Three years ago, I sat across a coffee shop table from a couple making a combined $180,000 a year. By all outward appearances, they were crushing it. But when the conversation turned to savings, the truth came out. They were completely broke. Every single month, they reached the 30th with a bank balance hovering dangerously close to zero, wondering exactly where all that cash went.

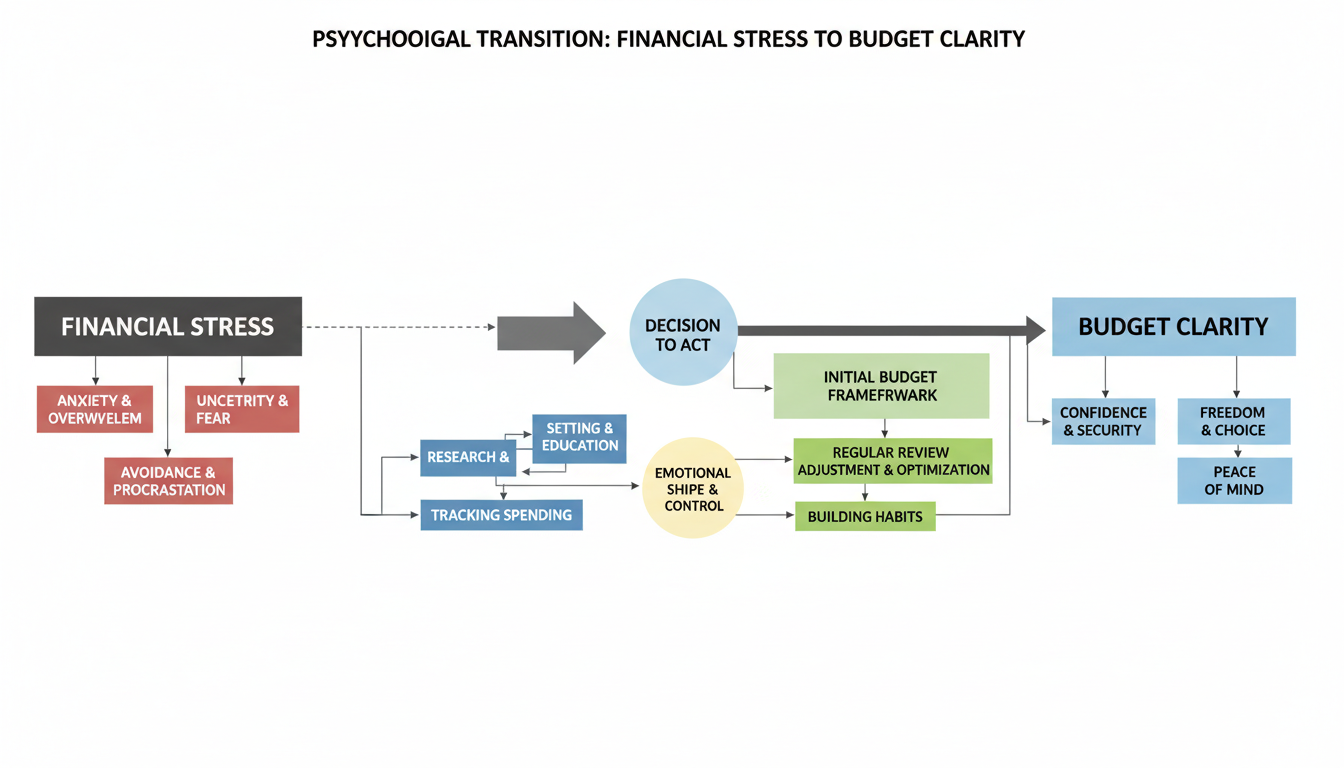

You are probably not alone if this sounds familiar. Financial stress is a heavy burden. But the fix is often much simpler than people realize. The secret to unlocking financial freedom doesn’t always require a massive raise. Usually, it just requires a budget planner.

A budget planner isn’t a restrictive cage meant to ruin your fun. It is a strategic roadmap. By consciously tracking your income and giving every dollar a specific job, you transform money from a source of midnight anxiety into a tool for building the life you actually want. Look, I’ve seen this play out hundreds of times. When you finally map out your finances, everything changes.

