If I offered you a choice between receiving $1 million right now or a single penny that doubles in value every day for 30 days, which would you take?

Most people, driven by human instinct, grab the million. It feels safe. It feels huge. But it’s the wrong choice.

That humble penny? By day 30, it grows to over $5.3 million. This is the power of compounding. It’s not magic; it’s math. But it’s math that feels like magic when it starts working in your favor.

Here’s the thing: our brains aren’t wired to understand exponential growth intuitively. We think in straight lines—1, 2, 3, 4. Compound interest moves in curves—2, 4, 8, 16. That’s why a compound interest calculator isn’t just a convenient widget; it is the single most important tool in your financial arsenal. It bridges the gap between what you think will happen and what actually happens over time.

In this guide, we aren’t just going to plug numbers into boxes. We’re going to look at how to wield this tool to map out a path to financial independence, avoid the inflation trap, and understand the mechanics behind the wealth.

📑 What You’ll Learn

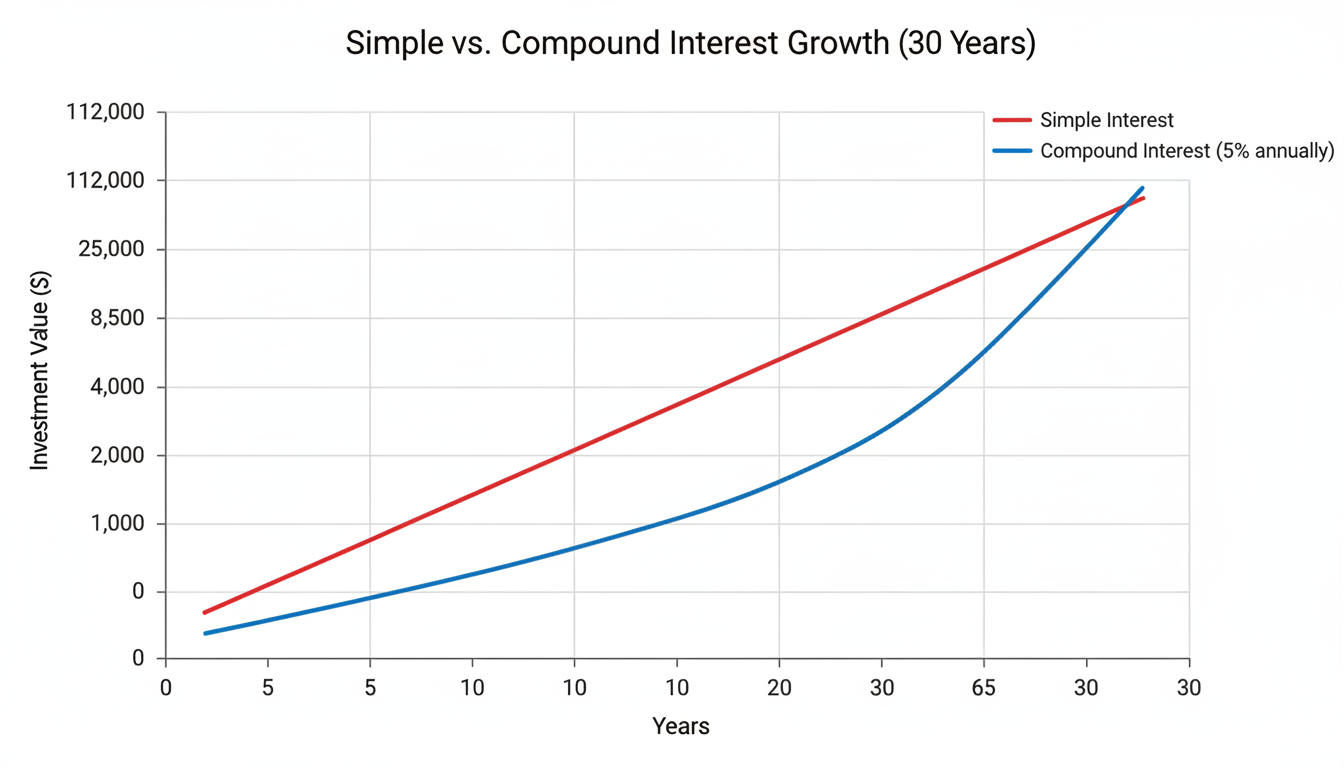

The Mechanics: Simple vs. Compound Interest

To truly respect the numbers a compound interest calculator spits out, you have to understand the engine under the hood. In my experience working with financial data, the biggest mistake people make is confusing “yield” with “interest.”

Simple interest is calculated only on your principal (the original money you put in). If you invest $10,000 at 5% simple interest, you get $500 this year. Next year? Another $500. Ten years from now? Still $500. It’s flat. It’s boring.

Compound interest is interest on interest. It’s the snowball rolling down the hill.

In year one, you earn that same $500. But in year two, you earn 5% on $10,500 (your principal + last year’s earnings). That’s $525. By year 30, that annual payment has grown massively, not because you added more money, but because your money had babies, and those babies had babies.

Why Your Brain Needs This Tool

Financial planning without a projection tool is like trying to drive across the country without a GPS. You might head generally west, but you’ll likely get lost.

A compound interest calculator serves as your navigational system. It removes the emotional guesswork. When markets dip, or when saving feels pointless because the numbers seem small, the calculator shows you the long-term vision. It proves that the first $100,000 is the hardest, but the next $100,000 happens almost on autopilot.

🎯 Key Takeaway

Time is more powerful than the amount of money you invest. A compound interest calculator visually proves that starting small today is mathematically superior to starting “big” ten years from now.

