Here’s a brutal truth about money: it never sleeps. It’s either working 24/7 to build your wealth, or it’s working 24/7 to dig you into a hole you can’t climb out of. The difference between those two realities usually comes down to one thing—understanding the math.

I’ve spent years analyzing financial content and strategies, and I can tell you that the gap between the “average” saver and the wealthy investor isn’t just income. It’s how they leverage the simple interest vs compound interest formula.

Albert Einstein reportedly called compound interest the “eighth wonder of the world,” adding that “he who understands it, earns it; he who doesn’t, pays it.” Whether that quote is apocryphal or not, the math holds up. In this guide, we aren’t just going to look at dry formulas. We’re going to tear apart the mechanics of wealth, look at real-world 2026 examples, and show you exactly how to position your money on the right side of the equation.

📑 What You’ll Learn

The Foundation: What is Simple Interest?

Let’s start with the basics. Simple interest is exactly what it sounds like—clean, linear, and predictable. It’s the “flat fee” of the finance world.

When you deal with simple interest, the calculation is based strictly on the principal amount (the original chunk of money you borrowed or invested). It doesn’t care about the interest you earned last year or last month. It has a short memory.

In my experience, you’ll mostly encounter this in short-term situations: personal loans from friends, some auto loans, and certain types of bonds. It’s great for borrowers because the debt doesn’t spiral, but it’s terrible for investors because the growth is painfully slow.

The Simple Interest Formula

The math here is straightforward. You don’t need a financial degree to run these numbers on a napkin.

I = P × R × T

- P (Principal): The starting amount.

- R (Rate): The annual interest rate (written as a decimal, so 5% becomes 0.05).

- T (Time): The duration in years.

To get the total final amount (A), you just add that interest back to your principal: A = P + I.

💡 Pro Tip

If you are taking out a personal loan or a car loan, always ask if it’s a “simple interest” loan. If you pay off a simple interest loan early, you save money on interest. Some predatory loans use “pre-computed” interest where you owe the full interest amount even if you pay it off in week one. Avoid those at all costs.

The Accelerator: How Compound Interest Works

Now, let’s talk about the heavy hitter. Compound interest is “interest on interest.” It’s the snowball effect in action.

Imagine rolling a snowball down a hill. At first, it’s small. But as it rolls, it picks up more snow. The surface area gets bigger, so it picks up even more snow with every rotation. That is compounding.

With compound interest, the math calculates returns on your principal plus all the accumulated interest from previous periods. In the early years, the curve looks flat. But give it time, and that curve goes vertical. This is how retirement accounts turn modest monthly contributions into millions over a career.

The Compound Interest Formula

This formula is a bit more intimidating, but it’s where the magic happens. The key variable here isn’t just the rate—it’s the frequency.

A = P (1 + r/n)nt

- A: The future value of the investment/loan.

- P: The principal investment amount.

- r: The annual interest rate (decimal).

- n: The number of times that interest is compounded per year.

- t: The number of years the money is invested or borrowed for.

⚠️ Watch Out

The variable ‘n’ (compounding frequency) is a silent wealth killer when you are in debt. Credit cards typically compound daily. That means every single day, your debt grows slightly larger, and tomorrow’s interest is calculated on that new, larger number. This is why a $5,000 balance can take decades to pay off if you only make minimum payments.

Head-to-Head: The Formulas Compared

To really grasp the simple interest vs compound interest formula debate, you need to see them side-by-side. The structural differences dictate where you should use them.

| Feature | Simple Interest | Compound Interest |

|---|---|---|

| Formula | I = P × R × T | A = P (1 + r/n)nt |

| Basis of Calculation | Principal only | Principal + Accumulated Interest |

| Growth Trajectory | Linear (Slow & Steady) | Exponential (Accelerates over time) |

| Best For… | Borrowing money (Car loans, personal loans) | Investing (Savings, Stocks, 401k) |

| Impact of Time | Constant return regardless of duration | Massive returns as time increases |

According to educational resources from the U.S. Securities and Exchange Commission (SEC), the frequency of compounding can dramatically alter the outcome. A savings account compounding daily will always outperform one compounding annually, assuming the same rate.

