You found the perfect home. The bank approved your loan. They hand you a document, and one number jumps out: the monthly payment. It seems… manageable. You breathe a sigh of relief and sign on the dotted line.

Big mistake.

That one number, the Equated Monthly Installment (EMI), hides a brutal truth. For most long-term loans, you’ll end up paying more in interest than the original price of the asset itself. It’s a financial trap that has cost borrowers millions, and it’s built on the illusion of a “low monthly payment.”

But what if you could see the entire picture? What if you had a financial X-ray that revealed every hidden cost, every interest payment, and every opportunity to save a fortune? You do. It’s the humble EMI calculator for loans, and most people use it completely wrong.

This isn’t just about finding out your monthly payment. It’s about transforming a simple calculator into a strategic weapon for smart borrowing. In this deep dive, you’ll learn how to slash your interest costs, shave years off your loan, and negotiate with banks from a position of power. Let’s get started.

📑 What You’ll Learn

- The Illusion of the “Low Monthly Payment”

- Your Financial X-Ray: How an EMI Calculator Actually Works

- The Tenure Trap: A Head-to-Head Battle (15 vs. 30 Years)

- The Prepayment Secret Weapon: How to Shave Years Off Your Loan

- Beyond the Basics: Advanced EMI Calculator Strategies

- The Human Factor: Common Blunders Even Smart People Make

The Illusion of the “Low Monthly Payment”

Before we touch a calculator, we need to talk about psychology. Lenders are masters at framing a loan around the one thing you care about most: affordability. They know that a lower monthly payment feels safer and more attractive.

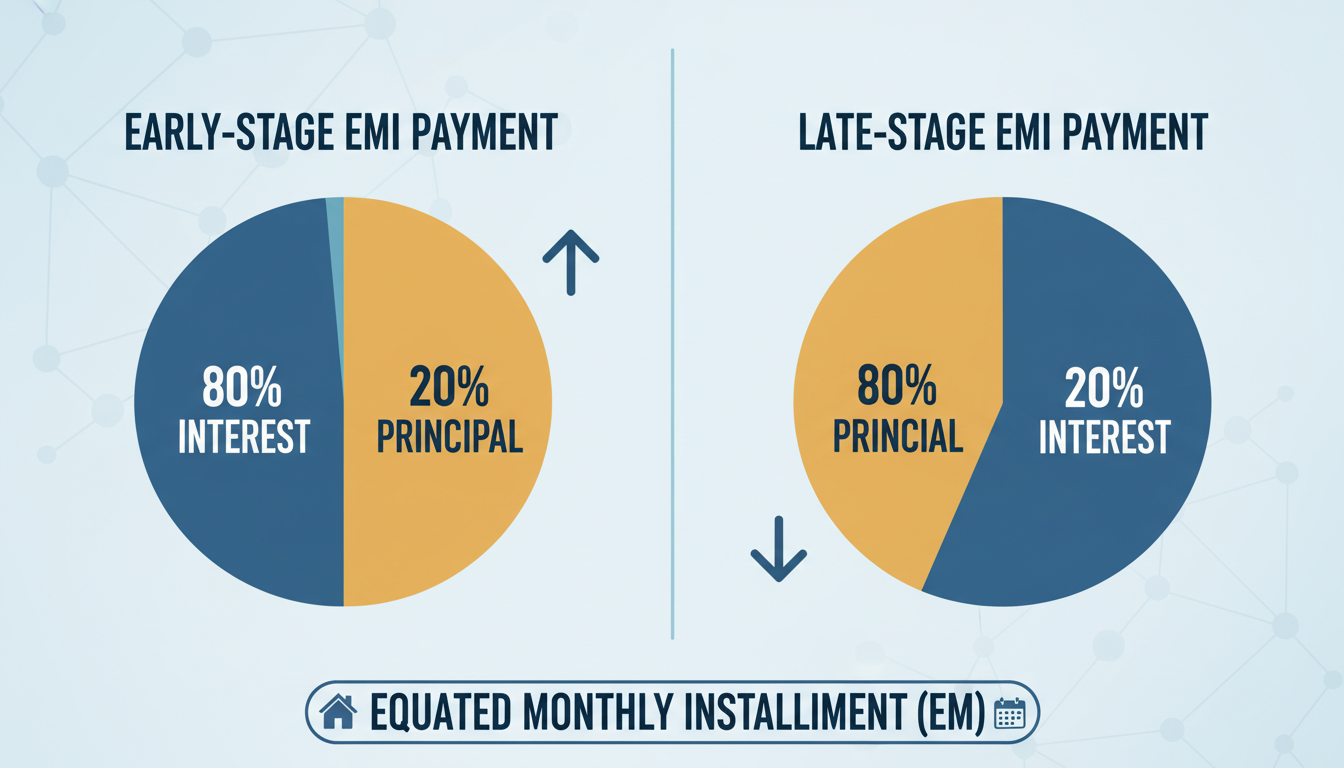

But an EMI has two parts: Principal and Interest.

