Let’s be real for a second. You work too hard to feel this stressed about money.

We’ve all been there. You check your bank account on the 25th of the month, and your stomach drops. The math doesn’t add up. You earned good money, but somehow, it vanished into the ether of takeout coffees, subscription services, and “essential” Amazon purchases.

Here is the hard truth: Financial freedom isn’t about how much money you make; it’s about how much control you have over the money you keep.

In 2026, with inflation fluctuating and the digital economy moving faster than ever, “winging it” is no longer a viable strategy. You need a system. You need a budget planner.

But I’m not talking about a restrictive diet for your wallet that says you can never eat avocado toast again. I’m talking about a wealth-building blueprint. A good planner gives you permission to spend without guilt and the roadmap to save with purpose. In this guide, we’re going to dismantle the myths about budgeting and show you exactly how to use this tool to engineer the life you actually want.

📑 What You’ll Learn

The Psychology of Control: Why You Need a Plan

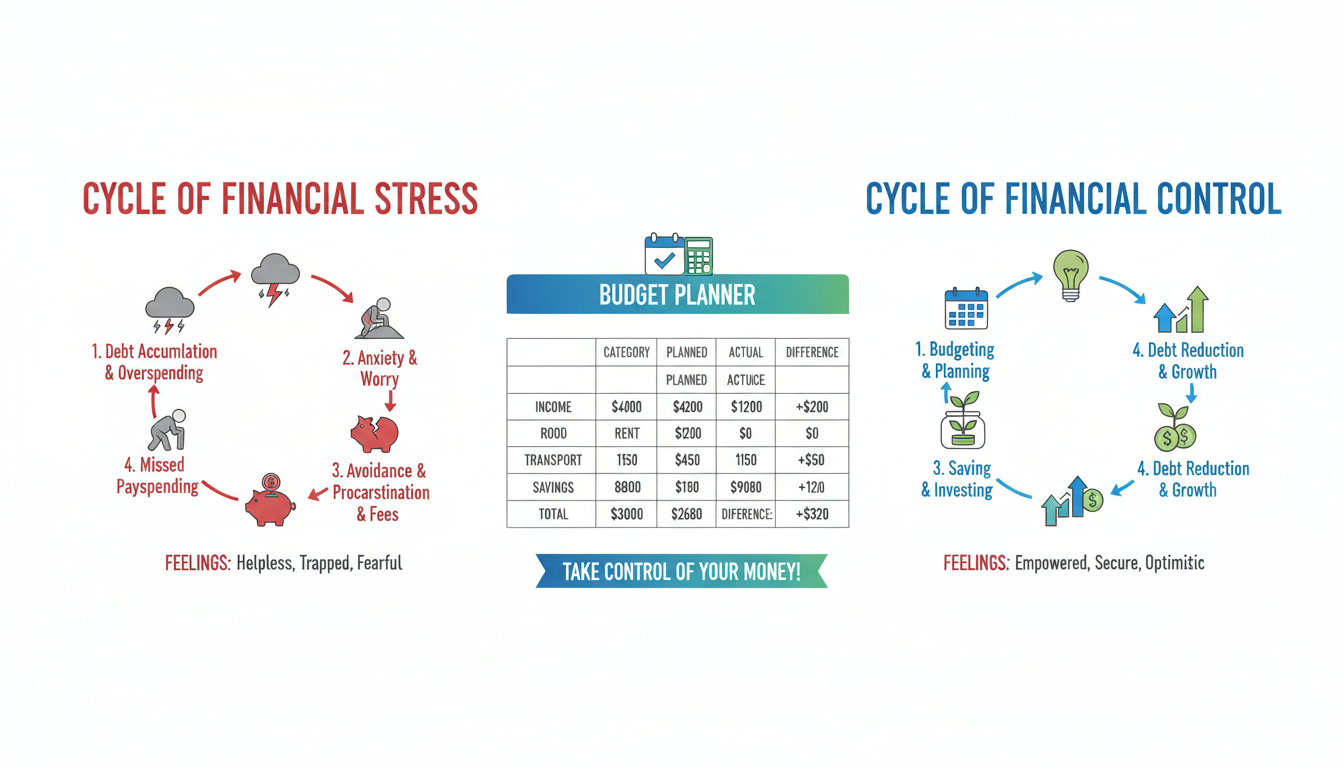

Living paycheck to paycheck is a stressful reality for millions, but the root cause often isn’t a lack of income—it’s a lack of visibility. You cannot manage what you do not measure.

In our experience working with financial strategies, we’ve seen that anxiety diminishes the moment you put numbers on paper (or a screen). A budget planner serves as your external brain. It moves your financial worries from the abstract (“I hope I can pay rent”) to the concrete (“I have $2,400 allocated for bills”).

