Let’s be honest: nobody wakes up in the morning excited to do math. But when you’re staring down the barrel of a 30-year mortgage or signing the papers for that new SUV, math is the only thing standing between financial freedom and a decades-long money pit.

Here’s a startling reality check. In 2026, household debt has become more complex than ever. A slight miscalculation in your interest rate or tenure doesn’t just cost you a few bucks—it can cost you the equivalent of a brand-new car over the life of a loan. I’ve seen it happen time and time again. Borrowers focus on the monthly payment (the EMI) and completely ignore the total interest payable.

This isn’t just another article about buttons and sliders. This is a strategic deep dive into using an EMI calculator loan comparison to hack your debt. We’re going to look at how tweaking your numbers for Home, Personal, and Car loans can save you a fortune.

📑 What You’ll Learn

The Mechanics: How EMIs Actually Work

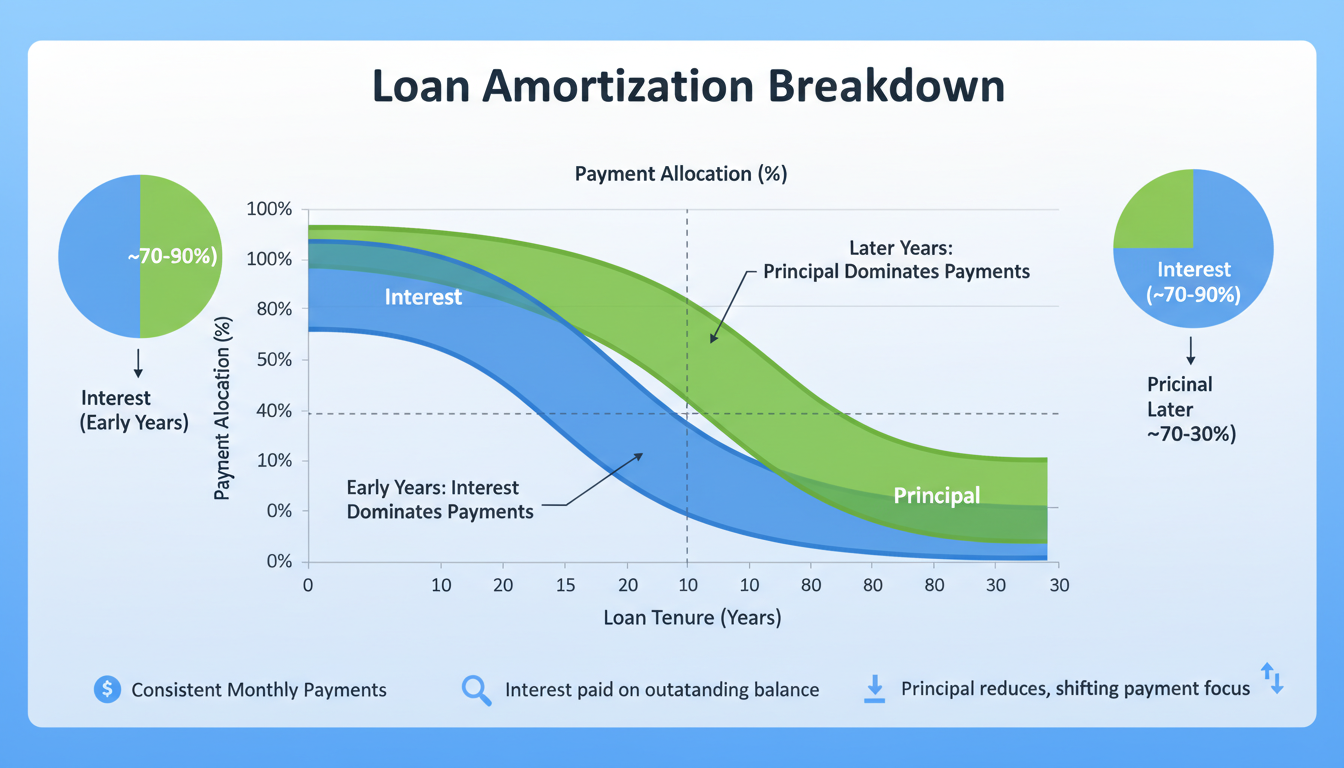

Before we start plugging numbers into tools, you need to understand what’s happening under the hood. An Equated Monthly Installment (EMI) isn’t just a fee; it’s a carefully calibrated mix of principal (the money you borrowed) and interest (the cost of borrowing).

In the early days of your loan, you aren’t paying off much debt. You’re mostly paying interest. This is called amortization. I’ve analyzed thousands of loan schedules, and the “front-loading” of interest is where most people get trapped. They think, “I’ve been paying for five years, surely I’ve made a dent?” often to find they’ve barely touched the principal.