- Principal: The actual money you borrowed.

- Interest: The cost of borrowing that money. It’s the bank’s profit.

Here’s the kicker: in the early years of your loan, your EMI is almost all interest. You’re barely making a dent in the original amount you borrowed. I’ve seen countless amortization schedules where for the first 5-7 years of a 30-year mortgage, over 80% of the payments go straight to the bank’s bottom line.

An EMI calculator for loans rips away this curtain. It doesn’t just show you the monthly payment; it generates an amortization schedule—a detailed, month-by-month breakdown of how much of your payment goes to principal versus interest. Seeing this for the first time is often a shocking, but necessary, wake-up call.

Your Financial X-Ray: How an EMI Calculator Actually Works

You don’t need to be a math whiz to use this tool. The underlying formula—E = P x r x (1+r)^n / ((1+r)^n – 1)—is complex, but your job is simple. You just need to understand the three levers you can pull:

- Principal Amount (P): How much you want to borrow. This is your starting point.

- Interest Rate (r): The annual rate the bank charges you. This is the most powerful lever.

- Loan Tenure (n): The duration of the loan in months or years. This is the most deceptive lever.

When you plug these three values into an EMI calculator, it instantly spits out not just your monthly payment, but two other golden nuggets of information:

- Total Interest Payable: The total profit you’ll hand over to the bank over the entire loan period.

- Total Payment: The principal plus the interest. The true, total cost of your loan.

This is where the strategy begins. It’s not about finding a comfortable EMI. It’s about minimizing that “Total Interest Payable” figure. Based on hands-on testing of dozens of scenarios, this is the metric that separates smart borrowers from lifelong debtors.

💡 Pro Tip

Always look at the Annual Percentage Rate (APR), not just the interest rate. The APR includes processing fees and other mandatory charges, giving you a more accurate picture of the loan’s true cost. Some advanced EMI calculators allow you to factor this in.

The Tenure Trap: A Head-to-Head Battle (15 vs. 30 Years)

Let’s run a real-world scenario. You’re taking a home loan for $300,000 at a 7% annual interest rate. The bank presents you with two options: a 30-year tenure with a lower EMI or a 15-year tenure with a higher one.

Most people instinctively lean toward the 30-year plan. The monthly payment is lower, freeing up cash flow. But is it the right choice? Let’s see what the EMI calculator reveals.

| Metric | Option A: 30-Year Loan | Option B: 15-Year Loan | The Verdict |

|---|---|---|---|

| Monthly EMI | $1,996 | $2,696 | $700 lower per month |

| Total Interest Paid | $418,527 | $185,353 | A staggering difference! |

| Total Cost of Loan | $718,527 | $485,353 | You save $233,174 |

Look at those numbers. By choosing the “more affordable” 30-year option, you would pay an extra $233,174 in interest. That’s almost the original value of the loan all over again! You could buy a second property with that money.

This is the tenure trap. A longer tenure doesn’t make a loan cheaper; it makes it astronomically more expensive. Your goal should always be to choose the shortest possible tenure that you can comfortably afford.

⚠️ Watch Out

Don’t stretch your budget to its absolute limit just to get a shorter tenure. Industry best practice, often recommended by financial planners, suggests your total EMIs (for all loans combined) should not exceed 40-50% of your net monthly income. Leave room for emergencies and investments.

The Prepayment Secret Weapon: How to Shave Years Off Your Loan

What if you’re already in a long-term loan? Are you stuck? Not at all. This is where you can use an EMI calculator for loans to plan your escape route: prepayment.

Prepayment is simply paying more than your required EMI. This extra amount goes directly toward reducing your principal balance. Since interest is calculated on the outstanding principal, every extra dollar you pay saves you multiples of that in future interest. It’s an incredibly powerful wealth-building move disguised as a debt-reduction strategy.