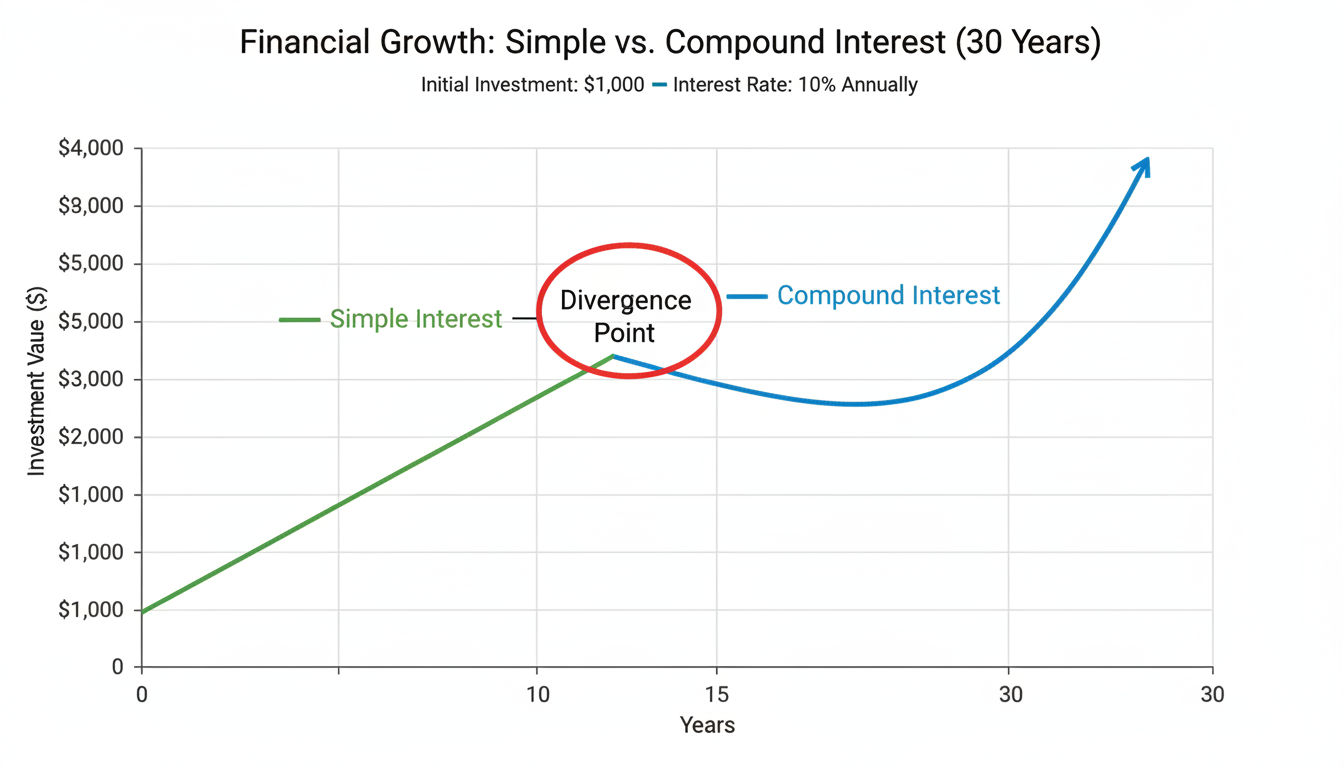

Real-World Scenarios: The $100k Difference

Let’s stop looking at variables and start looking at dollars. This is where the theory hits your bank account.

The Scenario: You have $10,000 to invest. You find two opportunities. Both offer an 8% annual return. You plan to leave the money alone for 30 years to fund your retirement in 2056.

- Option A: A corporate bond paying Simple Interest.

- Option B: A diversified index fund paying Compound Interest (compounded annually).

