Let’s be honest: nobody wants to pay a cent more to the IRS than they absolutely have to. But the fear of an audit—or worse, penalties—keeps most people from aggressively optimizing their tax bill. You hear horror stories about “offshore loopholes” and “creative accounting” that land people in hot water.

Here’s the thing, though. You don’t need to break the law to lower your bill. In fact, the tax code is literally written to incentivize certain behaviors by offering you a discount for doing them.

In 2026, the landscape has shifted slightly, but the core principles of wealth retention remain the same. Whether you’re a high-income earner, a freelancer, or just trying to maximize a middle-class salary, there are levers you can pull right now. I’ve spent years analyzing these frameworks, and I’m going to show you exactly how to keep more of your hard-earned money without losing sleep over an IRS letter.

📑 What You’ll Learn

1. Maximize Retirement Contributions (The “Pay Yourself First” Strategy)

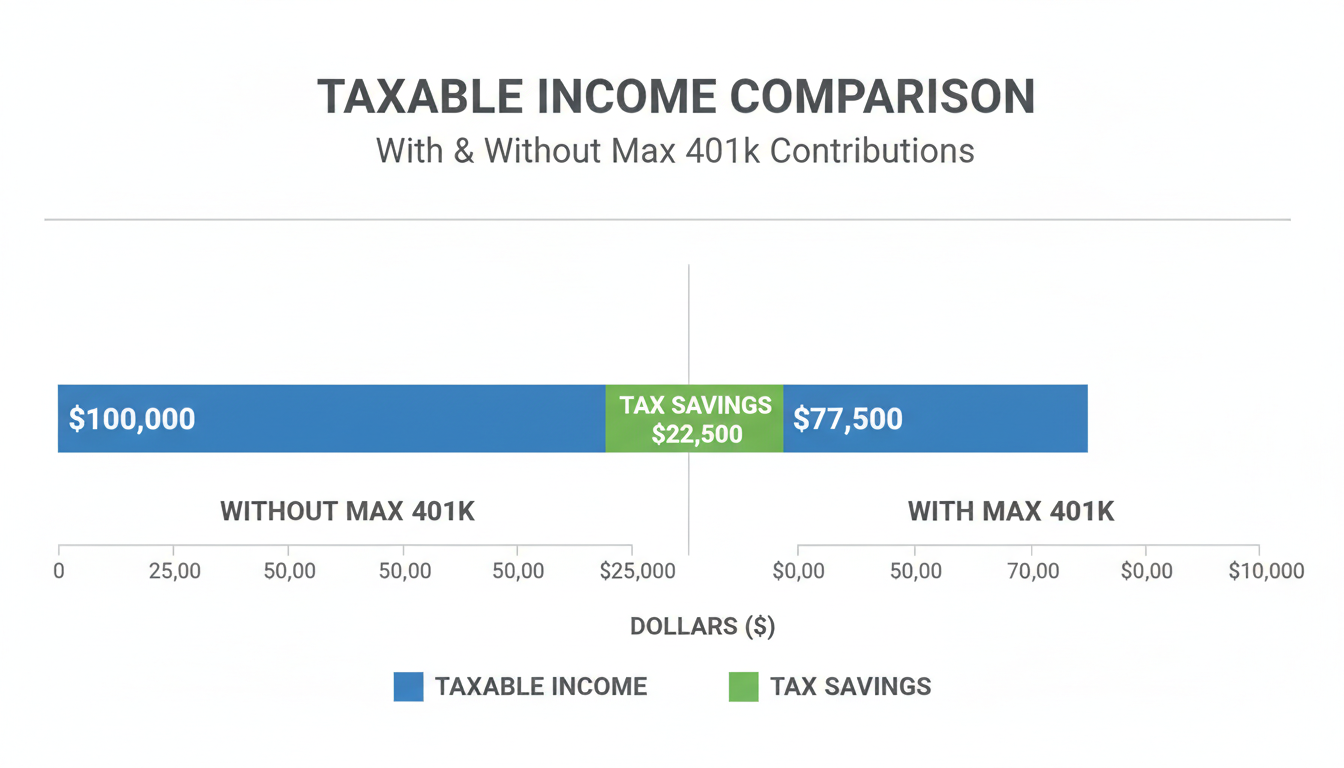

This is the cornerstone of any solid tax strategy, yet so many people leave this bucket half-full. When you contribute to a traditional 401(k) or 403(b), you are effectively lowering your salary in the eyes of the IRS. If you earn $100,000 and contribute $20,000, the IRS only taxes you on $80,000. That’s immediate savings at your highest marginal tax rate.

For 2026, contribution limits have adjusted for inflation. If you have the cash flow, hitting the maximum limit isn’t just good saving advice; it’s a massive tax shield.