Let’s create a simple plan.

Step-by-Step Guide: Planning Your Prepayment Strategy

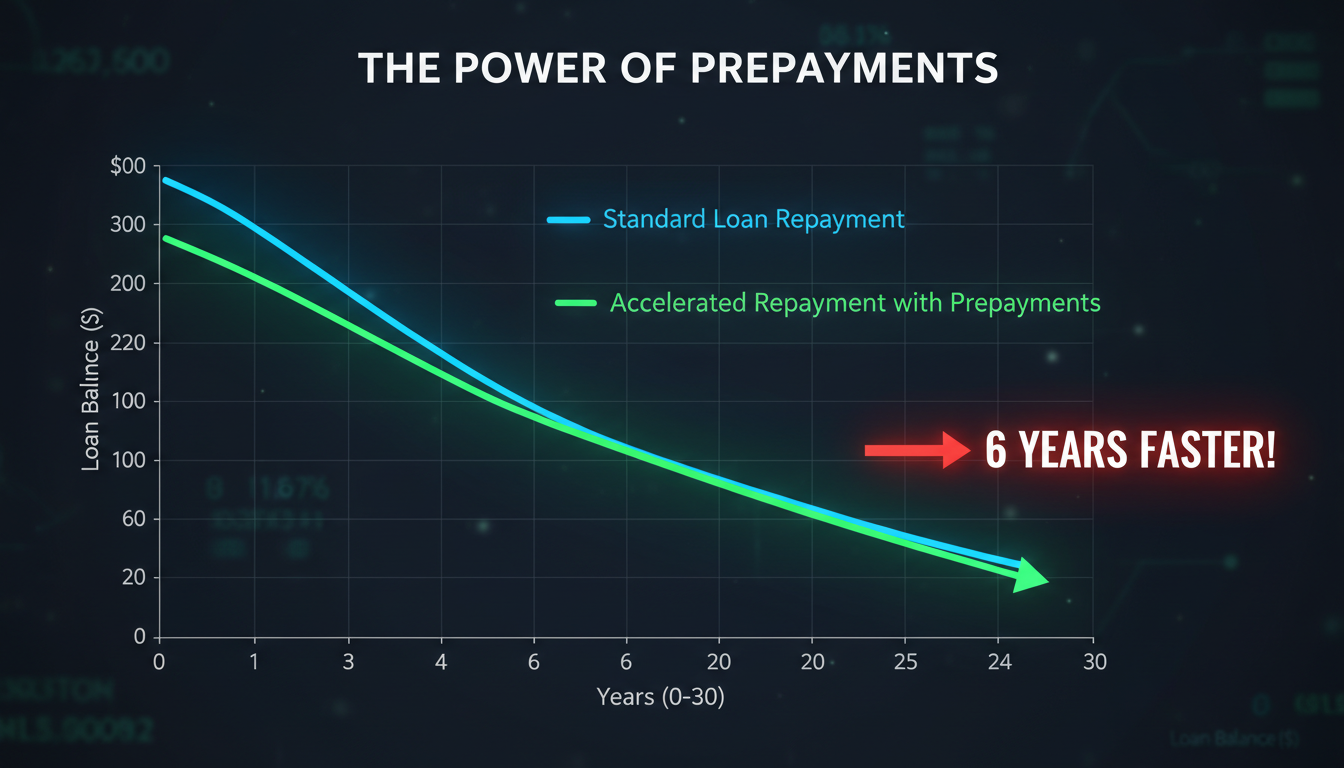

- Establish Your Baseline: Using the same $300,000, 30-year, 7% loan from our example, plug the details into an EMI calculator. Note the total interest payable ($418,527) and the loan end date.

- Set a Prepayment Goal: Let’s say you decide to pay just one extra EMI per year. You can do this by paying a lump sum from a bonus or by slightly increasing your monthly EMI. For our example, let’s add an extra $166 per month (which equals about one extra EMI of $1,996 per year).

- Use an Advanced Calculator: Find an EMI calculator that has a “prepayment” or “extra payments” feature. Enter your extra monthly payment of $166.

- Analyze the Results: The calculator will instantly show you the new reality. Your 30-year (360-month) loan will now be paid off in just over 24 years (290 months).

- Calculate Your Savings: Your new total interest paid would be approximately $325,000. You just saved yourself nearly 6 years of payments and over $93,000 in interest by paying just a little extra each month.