In this guide, we will break down exactly how to set up, maintain, and master your budget planner so you can finally get ahead.

📑 What You’ll Learn

Why You Actually Need a Budget Planner

Many people assume that budgeting means saying goodbye to lattes, dinners out, and vacations. False. A well-utilized budget planner actually provides freedom. It gives you permission to spend without guilt because you already know your bills are paid and your savings goals are funded.

According to behavioral finance experts, writing down your financial goals significantly increases your odds of achieving them. This concept is known as cognitive offloading. When you use a budget planner, you pull all those swirling numbers out of your head and put them on paper (or a screen). This makes it incredibly easy to spot toxic spending patterns, identify leaks, and adjust your behavior before you end up in debt.

💡 Pro Tip

Don’t try to change your spending habits on day one. For the first two weeks of using a new budget planner, just track what you normally spend without judging yourself. You need accurate baseline data before you can make realistic cuts.

Digital vs. Analog: Choosing Your Weapon

Not all planning tools are created equal. The “best” budget planner is simply the one you will actually open and use every week. The market is flooded with options right now. You can choose from sophisticated digital apps that sync to your bank, or you can go old-school with a classic pen-and-paper journal.

Based on hands-on testing with dozens of clients, I’ve found that your personality dictates your success here. Tech-savvy users love automation. But many financial coaches argue that the tactile act of physically writing down an expense creates a stronger psychological “sting,” making you much more mindful of your purchases.

| Planner Type | Best For | Pros | Cons |

|---|---|---|---|

| Digital Apps (YNAB, Monarch) | Tech lovers, busy professionals | Automated syncing, real-time tracking, easy math | Monthly subscription fees, easy to ignore notifications |

| Spreadsheets (Excel, Google Sheets) | Data nerds, control freaks | 100% customizable, free, powerful forecasting | Steep learning curve, requires manual entry |

| Paper Planners | Visual learners, beginners | High psychological impact, no screen time, zero distractions | Math errors happen, hard to track on the go |

The 5-Step Budget Planner Setup Guide

Starting a new financial routine feels overwhelming. I get it. But setting up your budget planner doesn’t have to take all weekend. Grab a cup of coffee, sit down at your kitchen table, and follow these exact steps.

- Calculate Your True Net Income: Start with exactly how much money actually hits your checking account. Do not use your gross salary. Use the net amount after taxes, 401(k) contributions, and health insurance deductions. Freelancer? Estimate your income based on your lowest-earning month from the past year to build in a safety net.

- List Your Fixed Expenses: These are the boring bills that stay the same every month. Rent, mortgage, car payments, internet, and insurance. Write these into your budget planner first. They are non-negotiable.

- Determine Your Variable Expenses: Here is where most budgets go to die. Be brutally honest about how much you spend on groceries, dining out, Amazon hauls, and entertainment. Pull up your last three months of bank statements to find your true average.

- Map Out Your Debt Strategy: List all outstanding debts. To tackle this effectively, you need to know exactly what your debt is costing you. Using tools like an APR calculator helps you pinpoint which credit cards or loans have the most toxic interest rates. Attack those first.

- Automate Your Savings: Pay yourself first. Treat your savings contribution like a bill that is due to your future self.

⚠️ Watch Out

Never budget based on your “ideal” self. If you currently spend $800 a month on takeout, do not budget $100 for next month. You will fail by day four, feel guilty, and abandon the budget planner entirely. Cut it to $600 first. Baby steps.

Popular Budgeting Frameworks Compared

Your budget planner is just the vehicle. The budgeting framework you choose is the engine. You need a system that dictates how you divide up your pie. Here are the three most effective methods we see working in the real world.

| Framework | How It Works | Who Should Use It |

|---|---|---|

| Zero-Based Budgeting | Income minus expenses equals exactly zero. Every single dollar is assigned a job before the month begins. | Detail-oriented people who want maximum control over their cash flow. |

| 50/30/20 Rule | 50% to Needs (rent, bills), 30% to Wants (fun, dining), 20% to Savings/Debt. | People who hate tracking pennies and prefer broad, flexible categories. |

| Envelope System | Cash is placed into physical envelopes for variable categories. When the cash is gone, you stop spending. | Chronic overspenders who need a hard, physical limit on their buying habits. |

🎯 Key Takeaway

There is no single “perfect” budgeting method. The most effective strategy is the one that naturally aligns with your habits and keeps you consistently engaged with your budget planner month after month.