Here is how the math plays out over three decades:

| Year | Option A (Simple) Value | Option B (Compound) Value | The “Gap” |

|---|---|---|---|

| Year 1 | $10,800 | $10,800 | $0 |

| Year 10 | $18,000 | $21,589 | +$3,589 |

| Year 20 | $26,000 | $46,609 | +$20,609 |

| Year 30 | $34,000 | $100,626 | +$66,626 |

Look at that gap. $66,626.

You didn’t work harder for Option B. You didn’t save more money. You simply chose the right mathematical formula. In Option A, your money earned a flat $800 every single year. In Option B, by year 30, your money was earning over $7,000 per year in interest alone.

🎯 Key Takeaway

Time is the fuel for compound interest. The difference between simple and compound interest is negligible over 1 or 2 years, but over 20+ years, it is the difference between a comfortable retirement and working until you’re 80. Start early, even if the amount is small.

Step-by-Step: How to Calculate It Yourself

You don’t need a fancy financial calculator to run these numbers. Here is a quick guide to doing a “back of the napkin” check on an investment using the Rule of 72 (a mental shortcut for compound interest).

- Identify your Interest Rate: Let’s say you expect a 9% return on the stock market.

- The Magic Number: Take the number 72.

- Divide: Divide 72 by your interest rate (72 / 9 = 8).

- The Result: The answer (8) is roughly how many years it will take for your money to double using compound interest.

- Project: If you are 30 years old with $10,000, at 9%, you’ll have $20k at age 38, $40k at age 46, $80k at age 54, and $160k at age 62.

For precise calculations, I always recommend checking your work against the Federal Reserve Education tools, which offer excellent calculators for free.

Strategic Moves for 2026

Understanding the simple interest vs compound interest formula is useless if you don’t apply it. Based on the current economic landscape of 2026, here is how you should play your hand.

1. Flip the Script on Debt

If you have high-interest credit card debt (20%+ APR), you are on the wrong side of the compound interest equation. The bank is getting rich off your “n” variable. Attack this debt with fury. Every dollar you pay off is a guaranteed 20% return on your money—you won’t find that in the stock market.

2. The “Frequency” Hack

When opening a high-yield savings account, check the fine print. Does it compound monthly? Quarterly? Daily? Always choose daily compounding if the rates are equal. It seems small, but over a decade, those extra fractions of pennies add up to real dollars.