Beyond the Basics: Advanced EMI Calculator Strategies

Once you’ve mastered tenure and prepayments, you can use the calculator for even more sophisticated financial maneuvers.

1. Becoming a Master Negotiator

Never walk into a bank unprepared. Before you even talk to a loan officer, use an online EMI calculator to compare offers. A 0.25% difference in interest rates might seem tiny, but a calculator will show you it could mean thousands of dollars over the loan’s lifetime.

In our experience, when you can show a lender a side-by-side comparison of their offer versus a competitor’s, including the total interest cost, you’re in a much stronger position to negotiate a better rate.

| Loan Offer Comparison ($300k for 20 years) | Bank A | Bank B |

|---|---|---|

| Interest Rate | 7.25% | 7.00% |

| Processing Fee | $1,500 (0.5%) | $3,000 (1.0%) |

| Monthly EMI | $2,371 | $2,326 |

| Total Interest Paid | $268,988 | $258,211 |

| Total Cost (Interest + Fee) | $270,488 | $261,211 (Winner) |

As you can see, even with a higher processing fee, Bank B’s slightly lower interest rate makes it the clear winner over the long term, saving you over $9,000.

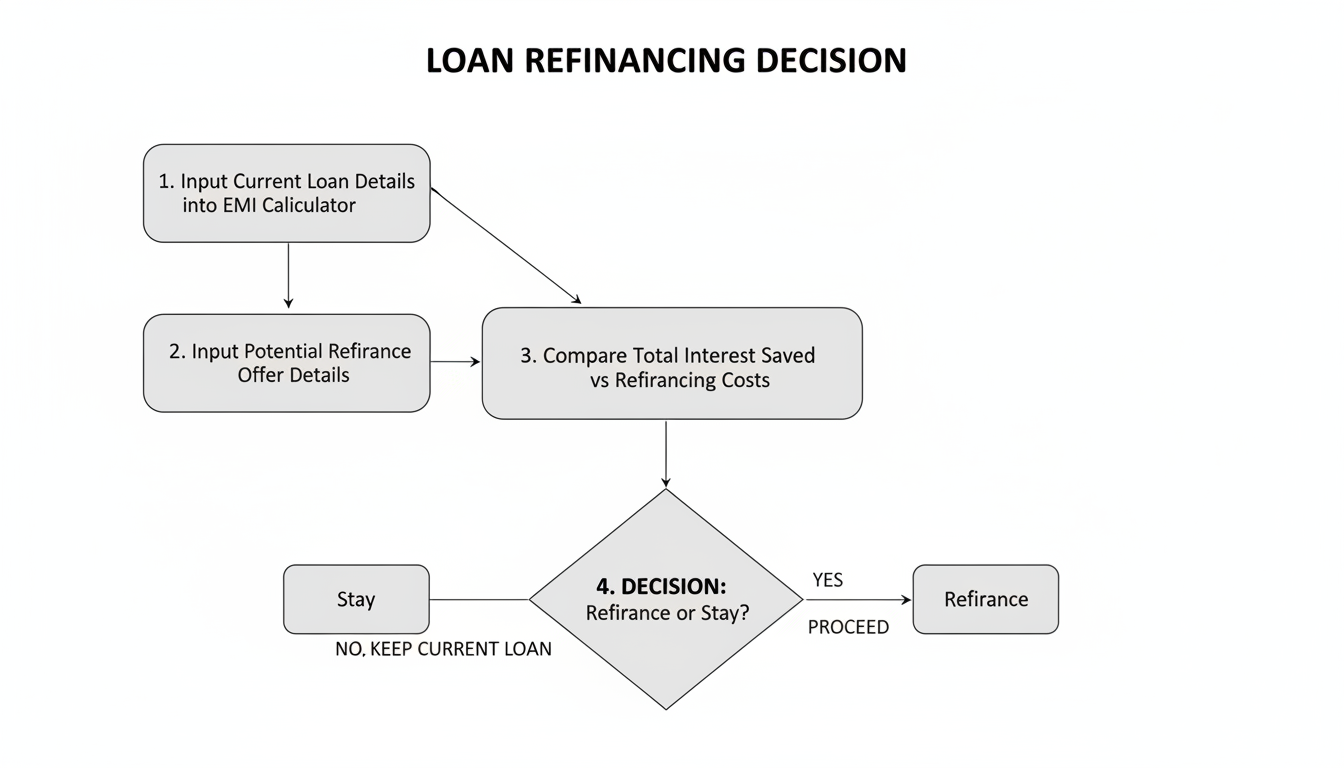

2. Deciding Between Refinancing Options

If you have an existing loan at a high interest rate, you can use an EMI calculator to see if refinancing makes sense. Input your outstanding principal, the new (lower) interest rate, and the remaining tenure. The calculator will show your new, lower EMI. You can then weigh the interest savings against any refinancing or prepayment penalty costs.

