Do you know your “Number”?

I’m not talking about your phone number or your pin code. I’m talking about the exact dollar amount you need to walk away from the 9-to-5 grind and never look back. If you’re like most people, you probably have a vague idea. Maybe you’re thinking, “A million sounds good,” or “I’ll just work until I’m 70.”

Here’s the hard truth: Hope is not a strategy.

In 2026, with shifting inflation rates and evolving market dynamics, flying blind is the fastest way to crash your financial future. You need precision. You need a plan. And the single most effective tool to bridge the gap between where you are and where you want to be is a high-quality Retirement Calculator.

I’ve spent years analyzing financial tools, and I’ve seen the difference this simple step makes. It transforms anxiety into action. In this guide, we’re going to strip away the confusion and show you exactly how to use this tool to engineer the life you deserve.

📑 What You’ll Learn

The “Ostrich Effect”: Why You Need to Look Now

There’s a psychological phenomenon where people avoid negative financial information because it causes stress. It’s called the Ostrich Effect. We bury our heads in the sand, hoping things will work out.

But here is the thing: ignoring the math doesn’t change the math.

Whether you are twenty-five and just starting your career, or fifty-five and eyeing the finish line, a Retirement Calculator acts as a mirror. It reflects your current reality. Sometimes that reflection is scary. Maybe you’re behind. That’s okay. Knowing you are behind is the only way to catch up.

🎯 Key Takeaway

A retirement calculator isn’t just a math tool; it’s a behavior modification device. By turning vague fears into concrete numbers, it empowers you to make small adjustments today that compound into massive wealth tomorrow.

7 Critical Reasons to Use a Calculator Today

Why bother plugging numbers into a form? Because the human brain is terrible at calculating exponential growth. We think linearly (1, 2, 3), but money grows exponentially (2, 4, 8). Here is why you need digital help.

1. It Defines Your “Enough”

Most people aim for arbitrary numbers. A calculator looks at your spending, your lifestyle goals, and your lifespan to give you a personalized target. It shifts the goal from “get rich” to “get $2.4 million.”

2. It Visualizes the Power of Compounding

Einstein reportedly called compound interest the eighth wonder of the world. A calculator shows you exactly how your money makes babies, and then those babies make babies. Seeing this curve shoot upward is incredibly motivating.

3. It Accounts for the “Silent Killer” (Inflation)

A dollar in 2026 won’t buy a coffee in 2056. Good calculators adjust for purchasing power, ensuring you don’t save a million dollars only to find out it spends like $500,000.

4. It Integrates Social Security

You aren’t in this alone. According to the Social Security Administration, benefits replace about 40% of an average earner’s income. A calculator layers this on top of your savings for a complete picture.

5. It Highlights the Gap

This is the most valuable feature. It shows the “Gap” between what you have and what you need. If the gap is huge, don’t panic. It just means you need to pull a lever: save more, spend less, or work longer.

6. It Allows for “What If” Scenarios

What if you retire at 62 instead of 67? What if the market crashes the year you retire? Advanced tools let you stress-test your plan against different economic realities.

7. It Saves You From Tax Surprises

Not all money is created equal. A million dollars in a Roth IRA is very different from a million in a traditional 401(k) due to taxes. Calculators help you see your spendable income.

Under the Hood: How These Tools Actually Work

To get the best results, you have to understand the engine driving the car. A Retirement Calculator is essentially a complex algorithm that processes four main data buckets:

- Current Assets: What you have today.

- Contributions: What you add monthly/yearly.

- Time Horizon: How long the money has to grow.

- Rate of Return: How fast the money grows.

The magic happens when these variables interact. A small change in “Rate of Return” or “Contributions” can swing your final number by hundreds of thousands of dollars over a few decades.

💡 Pro Tip

Never use a static rate of return. The stock market doesn’t give you a flat 8% every year. Look for calculators that use “Monte Carlo simulations.” These run thousands of random market scenarios to give you a probability of success (e.g., “You have an 85% chance of not running out of money”).