💡 Pro Tip

Don’t forget the “Catch-Up.” If you are age 50 or older in 2026, you are eligible for additional catch-up contributions. This is often the difference between jumping into a lower tax bracket or staying in a higher one. Check your payroll settings today.

Don’t Ignore the Traditional IRA

If you don’t have a workplace plan, or if you want to supplement it (income limits apply), the Traditional IRA is your best friend. While the deduction phases out for high earners who also have workplace plans, for many, it’s a clean dollar-for-dollar reduction in taxable income.

2. Leverage Health Savings Accounts (The Triple-Tax Threat)

In my experience, the Health Savings Account (HSA) is the most misunderstood vehicle in the tax code. Most people treat it like a spending account. Stop doing that.

The HSA is the only account that offers a “triple tax advantage”:

- Tax-deductible contributions: Lowers your taxable income today.

- Tax-free growth: Invest the funds, and they grow without capital gains tax.

- Tax-free withdrawals: As long as it’s for qualified medical expenses.

If you can afford to pay for medical expenses out of pocket, let your HSA grow. It essentially becomes a super-charged retirement account for healthcare costs later in life.

Compare Your Tax-Advantaged Options

Understanding where to put your next dollar is crucial. Here is a breakdown of how these accounts interact with your taxes in 2026.

| Account Type | Tax Deduction (In) | Tax-Free Growth | Tax-Free Withdrawal |

|---|---|---|---|

| Traditional 401(k)/IRA | ✅ Yes | ✅ Yes (Deferred) | ❌ No (Taxed as income) |

| Roth IRA | ❌ No | ✅ Yes | ✅ Yes |

| HSA | ✅ Yes | ✅ Yes | ✅ Yes (for medical) |

3. “Bunching” Your Itemized Deductions

Since the standard deduction was nearly doubled a few years back, fewer people itemize. But if you are on the borderline, “bunching” is a sophisticated strategy that works wonders.

Instead of giving $5,000 to charity every year and taking the standard deduction every year, you “bunch” two or three years of donations into a single tax year. This pushes your itemized deductions over the standard deduction threshold for that year, yielding a massive tax break. In the “off” years, you simply take the standard deduction.

⚠️ Watch Out

Timing is everything here. You must make the payments by December 31st of the tax year. Writing the check isn’t enough; the charity needs to process it, or your credit card needs to be charged before the ball drops.

