with a fixed repayment schedule over a few years (e.g., student loans, car loans), often use simple interest on the outstanding principal balance.

Basic Certificates of Deposit (CDs)

Some CDs, particularly those offered by smaller institutions, may advertise simple interest rates, meaning the interest is paid out periodically rather than reinvested immediately.

It is crucial for consumers to read the terms and conditions carefully. Just because a loan uses simple interest doesn’t automatically mean it’s cheaper; the rate (R) is the ultimate determining factor in the overall cost or return.

Key Differences Summarized: Simple Interest vs Compound Interest Formula

The distinction between these two methods is vital for anyone managing money. Simple interest is linear and predictable, while compound interest is dynamic and often more powerful. Recognizing when the simple interest vs compound interest formula is being applied is the cornerstone of effective financial planning.

Basis of Calculation

Simple: Always calculated on the original principal amount (P).

Compound: Calculated on the principal plus all previously accumulated interest (P + I).

Growth Trajectory

Simple: Linear growth. The return or cost per period is constant.

Compound: Exponential growth. The return or cost accelerates over time.

Impact on Time

Simple: Time (T) increases the total interest proportionally.

Compound: Time (T) and the compounding frequency (n) increase the total amount dramatically.

Formula Comparison

Simple Interest: I = PRT

Compound Interest: A = P(1 + r/n)^(nt)

Strategic Investment Decisions

When making investment or borrowing decisions, you should always strive to be on the receiving end of compounding and the paying end of simple interest, if possible. For investments, seek accounts that compound frequently (daily or monthly) to maximize growth.

Conversely, when borrowing, understand that debt structured with compounding interest (like credit cards or mortgages) can quickly snowball if not managed properly. While mortgages technically use compounding calculations, they are structured amortization schedules that simplify the periodic payment, but the underlying mechanism is still interest on the remaining principal balance, which changes over time.

Financial education resources, such as those provided by the Federal Reserve Education, emphasize that understanding how interest accrues is fundamental to avoiding financial pitfalls.

In summary, the choice between simple and compound interest is usually not yours to make – it is dictated by the financial product. Your power lies in recognizing which formula is applied and adjusting your financial behavior accordingly: maximizing time and compounding frequency for savings, and minimizing both for debt.

Conclusion

The difference between the simple interest and compound interest formula is the difference between linear progression and exponential growth. Simple interest offers a transparent, predictable calculation based solely on the principal, making it ideal for short-term financial arrangements. Compound interest, however, leverages time and frequency to generate significantly higher returns (or costs) because it calculates interest on previously earned interest.

By mastering these two core financial formulas and understanding the implications of P, R, T, and N, you gain the ability to accurately forecast your financial future, whether you are planning to pay off a loan or build lasting wealth.

FAQs

Simple interest is calculated only on the original principal amount. Compound interest is calculated on the principal plus all accumulated interest from previous periods. This reinvestment of interest is what allows compound interest to grow exponentially.

Compound interest is overwhelmingly better for investors because it allows money to grow faster over time, especially over long periods. Investors seek high compounding frequency (e.g., daily or monthly) to maximize returns.

The formulas themselves remain the same, but the perspective changes. For investments, you want the highest possible interest rate and compounding frequency. For loans, you want the lowest possible interest rate, and ideally, debt that is structured using simple interest or fixed amortization schedules to limit the growth of the total obligation.

The compounding frequency (n) dictates how many times per year the interest is added back to the principal. A higher ‘n’ (e.g., compounding monthly, n=12, versus annually, n=1) results in faster growth, because the interest starts earning its own interest sooner.

Generally, a single financial product is structured using one method or the other, though compounding is far more common for long-term debts like mortgages or high-interest debts like credit cards. Simple interest is primarily reserved for very specific, often short-term, contracts or fixed installment plans where the interest component is clearly defined upfront.

Read Also:

- Find the Best App to Split Bills with Friends: Ultimate Comparison Guide for Seamless Group Expenses

- How to Easily Make Bar Graph Online Free: The Ultimate Guide to Data Visualization Success

- Mastering Your Health: Understanding the Blood Sugar Level Chart by Age 50 for Effective Diabetes Management

- The Ultimate Guide to Choosing and Using a Cash Counter Calculator India

- PAK to BIN Converter Online: The Ultimate 2026 Safety Guide

- Text to Hex Converter: The Complete 2026 Guide for Developers

- The 7:30 to 3:30 Work Schedule: A 2026 Guide to Reclaiming Your Life

- Watts vs. Hertz: Your 2026 Electrical Guide

- Citation Generator: Streamline Academic Writing – Visual Story

- PAK to BIN Dangers: Your 2026 Safety Plan

- Unlock PDFs in 2026: Your Ultimate Guide

- Supercharge Your SEO with AI in 2026

- Unlock SEO Rich Snippets in 2026

- 9 Uses of a Currency Converter to Save Money & Avoid Fees – Visual Story

- JSON to CSV: Your 2026 Data Guide

- Convert Sq Yards to Tons: The Ultimate 2026 Pro Guide

- Measure Any Room Like a Pro: 2026

- Your 2026 SEO Content Playbook

- Capital Letter Mistakes Costing Millions in 2026?