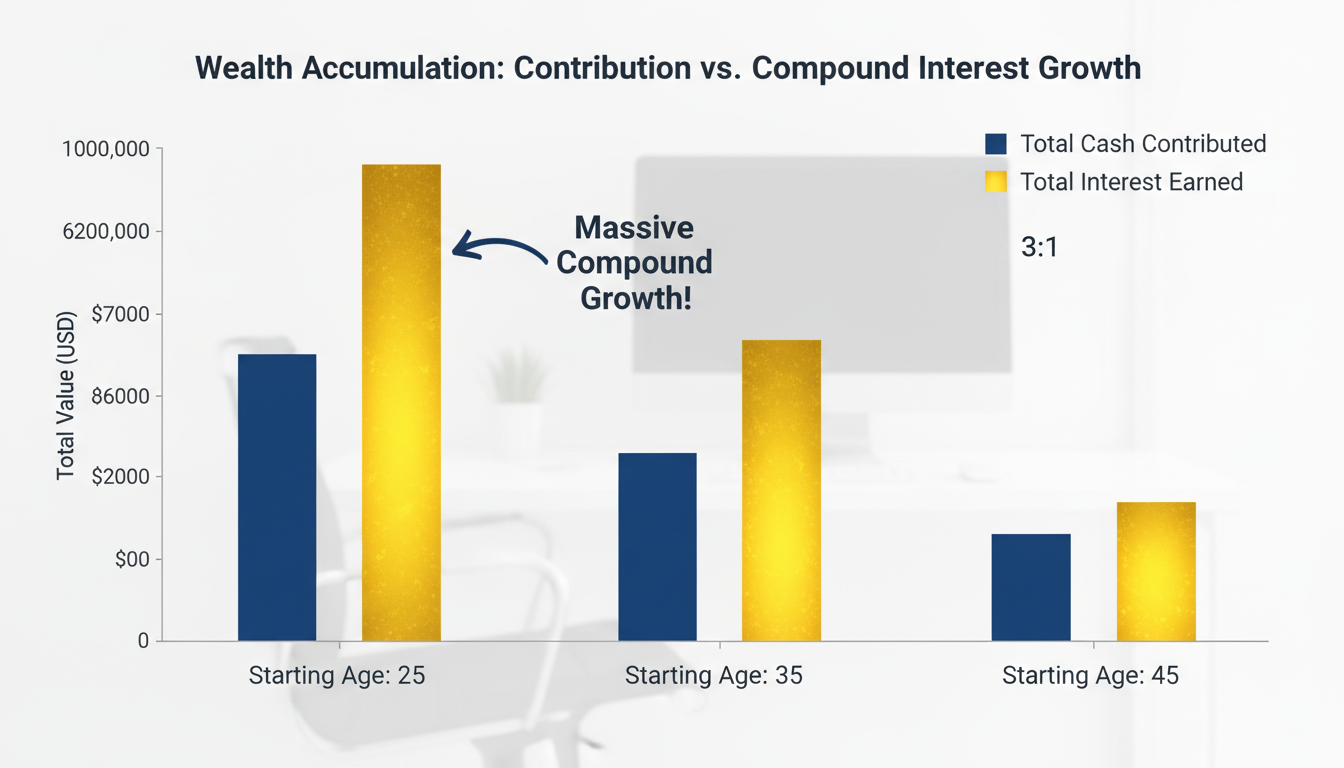

Data: The High Cost of Waiting

I can tell you to start early, but numbers speak louder. Let’s look at three people who all want to retire at 65 with $1 million. They all earn a 7% annual return. Look at how much more the procrastinator has to pay out of pocket.

| Starting Age | Monthly Savings Needed | Total Cash Contributed | Interest Earned (Free Money) |

|---|---|---|---|

| 25 Years Old | $381 | $182,880 | $817,120 |

| 35 Years Old | $820 | $295,200 | $704,800 |

| 45 Years Old | $1,920 | $460,800 | $539,200 |

The takeaway? The 25-year-old only has to invest $182k of their own money to become a millionaire. The 45-year-old has to invest nearly half a million. Time does the heavy lifting.