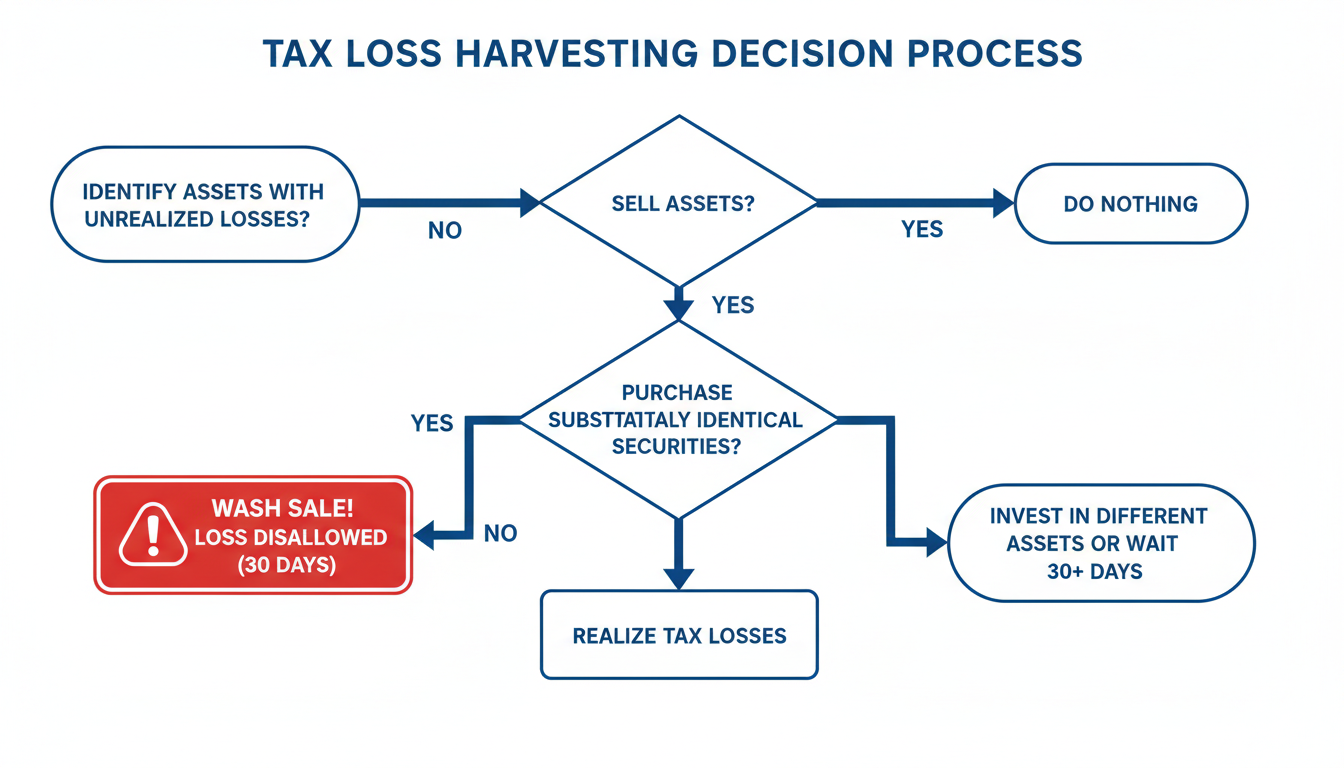

4. Take Advantage of Tax-Loss Harvesting

Markets fluctuate. It’s a fact of life. But savvy investors use the dips to lower their tax bill. Tax-loss harvesting involves selling an investment that is down to realize a loss. You can use that loss to offset any capital gains you realized that year.

Even better? If your losses exceed your gains, you can use up to $3,000 of the excess loss to offset your ordinary income (like your salary). The rest carries forward to future years indefinitely.

The Wash Sale Rule

You have to be careful here. You cannot sell a stock at a loss and buy a “substantially identical” stock within 30 days before or after the sale. If you do, the IRS disallows the loss. To stay safe, swap an individual stock for a broad ETF, or switch between ETFs that track different indexes (e.g., switch from an S&P 500 fund to a Total Market fund).

5. Optimize Business Deductions (For Freelancers & Owners)

If you have any self-employment income—even from a side hustle—you open the door to “above the line” deductions that W-2 employees can only dream of.

The Home Office Deduction

Working from the couch doesn’t count. But if you have a dedicated space used exclusively for business, you can deduct a portion of your rent/mortgage, utilities, and insurance. The simplified method allows for $5 per square foot (up to 300 sq ft), which is audit-proof and easy to claim.

Section 179 Expensing

Need a new laptop, camera, or even a work vehicle? Under Section 179, you can often deduct the entire purchase price in the year you buy it, rather than depreciating it over 5 years. For 2026, the limits are generous, designed to encourage businesses to invest in themselves.

6. Utilize Education & Dependent Care Benefits

Kids are expensive, but the tax code offers some relief. If you are paying for college, the American Opportunity Tax Credit (AOTC) is the gold standard. It offers a credit (dollar-for-dollar tax reduction) of up to $2,500 per student for the first four years of college.

According to the IRS guidelines, this credit is partially refundable, meaning you could get money back even if you owe zero taxes.

529 Plans

While federal taxes don’t offer a deduction for 529 contributions, over 30 states do. Check your specific state’s rules. If you live in a state like New York or Indiana, contributing to a 529 is a no-brainer for the state tax savings alone.