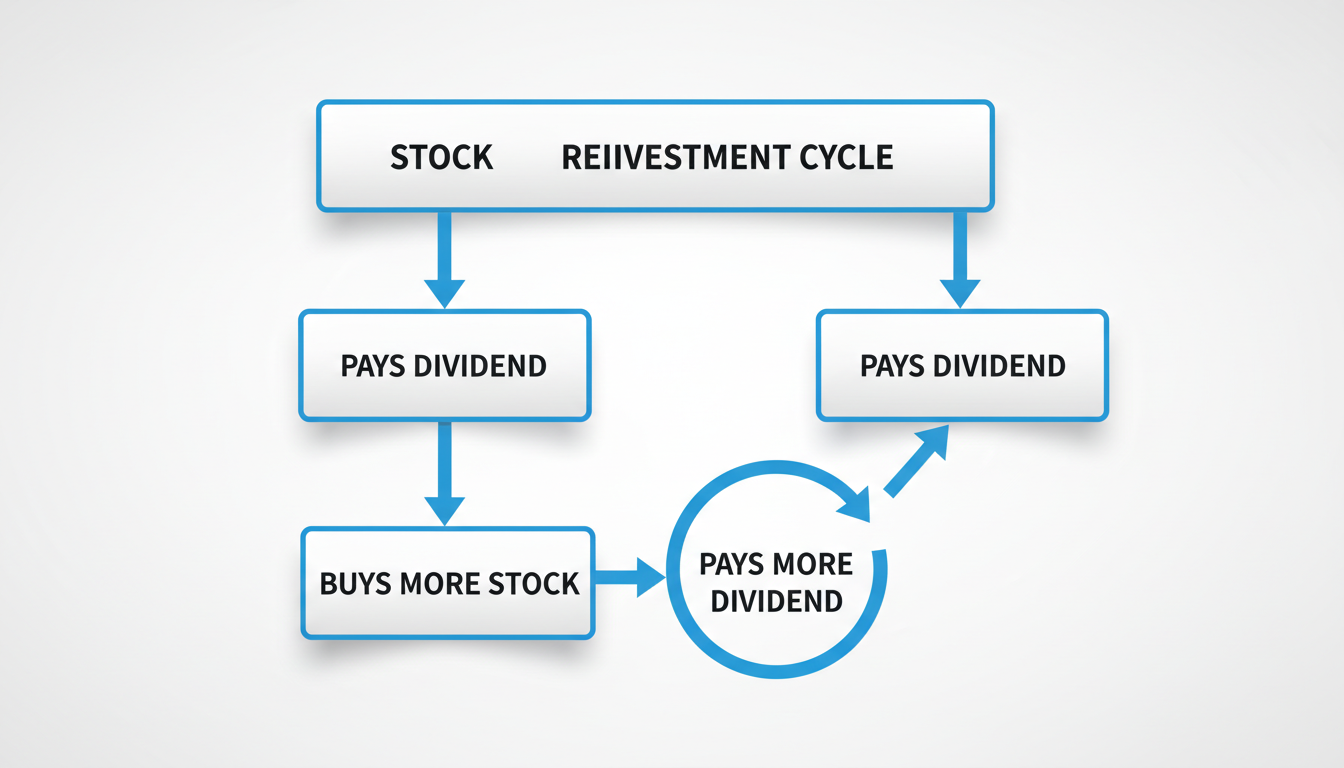

3. Reinvest Dividends Automatically

If you own stocks, you likely get dividend payments. Do not cash these out. Set up a DRIP (Dividend Reinvestment Plan). This forces your simple interest (the dividend) to become compound interest (by buying more shares, which then earn their own dividends).

⚠️ Watch Out

Inflation is the “invisible” compound interest working against you. If your money is sitting in a shoebox or a checking account earning 0.01%, it is losing purchasing power every year. To build wealth, your compound interest rate must exceed the inflation rate.

❓ Frequently Asked Questions

Is a mortgage simple or compound interest?

This surprises most people: standard U.S. mortgages are typically simple interest loans, calculated monthly on the outstanding principal balance. However, because the amortization schedule is front-loaded with interest, it can feel like compounding. Paying extra toward the principal early in the loan saves you massive amounts of simple interest later.

Can simple interest ever be higher than compound interest?

In terms of total return? No, not if the rate and time are the same. However, a simple interest investment with a massive interest rate (e.g., 15%) could outperform a compound investment with a tiny rate (e.g., 2%) over a short period. But given enough time, the compound curve almost always wins.

What is “Continuous Compounding”?

This is the theoretical limit of compounding. Instead of compounding daily or hourly, the formula assumes interest is added at every possible instant. It uses the mathematical constant e. While rare in consumer banking, it’s used heavily in derivatives trading and advanced economics.

Why do car loans use simple interest?

Lenders use simple interest for auto loans because the asset (the car) depreciates rapidly. They want a fixed, predictable repayment schedule. It also benefits the borrower; if you get a bonus at work and pay off your car loan two years early, you stop paying interest immediately on the remaining balance.

Conclusion

Look, the debate between the simple interest vs compound interest formula isn’t just academic fluff. It’s the operating system of your financial life. Simple interest is linear, safe, and predictable—ideal for when you have to borrow money. Compound interest is exponential, powerful, and aggressive—the engine you need for your investments.

If you take one thing away from this guide, let it be this: Time is your greatest lever. You can’t control the stock market, and you can’t always control interest rates. But you can control when you start.

Don’t wait for the “perfect” time to invest. The math shows clearly that starting today with a small amount beats starting tomorrow with a large one. For more on the fundamentals of growth, I highly recommend checking out Khan Academy’s Finance Unit to visualize these concepts further.

Get the math working for you, not against you.