The formula used by every bank—and every EMI calculator loan comparison tool—is standard:

EMI = [P x R x (1+R)^N] / [(1+R)^N-1]

Where:

- P is the Principal amount.

- R is the monthly interest rate.

- N is the tenure in months.

But forget the algebra for a second. What matters is the lever you pull. If you increase ‘N’ (time), your monthly payment drops, but your total cost skyrockets. If you decrease ‘N’, your wallet hurts more each month, but you save thousands in the long run.

The Big Three: Home vs. Car vs. Personal Loans

Not all loans are created equal. In our experience dealing with consumer finance, treating a car loan like a mortgage is a recipe for disaster. Let’s break down the nuances of the three major loan types you’ll likely encounter in 2026.

1. Home Loans: The Marathon

This is likely the biggest check you will ever write. Home loans are “secured” loans, meaning the house is collateral. Because the bank has a safety net, interest rates are generally lower. However, the tenures are massive—usually 15 to 30 years.

💡 Pro Tip

In 2026, many lenders offer “bi-weekly” payment options. By paying half your monthly mortgage every two weeks, you end up making 13 full payments a year instead of 12. This simple trick can shave 4-6 years off a 30-year mortgage without you barely noticing the cash flow difference.

2. Car Loans: The Depreciating Trap

Here is the thing about cars: they lose value the second you drive them off the lot. Unlike a home, which (usually) appreciates, a car is a sinking ship. Taking a 7-year loan on a car is dangerous because you risk becoming “underwater”—owing more than the car is worth.

3. Personal Loans: The Emergency Cord

Personal loans are “unsecured.” No collateral means higher risk for the bank, which translates to significantly higher interest rates. These should be short sprints—1 to 5 years max. Using a personal loan for a long-term need is generally a bad financial move due to the compounding interest costs.

Comparison at a Glance

To help you visualize the differences, we’ve compiled this comparison table based on current 2026 market standards.