Step-by-Step: Your 15-Minute Financial Audit

Ready to stop guessing? Follow this workflow. You don’t need a degree in finance, just a cup of coffee and your login info.

Step 1: Gather Your Intel

You can’t build a house without bricks. Before you open a calculator, get these numbers ready:

- Current balance in 401(k)s, IRAs, and brokerage accounts.

- Your current annual income.

- Your estimated monthly spending in retirement (be realistic!).

- Your expected Social Security benefit (create an account at SSA.gov to find this).

Step 2: Choose Your Weapon

Not all calculators are equal. Here is a quick comparison of what to use based on your needs.

| Calculator Type | Best For… | Pros | Cons |

|---|---|---|---|

| Simple Web Calculator | Quick check-ins & beginners | Fast, easy, no login required | Ignores taxes & complex scenarios |

| Detailed Planner | Serious planning (Age 40+) | Includes taxes, healthcare, pensions | Takes 20+ minutes to set up |

| Monte Carlo Sim | Final validation (Age 50+) | Accounts for market crashes | Can be overwhelming/complex |

Step 3: Run the Numbers & Stress Test

Input your data. Look at the result. Now, break it. Lower your expected return by 2%. Increase your inflation assumption to 4%. Does your plan survive? If not, you need a bigger safety margin.

⚠️ Watch Out

Don’t forget healthcare. Research from Fidelity Investments consistently shows that a retired couple may need over $300,000 just for out-of-pocket medical expenses. If your calculator doesn’t have a specific field for this, add it to your “monthly spending” estimate.

3 Traps That Will Ruin Your Calculation

I’ve seen smart people make bad plans because they fed the calculator bad data. Avoid these pitfalls.

1. The “Linear Life” Fallacy

You won’t spend the same amount every year in retirement. Most people spend more in the early “Go-Go” years (travel, hobbies) and less in the later “Slow-Go” years. Advanced calculators allow for “spending stages.”

2. Over-Optimism on Returns

The S&P 500 has historically returned about 10%, but that’s an average. If you retire into a recession, you might see -20%. To be safe, use a conservative estimate of 6% to 7% real return (after inflation) in your projections.

3. Ignoring Taxes

This is the big one. If you have $1 million in a traditional 401(k), the IRS owns about 20-30% of that. You don’t have a million; you have $750,000. Always calculate based on after-tax value.

💡 Pro Tip

Update your calculation once a year. Treat it like a physical for your wallet. Pick a date—like your birthday or New Year’s—and run the numbers again. Life changes, and your plan should too.

Conclusion: Your Future Starts with a Click

Financial freedom is a marathon, not a sprint. But you can’t run a marathon if you don’t know where the finish line is. A Retirement Calculator is your GPS. It replaces anxiety with facts and vague wishes with a concrete roadmap.

By using these tools correctly, adjusting for the realities of 2026, and updating your plan annually, you are doing more than just saving money—you are buying your future freedom.

Don’t wait for the “perfect time.” The perfect time was yesterday. The second best time is right now. Open a calculator, input your numbers, and take the first step toward a retirement you can actually enjoy.

❓ Frequently Asked Questions

How accurate are retirement calculators?

They are estimates, not crystal balls. They are excellent for identifying trends and gaps in your savings, but they cannot predict future market crashes or tax law changes. Use them as a guide, not a guarantee.

What rate of return should I use in 2026?

Given current economic conditions, financial experts often recommend a conservative estimate of 6% to 7% for equity-heavy portfolios. If you are closer to retirement and hold more bonds, adjust this down to 4% or 5%.

Does a retirement calculator account for inflation?

Good ones do. Look for a “Real Rate of Return” setting or an “Inflation Rate” input. We recommend setting inflation to at least 3% to be safe. If a calculator doesn’t offer this, it’s too basic for serious planning.

Should I include my home equity?

Generally, no—unless you plan to sell your home and downsize to fund your retirement. Your home is a place to live, not a liquid asset you can buy groceries with.