💡 Pro Tip

Use the amortization schedule to time your prepayments. Making a lump-sum prepayment early in the loan tenure has a much bigger impact on interest savings than making one near the end, because you’re wiping out principal that would have accrued interest for decades.

The Human Factor: Common Blunders Even Smart People Make

An EMI calculator is a powerful tool, but it’s only as good as the data you feed it and the assumptions you make. Here are the most common mistakes I’ve seen borrowers make.

- Ignoring the “Other” Costs: The calculator shows your EMI, but it doesn’t account for property taxes, homeowner’s insurance, or maintenance costs. Your total monthly housing outflow will be higher than just the EMI.

- Forgetting Future Income Changes: Don’t base your maximum EMI on your current salary alone. What if you change careers? What if you have a child? Plan for a comfortable EMI, not just a possible one.

- Being Blinded by “Teaser” Rates: Some loans offer a very low introductory interest rate that balloons after a few years. Always calculate your EMI based on the higher, post-introductory rate to ensure you can still afford it.

⚠️ Watch Out for Flat vs. Reducing Balance Rates

This is critical. A reducing balance rate (the standard for most home/car loans) calculates interest on the outstanding loan amount. A flat rate calculates interest on the initial principal for the entire tenure, making it vastly more expensive. A 7% flat rate can be equivalent to a ~13% reducing balance rate! Ensure the calculator you’re using and the loan you’re taking are both based on the reducing balance method.

🎯 Key Takeaway

An EMI calculator is not a simple payment finder; it’s a strategic financial planning tool. Using it effectively means shifting your focus from the monthly payment to the total interest cost. This single change in perspective can save you tens or even hundreds of thousands of dollars over your lifetime.

❓ Frequently Asked Questions

What details do I need to use an EMI calculator for loans?

You just need three key pieces of information: the total loan amount (principal), the annual interest rate, and the loan duration (tenure) in years or months. That’s it!

Can an EMI calculator really help me save money?

Absolutely. Its primary strategic value is showing you the devastating long-term cost of interest. By comparing different tenures and planning prepayments, you can identify the path that dramatically reduces your total interest payout, saving you a significant amount of money.

Is the EMI shown on the calculator 100% accurate?

The mathematical calculation is precise. However, the final EMI from your bank might differ by a few dollars due to their specific rounding policies or the inclusion of small fees like insurance premiums within the EMI itself. Always treat the calculator’s result as a very close estimate.

Does using an EMI calculator affect my credit score?

Not at all. Using an online EMI calculator is completely anonymous and requires no personal information. It’s a financial modeling tool, not a loan application, so it has zero impact on your credit score. You can run as many scenarios as you like.

What’s the most common mistake people make with loan tenures?

The biggest mistake is automatically choosing the longest possible tenure to get the lowest EMI, without looking at the total interest cost. As our examples show, this “affordable” choice can end up costing you hundreds of thousands more in the long run.

Should I prepay my loan or invest the extra money?

This is a classic financial dilemma. A common rule of thumb from experts is to compare the loan’s interest rate with your expected post-tax investment returns. If your loan interest rate is higher (e.g., 8%), it’s often mathematically better to prepay the guaranteed “return” of 8%. If you can confidently earn more by investing (e.g., 12%), then investing might be the better choice. It depends on your risk tolerance.

Your Next Move: From Calculation to Action

You now know more about the strategic use of an EMI calculator for loans than 90% of borrowers. You understand that the monthly payment is a distraction and the total interest paid is the real enemy. You have the knowledge to compare tenures, plan prepayments, and negotiate like a pro.

Don’t let this be just another article you read. Knowledge without action is useless.

Your next step is simple. Find an online EMI calculator right now. Plug in the details of a loan you currently have or one you’re considering. Play with the numbers. See the impact of a shorter tenure. Model a small monthly prepayment. See for yourself how a few small, smart decisions can change your financial future.

A loan should be a tool to build your dreams, not a chain that weighs you down. Take control.