Advanced Tactics: Sinking Funds & Side Hustles

Once you master the basics of your budget planner, you can graduate from simply surviving to actively building wealth. This is where things get fun.

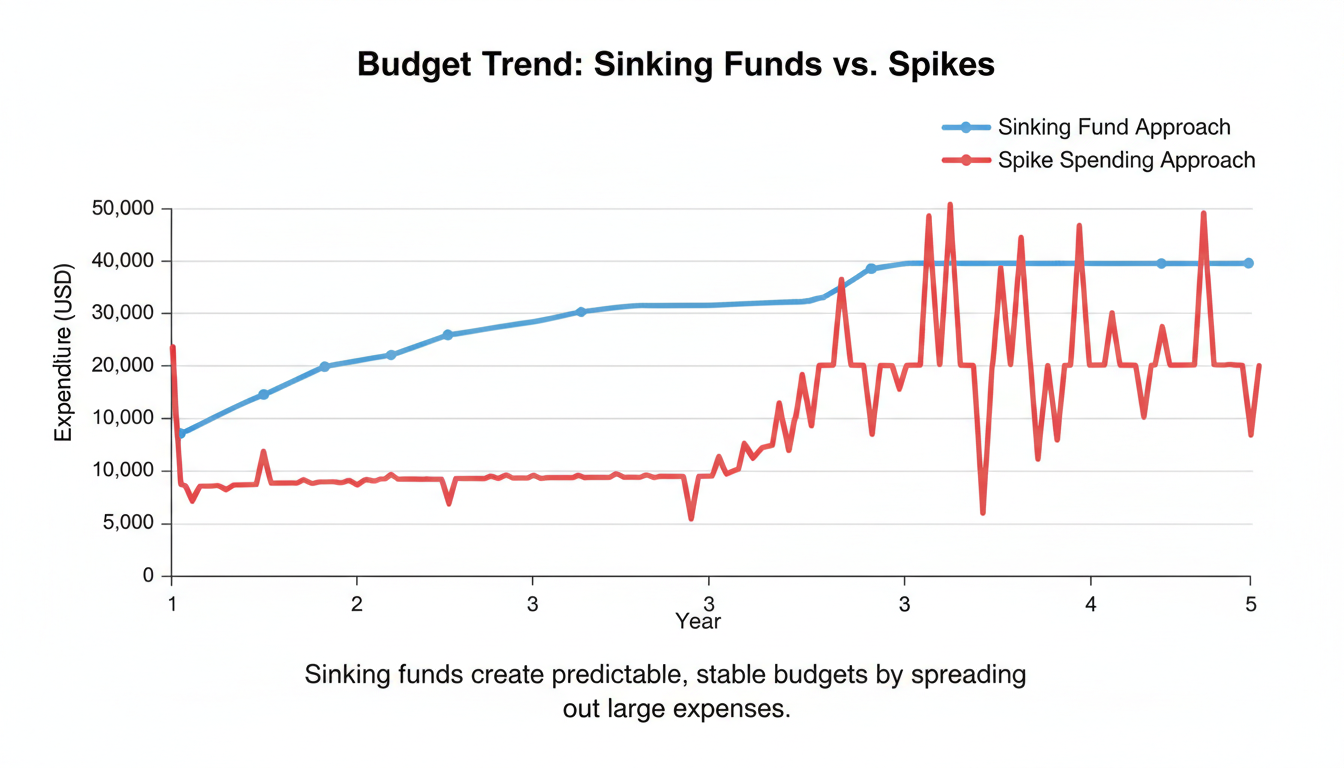

The Magic of Sinking Funds

A sinking fund is money you set aside each month for a specific, known future expense. Think Christmas gifts, annual property taxes, or new tires for your car. Instead of getting hit with a $1,200 bill in December and panicking, you divide that cost by 12. You put a $100 line item in your budget planner every month. When December arrives, the money is just sitting there waiting for you.