When you use a planner, you aren’t restricting yourself. You are identifying “spending leaks”—those silent wealth killers like unused streaming subscriptions or daily convenience fees—and plugging them. This clarity allows you to prioritize what actually brings you joy.

🎯 Key Takeaway

A budget planner is not a constraint; it is a permission slip. It tells you exactly how much you can spend on the things you love, guilt-free, because you know your necessities and savings are already covered.

Digital vs. Analog: Choosing the Right Tool

The “best” planner is simply the one you will actually use. In 2026, the market is flooded with options, from AI-driven apps that predict your spending to beautiful, leather-bound journals.

If you are a tactile learner, writing numbers by hand triggers a different cognitive process that improves memory and commitment. If you are a data nerd, an automated spreadsheet might be your sanctuary. Let’s break down the pros and cons to help you decide.

| Feature | 📱 Digital Apps / Software | 📝 Physical / Paper Planner | 📊 Spreadsheet (Excel/Sheets) |

|---|---|---|---|

| Best For | Busy professionals who want automation. | Visual learners who need to “feel” the numbers. | Control freaks who love custom data. |

| Pros | Syncs with bank accounts; real-time alerts; auto-categorization. | No screen distractions; higher retention; totally customizable. | Free; powerful formulas; no data privacy concerns. |

| Cons | Subscription fees; security risks; easy to ignore notifications. | Manual math (prone to errors); no backups if lost. | High learning curve; requires manual entry. |

| 2026 Trend | AI integration for forecasting. | Minimalist, habit-tracking hybrids. | Automated bank-feed plugins. |

💡 Pro Tip

Try the Hybrid Method. Use a secure app to track your daily transactions automatically, but sit down once a week with a physical budget planner to review the totals and set goals. This gives you the convenience of tech with the intentionality of paper.

Step-by-Step: Setting Up Your 2026 Budget

Merely owning a planner won’t fix your finances any more than owning a treadmill will get you in shape. You have to do the work. Here is a battle-tested workflow to get your budget planner up and running effectively.

1. Calculate Your “True” Net Income

Start with the money that actually hits your bank account. Forget the gross salary number your HR department quotes you. Deduct taxes, insurance, and 401(k) contributions. This is your fuel. If you have a side hustle, average the last three months of income—do not use your “best month ever” as the baseline.