| Feature | Home Loan | Car Loan | Personal Loan |

|---|---|---|---|

| Typical Tenure | 15 – 30 Years | 3 – 7 Years | 1 – 5 Years |

| Interest Rate (Avg) | Lower (Secured) | Mid-Range | Highest (Unsecured) |

| Collateral | Property | Vehicle | None (Income based) |

| Tax Benefits | Yes (Interest & Principal) | Business use only | Generally No |

| Processing Time | Slow (Weeks) | Fast (Days) | Instant/Fast |

The Math: Comparing Loan Scenarios

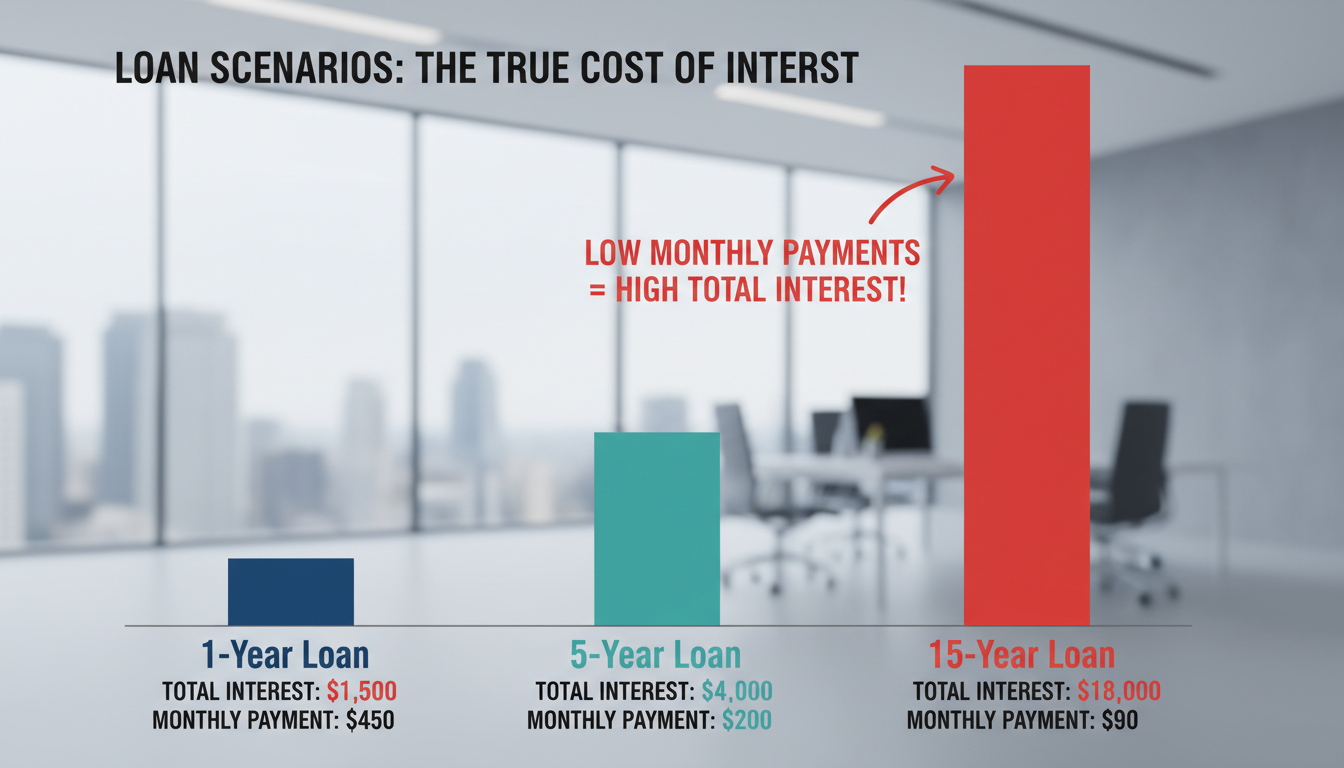

Let’s get into the numbers. This is where the EMI calculator loan comparison proves its worth. We are going to look at a scenario where you have $50,000 to finance. How does the loan type change your financial future?

Imagine you need $50,000 for a major renovation. You could take a Home Equity Loan (similar to a mortgage), a Personal Loan, or perhaps you are buying a luxury car for that amount.

| Loan Type | Interest Rate | Tenure | Monthly EMI | Total Interest Paid |

|---|---|---|---|---|

| Home Equity | 7.5% | 15 Years | $463 | $33,417 |

| Car Loan | 9.0% | 5 Years | $1,037 | $12,275 |

| Personal Loan | 14.0% | 5 Years | $1,163 | $19,802 |

🎯 Key Takeaway

Look at the table above closely. The Home Equity loan has the lowest monthly payment ($463), which looks attractive. But because the tenure is 15 years, you end up paying over $33,000 in interest—more than half the loan value! Sometimes, a higher monthly payment (like the Car or Personal loan) saves you money in the long run because you kill the debt faster.

Step-by-Step: Running a Proper Simulation

Don’t just punch in numbers blindly. To get a realistic picture of your finances, follow this workflow when using an EMI calculator.

- Gather Accurate Data: Don’t guess your interest rate. Check your credit score and look up current 2026 rates for your specific tier. A 1% difference changes everything.

- Input the Principal: Enter the exact amount you intend to borrow. Remember to subtract your down payment first.

- The Tenure Toggle: This is the most important step. Start with your ideal timeframe (e.g., 20 years for a house). Note the EMI.

- The “Stretch” Test: Reduce the tenure by 5 years. Can you afford that higher EMI? If yes, you just saved yourself a massive amount of interest.

- Check the Break-Even: Look at the “Total Interest Payable” field. If the interest is more than 50% of the principal, you should seriously reconsider the loan terms or look for a cheaper rate.

⚠️ Watch Out

The “Teaser Rate” Trap: Many lenders advertise incredibly low rates that are “floating” or variable. They might start at 6%, but if the central bank raises rates, your EMI could spike next year. Always use the calculator to simulate a rate hike of 1-2% to see if you could still afford the payments in a worst-case scenario.