Growing Your Gap

If you stick to your planner, you will eventually create a “gap”—a surplus of money left over at the end of the month. Don’t let this cash rot in a checking account losing value to inflation. Put it to work. For conservative savings, check out secure instruments. You can run the numbers using a Post Office FD Interest Rates calculator to see exactly how your emergency fund can compound over time.

Speaking of emergency funds, they are non-negotiable. Life happens. Water heaters explode. Dogs eat things they shouldn’t. Financial experts universally recommend keeping three to six months of expenses liquid. For a deeper dive into why this matters, check out this breakdown from Investopedia.

Tracking Side Hustle Income

If you’ve cut your expenses to the bone and still need more breathing room, increasing your income is the next logical step. Many people start side hustles, like freelance writing or building niche websites. Treat your side hustle just like your budget planner—track the metrics that matter. For example, if you run a blog, understanding your site’s authority is crucial for ad revenue. Read up on Domain Authority Score Explained: How DA Impacts Your SEO Rankings & Website Growth to see how tracking digital metrics mirrors tracking financial ones.

💡 Pro Tip

Schedule a “Financial Date Night” once a month. Order a pizza, pour a drink, and sit down with your partner (or just yourself) to review your budget planner. Celebrate the wins. Did you pay off a credit card? Awesome. Acknowledge it. Positive reinforcement makes the habit stick.

Common Budgeting Traps to Avoid

Even with the best intentions, people fall into predictable traps. Avoid these, and your budget planner will serve you for years.

- Forgetting the “Miscellaneous” Category: You cannot predict everything. A parking ticket. A last-minute birthday gift. Always keep a $50 to $100 buffer in your planner for random life events.

- Setting It and Forgetting It: A budget is a living document. If your rent goes up, or you finally get that promotion, your budget planner must be updated immediately to reflect your new reality.

- Being Too Restrictive: I’ve said it before, but it bears repeating. If you cut out all your “fun money,” you will eventually binge-spend. It’s exactly like a crash diet. Give yourself a realistic allowance for things you enjoy.

⚠️ Watch Out

Do not hide purchases from your spouse or partner. “Financial infidelity” destroys trust and completely ruins the effectiveness of a shared budget planner. Total transparency is required for this to work.

Conclusion

Using a budget planner is hands down one of the highest-ROI habits you can build. It takes the abstract, stressful concept of “money management” and turns it into a concrete, actionable daily plan. By choosing a tool that fits your personality, setting realistic targets, and reviewing your progress regularly, you take the steering wheel of your economic future.

Remember, the ultimate goal of a budget planner isn’t to restrict your life. It’s to fund your dreams. Grab a notebook, download an app, or open a spreadsheet today. Map out your next month. Your future self will thank you.

❓ Frequently Asked Questions

How often should I update my budget planner?

You should log your variable expenses (like groceries and gas) at least once a week to prevent overspending. A full review and setup for the upcoming month should happen a few days before the new month begins.

What is the best budget planner for absolute beginners?

A simple pen-and-paper notebook or a basic spreadsheet is usually best for beginners. Manually entering the numbers forces you to confront your spending habits head-on before you move to automated apps.

Can a budget planner actually help me get out of debt?

Absolutely. A budget planner acts like a spotlight, revealing “extra” money that is currently leaking out through impulse buys. You can then redirect those found funds toward aggressive debt repayment strategies like the debt snowball.

What should I do if I overspend my budget in one category?

Don’t panic, and definitely don’t quit. Just move money from another category to cover the deficit. If you overspent on dining out, reduce your clothing or entertainment budget for the rest of the month to balance the bottom line.

Should I include my spouse in my budget planner?

Yes. If you share finances, you must share the budget planner. Sit down together monthly to agree on the numbers. Budgeting as a team prevents arguments and ensures you are both pulling toward the same financial goals.