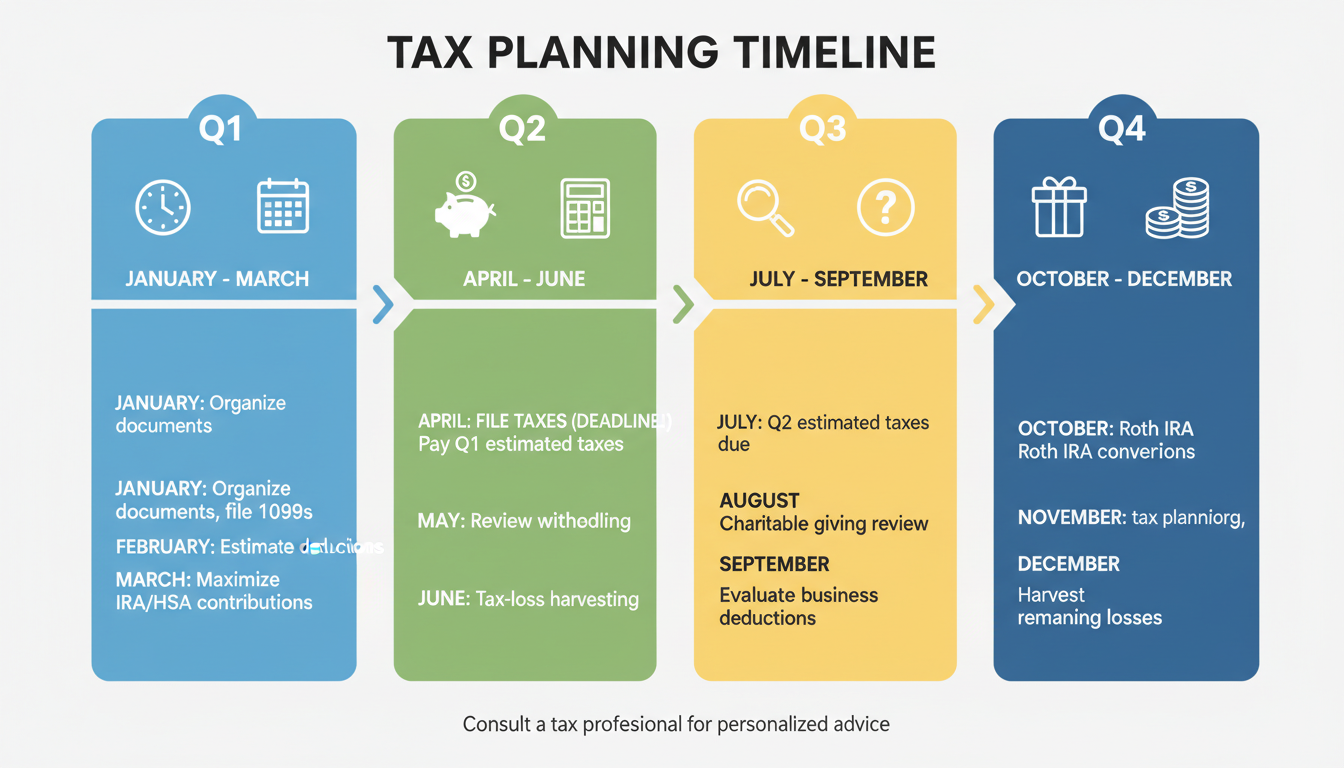

7. Step-by-Step: The Year-End Tax Sweep

Don’t wait until April 14th. Follow this workflow in Q4 of 2026 to ensure you aren’t leaving money on the table.

- Review Pay Stubs: Check your year-to-date 401(k) contributions. Can you bump up the percentage for the last few paychecks to hit the max?

- Harvest Losses: Log into your brokerage account. Look for positions in the red. Sell them to offset gains, then immediately buy a similar (but not identical) asset to stay invested.

- Spend FSA Funds: Unlike HSAs, Flexible Spending Accounts (FSAs) are “use it or lose it.” Schedule those dental appointments or buy new glasses before December 31st.

- Prepay Expenses: If you itemize, pay your January mortgage payment or property tax bill in December to claim the deduction this year.

- Gather Receipts: Digitalize your business receipts now. I recommend tools like Expensify or QuickBooks to ensure nothing gets lost.

🎯 Key Takeaway

Legitimate tax saving isn’t about finding a secret loophole; it’s about organization and timing. By maximizing retirement accounts, utilizing HSAs, and harvesting investment losses, you can legally reduce your taxable income by thousands of dollars. The most expensive tax mistake you can make is simply not paying attention.

❓ Frequently Asked Questions

Is tax-loss harvesting worth it for small portfolios?

Yes. Even if you only harvest $500 in losses, that’s savings in your pocket. Plus, it builds the habit of tax-efficient investing. Just be mindful of trading fees, though most modern brokerages offer zero-commission trades.

Can I contribute to both a 401(k) and an IRA in 2026?

Absolutely. You can contribute to both, provided you have the earned income to cover it. However, your ability to deduct the Traditional IRA contribution may be limited if your income exceeds certain IRS thresholds while you are covered by a workplace plan.

What is the difference between tax avoidance and tax evasion?

Tax avoidance is using legal methods (like the ones in this article) to minimize your tax liability. Tax evasion is illegal—it involves hiding income or lying about expenses. As the Tax Foundation notes, avoidance is smart financial planning; evasion is a felony.

Does the “Standard Deduction” change every year?

Yes, the IRS adjusts the standard deduction annually for inflation. For 2026, these adjustments ensure that inflation doesn’t secretly push you into a higher tax situation effectively. Always check the current year’s specific numbers before filing.

Final Thoughts: Be Proactive, Not Reactive

The tax code is complex, but it’s not impenetrable. The strategies outlined above—from maximizing HSAs to strategic deduction bunching—are powerful tools available to almost everyone. They don’t require offshore accounts or shady lawyers; they just require a bit of foresight.

Start with one or two of these tips. Maybe this week you increase your 401(k) contribution by 1%. Next month, you look into tax-loss harvesting. Small moves add up to massive compounding wealth over time. For more detailed definitions on investment terms, Investopedia is an excellent resource to keep bookmarked.

Take control of your financial future. The IRS is waiting for your check, but there’s no reason to make it larger than the law requires.