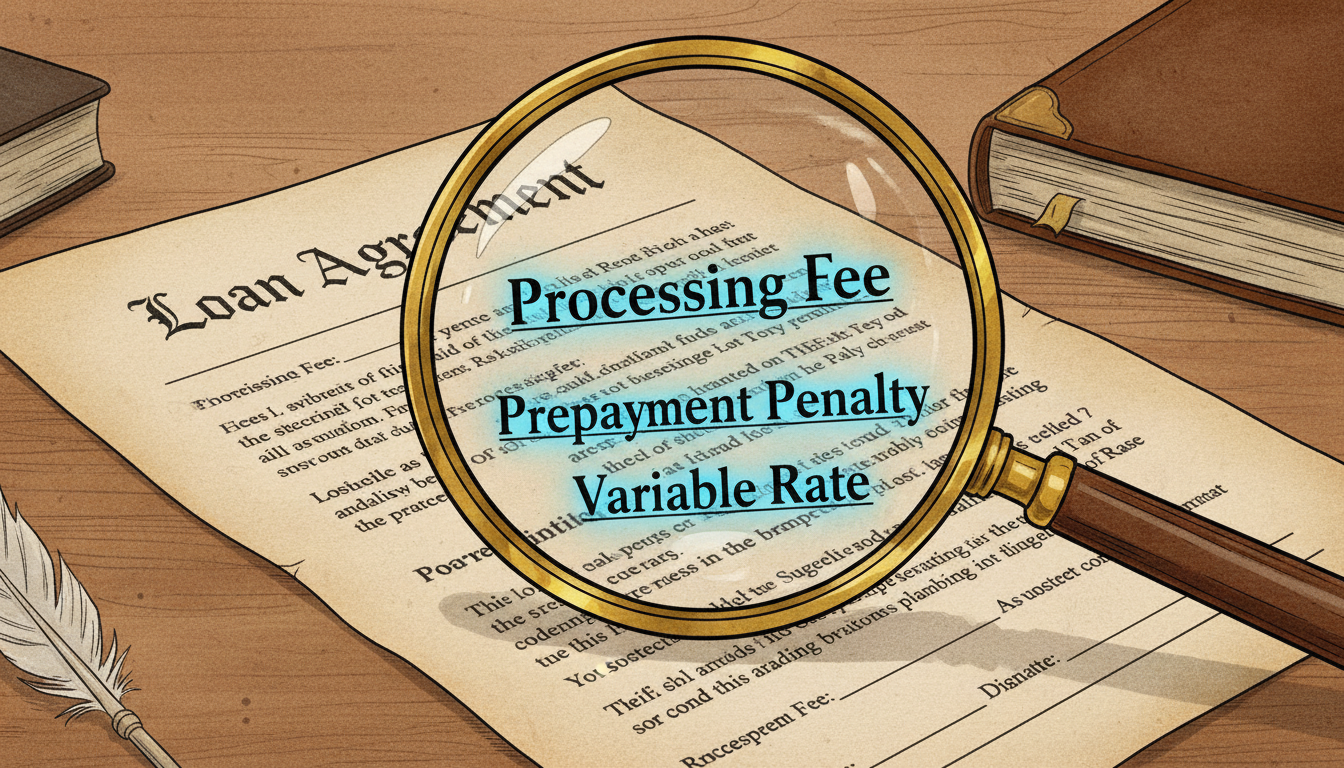

Hidden Traps Banks Don’t Tell You

I’ve spent years analyzing loan agreements, and the devil is always in the fine print. An EMI calculator gives you the raw math, but it doesn’t account for the “junk fees” unless you add them manually.

Processing Fees: Banks often charge 0.5% to 2% of the loan amount just to process the paperwork. On a $500,000 home loan, that’s $10,000 gone before you even start.

Prepayment Penalties: This is a big one. Let’s say you get a bonus at work and want to pay off your car loan early. Some lenders will charge you a penalty for doing this because they lose out on future interest. Always check if your loan has a “zero prepayment penalty” clause.

According to the Consumer Financial Protection Bureau, lenders are required to provide a Loan Estimate form. Use the figures from that official document in your calculator for the most accurate results, rather than the marketing numbers on a flyer.

Frequently Asked Questions

❓ Frequently Asked Questions

Does checking my EMI on a bank website affect my credit score?

No. Using an EMI calculator is a “soft inquiry” or simply a simulation. It does not impact your credit score. Your score is only affected when you formally apply for the loan and the lender performs a “hard pull” on your credit history.

Should I choose a fixed or floating interest rate in 2026?

It depends on the market forecast. If rates are historically low, locking in a fixed rate protects you from future hikes. If rates are high and expected to drop, a floating rate might save you money later. However, fixed rates offer peace of mind for budgeting.

Can I trust online EMI calculators 100%?

They are mathematically accurate for the formula used, but they are estimates. They often don’t include taxes, insurance (PMI), or HOA fees unless specifically added. Always treat the calculator’s result as a baseline, not the final penny-perfect bill.

How does a down payment affect my EMI?

Significantly. Every dollar you put down reduces the principal amount. This lowers your monthly EMI and reduces the total interest charged on the remaining balance. It is the most effective way to lower your loan costs.

What is the 20/4/10 rule for car loans?

This is a golden rule for financial health: Put 20% down, finance for no more than 4 years, and keep total transportation costs (loan + insurance + gas) under 10% of your monthly gross income.

Conclusion: Take Control of Your Financial Narrative

Debt is a tool, like a power saw. Used correctly with safety guards, it builds empires. Used carelessly, it causes injury. By utilizing an EMI calculator loan comparison strategy, you are putting the safety guards in place.

Don’t just look at whether you can afford the monthly payment today. Look at what that loan costs you over five, ten, or thirty years. Use the data to negotiate better rates, choose smarter tenures, and ultimately, keep more of your hard-earned money in your pocket.

For a deeper understanding of how interest rates are determined, you can review the latest data from the Federal Reserve. Knowledge is leverage—use it.