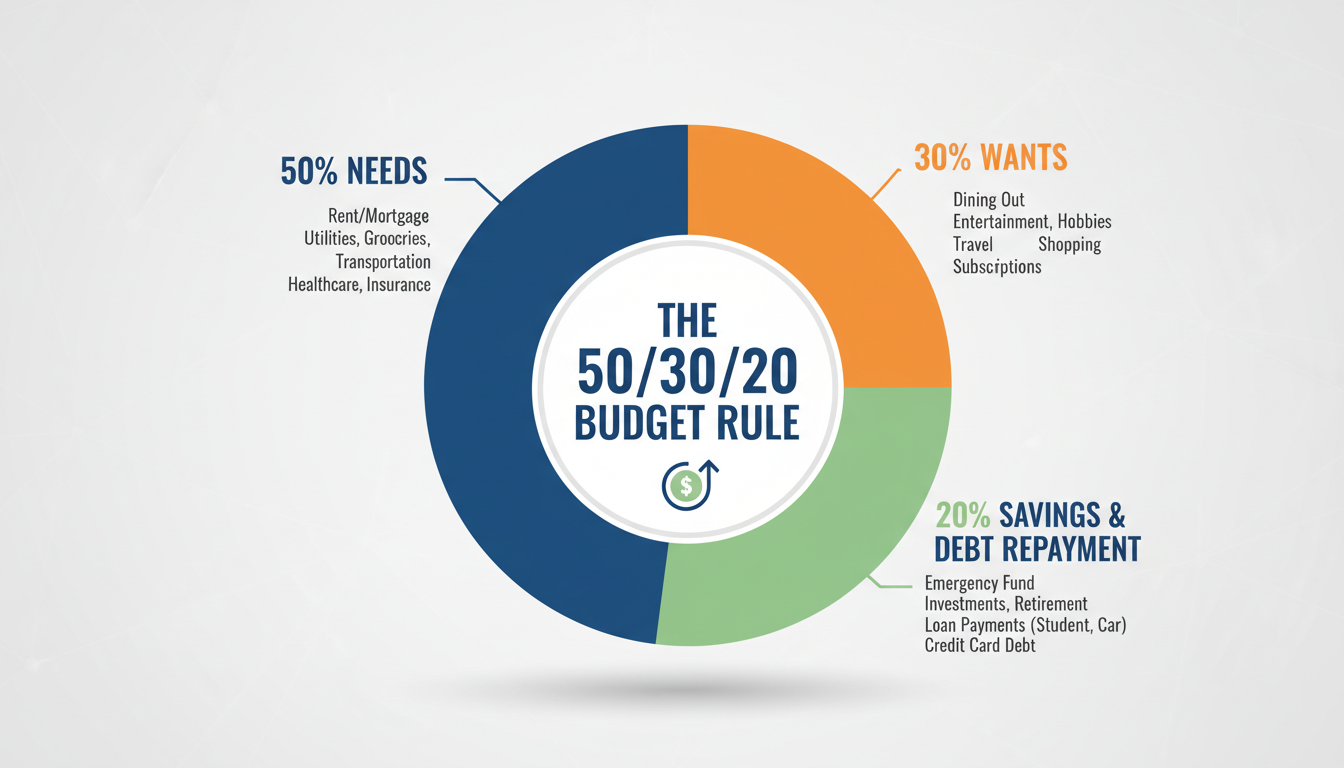

2. The 50/30/20 Audit

Before you fill in the boxes, benchmark your current spending against the classic 50/30/20 rule. This framework, popularized by Senator Elizabeth Warren, suggests:

- 50% Needs: Housing, utilities, groceries, minimum debt payments.

- 30% Wants: Dining out, hobbies, Netflix, travel.

- 20% Savings/Debt: Extra debt payments, emergency fund, investments.

According to the Consumer Financial Protection Bureau (CFPB), understanding these ratios is critical for long-term stability. If your “Needs” are at 70%, you know immediately that you have an income problem or a housing cost problem, not a latte problem.

3. Implement Zero-Based Budgeting

This is the gold standard for a budget planner. The goal is simple: Income – Expenses = $0.

Every single dollar gets a job. If you have $500 left over after bills, you don’t leave it in checking to “see what happens.” You assign it to “Emergency Fund” or “Vacation Fund.” When you give every dollar a name, you stop wondering where they went.

⚠️ Watch Out

The “Forgotten” Expenses Trap. Most budgets fail because people forget non-monthly bills. Car registration, Amazon Prime annual fees, and holiday gifts happen every year, yet they always feel like emergencies. Divide these annual costs by 12 and put that amount aside monthly.

Advanced Tactics: Sinking Funds & Automation

Once you have the basics down, it’s time to level up. A basic budget keeps the lights on; an advanced budget planner builds wealth.

The secret weapon here is the Sinking Fund. Unlike an emergency fund (which is for the unknown), a sinking fund is for the known future expenses. You are saving a little bit each month for a specific purpose.

Here is how a Sinking Fund strategy looks in a planner:

| Expense Category | Total Needed | Date Needed | Months to Save | Monthly Contribution |

|---|---|---|---|---|

| 🎄 Christmas Gifts | $800 | December 1st | 10 Months | $80 |

| 🚗 Car Tires | $600 | In 6 Months | 6 Months | $100 |

| 🐶 Vet Checkup | $200 | August | 4 Months | $50 |

| TOTAL | $230 / month |

By adding this $230 to your monthly budget, you eliminate the stress of these events. When Christmas comes, you have the cash ready. No credit cards. No hangover.

For more on the mechanics of saving, Investopedia’s guide on Zero-Based Budgeting offers a deep dive into allocating these funds precisely.

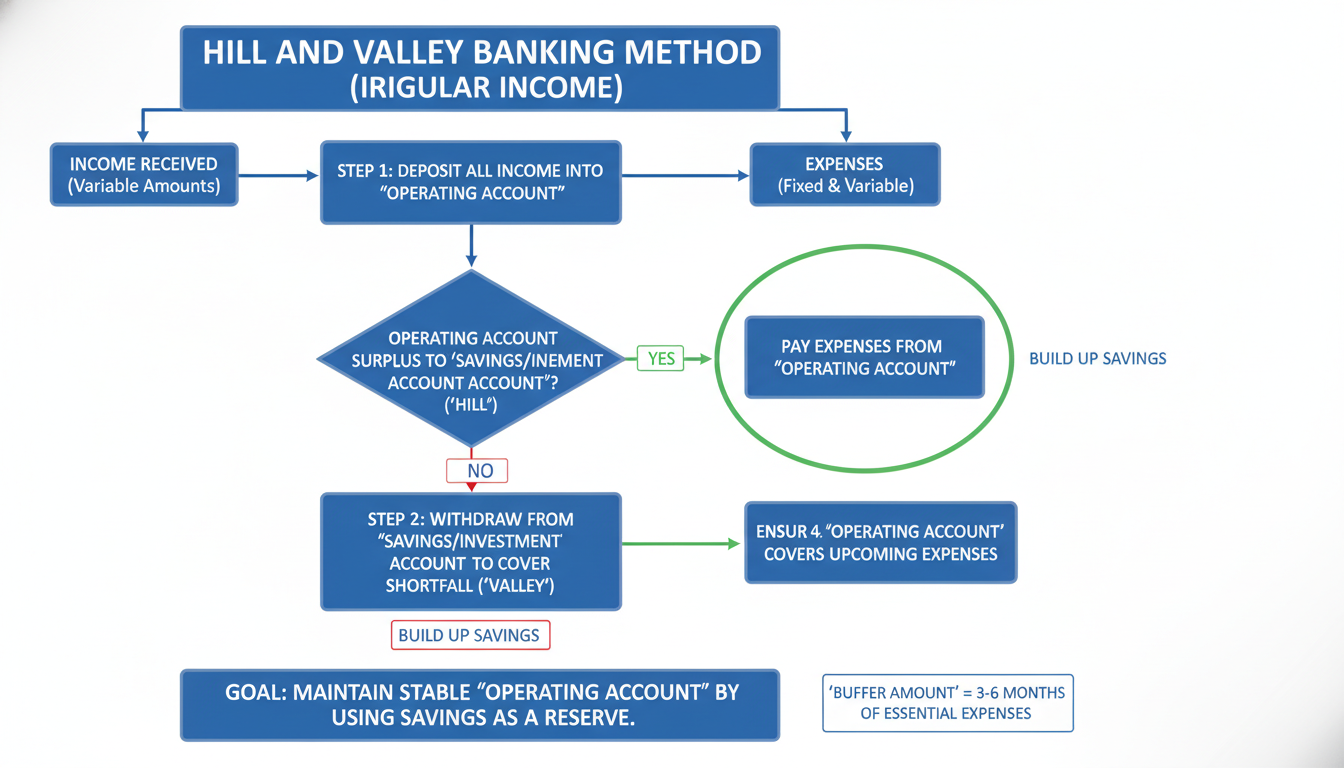

The Freelancer’s Guide to Budgeting

If you are a freelancer, gig worker, or in sales, a standard budget planner can feel impossible. One month you make $8,000; the next, you make $2,000. How do you plan?

The solution is the “Hill and Valley” Fund.

- Determine your “Bare Bones” number: What is the absolute minimum you need to survive (rent, food, lights)? Let’s say it’s $3,000.

- Budget off your worst month: Assume you will only make your lowest estimated income.

- Skim the surplus: In a month where you make $8,000, you do not spend $8,000. You spend your $3,000 baseline. The remaining $5,000 goes into a separate holding account (the Hill).

- Fill the Valleys: In a month where you only make $1,000, you pull $2,000 from that holding account to meet your baseline.

This smooths out your financial ride, turning a rollercoaster into a steady train.

Conclusion: Your Financial Future Starts Today

Using a budget planner isn’t about obsessing over pennies; it’s about designing a life you don’t need to escape from. By tracking your income, giving every dollar a job, and preparing for the future with sinking funds, you move from being a passenger to being the pilot of your financial journey.

Whether you download an app right now or head to the store to buy a notebook, the most important step is the first one. Don’t wait for the “perfect” time or the “perfect” income. Start with what you have, right now in 2026. Your future self—debt-free and financially secure—is waiting for you to make the move.

❓ Frequently Asked Questions

What is the best budget planner for beginners in 2026?

For absolute beginners, we recommend the 50/30/20 rule using a simple spreadsheet or a physical notebook. It prevents overwhelm by focusing on three broad buckets rather than forcing you to track every single penny immediately. Once you build the habit, you can move to more detailed zero-based apps.

How often should I update my budget planner?

Ideally, check your transactions weekly (we like “Money Mondays”). This ensures you catch overspending before the month is over. However, a comprehensive “Budget Meeting” with yourself or your partner should happen monthly to close out the previous month and set targets for the next one.

Can a budget planner really help me get out of debt?

Absolutely. It is the #1 tool for debt elimination. By identifying “spending leaks,” a planner frees up cash flow that you didn’t know you had. You can then redirect that found money toward debt payments using the Debt Snowball or Debt Avalanche methods.

What if I overspend my budget in a specific category?

It happens to the best of us. If you overspend on dining out, you must move money from another category (like clothing or entertainment) to cover it. This is called “rolling with the punches.” The goal is to keep the bottom line at zero, even if the individual categories shift.

Is it safe to link my bank account to a digital budget planner?

Generally, yes. Most reputable budgeting apps in 2026 use bank-level encryption (256-bit) and “read-only” access, meaning they can see your transactions but cannot move your money. Always check for Two-Factor Authentication (2FA) features before signing up.