Step-by-Step: Using the Calculator Correctly

Using these tools seems intuitive, but garbage in equals garbage out. If you input unrealistic expectations, your retirement plan will fail. Here is how to use a compound interest calculator like a pro.

- Determine Your Principal: This is your starting lump sum. Be honest—what can you invest today?

- Set a Realistic Contribution: How much can you add monthly? Consistency beats intensity here.

- Choose a Conservative Rate: This is where people mess up. The S&P 500 has historically returned about 10% annually. However, for planning purposes, I always recommend using 7% or 8% to account for inflation and bad years.

- Select Frequency: How often is interest added? (More on this below).

- Run the Numbers: Look at the total at the end of the term.

💡 Pro Tip

Don’t just run the calculation once. Run three scenarios: a “Bear Case” (5% return), a “Base Case” (7% return), and a “Bull Case” (9% return). This gives you a realistic range of outcomes rather than a single number that might not happen.

Real-World Scenarios: The Cost of Waiting

Let’s look at the data. I’ve put together a comparison to show you exactly why “I’ll start investing later” is the most expensive sentence in the English language.

We are comparing two investors: Sarah (starts at 25) and Mike (starts at 35). Both want to retire at 65. Both earn an 8% annual return.

| Variable | Sarah (The Early Bird) | Mike (The Procrastinator) |

|---|---|---|

| Starting Age | 25 | 35 |

| Monthly Investment | $500 | $500 |

| Years Invested | 40 | 30 |

| Total Cash Invested | $240,000 | $180,000 |

| Final Portfolio Value | $1,745,500 | $745,000 |

| Cost of Waiting | – | $1,000,500 Lost |

Look at that table again. Mike only invested $60,000 less than Sarah, but he ended up with $1 million less in his account. That is the penalty of ignoring the time variable in the compound interest formula.

The Hidden Variable: Compounding Frequency

One setting on the compound interest calculator that often confuses users is “Compounding Frequency.” Does it really matter if interest is calculated daily, monthly, or yearly?

Short answer: Yes.

The more frequently interest is added to your principal, the faster your money grows. A savings account usually compounds monthly. The stock market doesn’t technically “compound” in a fixed schedule, but reinvesting dividends quarterly mimics this effect.

Here is how a $10,000 investment at 8% over 20 years changes based on frequency:

| Frequency | Final Amount | Difference |

|---|---|---|

| Annually | $46,609 | Baseline |

| Semi-Annually | $48,010 | +$1,401 |

| Monthly | $49,268 | +$2,659 |

| Daily | $49,521 | +$2,912 |

⚠️ Watch Out

While daily compounding is great for savings, be careful with debt. Credit cards often use daily compounding (average daily balance), which is why your debt balance seems to grow so aggressively even when you stop spending.

3 Strategies to Supercharge Results

Once you’ve run your numbers through the calculator, you might feel discouraged. Maybe the number isn’t as high as you wanted. Don’t panic. You have levers you can pull to change the outcome.

1. The “1% Lift” Strategy

You don’t need to double your savings overnight. Try increasing your contribution rate by just 1% every year. If you get a raise, bank it. If you have a side hustle—perhaps you’re tracking growth with a YouTube channel statistics finder—funnel 100% of that “extra” money into your investment account. The calculator will show you that these small bumps have massive downstream effects.

2. Reinvest Everything

If you buy dividend stocks or hold bonds, you will receive cash payouts. It is tempting to spend that cash. Don’t. Set your account to DRIP (Dividend Reinvestment Plan). This automates the compounding process.

3. Audit Your Debt

Compounding works both ways. If you are paying 20% interest on a credit card while earning 8% in the market, you are losing wealth. Use a personal loan EMI calculator comparison to see if consolidating high-interest debt can lower your rate, freeing up more cash to put into the “good” side of the compound interest equation.

The Math Behind the Magic

For those who want to check the calculator’s work, here is the standard formula used by financial institutions and the SEC:

A = P (1 + r/n)^(nt)

- A: The future value (what you end up with).

- P: The Principal (what you start with).

- r: The annual interest rate (as a decimal, so 7% is 0.07).

- n: The number of times interest compounds per year.

- t: The time in years.

Notice that “t” (time) is in the exponent. In math, exponents are powerful. This is why adding 5 years to your investment timeline is often more effective than adding $5,000 to your principal.

Conclusion: Start Your Clock Today

Building wealth isn’t about hitting a home run on a lucky stock pick. It’s about discipline, time, and understanding the math. A compound interest calculator gives you the roadmap, but you have to drive the car.

If you play around with the numbers and realize you’re behind on your goals, don’t get discouraged. Use that data as a wake-up call. Increase your contributions by $50 this month. Wait an extra year to buy that new car. The beauty of compounding is that it rewards patience heavily. The best time to plant a tree was 20 years ago; the second-best time is today. Run your numbers, set your plan, and let the math make you wealthy.

❓ Frequently Asked Questions

Does the compound interest calculator account for inflation?

Most basic calculators do not. They show you the “nominal” value of your money. To see the “real” purchasing power, you should subtract the expected inflation rate (historically 2-3%) from your expected return rate. If you expect an 8% return, input 5% or 6% to see what that money will actually buy you in the future.

What is a realistic interest rate to use?

If you are investing in a diversified stock portfolio (like the S&P 500), historical averages hover around 10% before inflation. However, to be safe and build a robust plan, we recommend using 7% or 8%. If you are calculating for a high-yield savings account, check current bank rates, which fluctuate with the Federal Reserve rate.

What is the Rule of 72?

The Rule of 72 is a mental shortcut to estimate compound interest without a calculator. Divide 72 by your interest rate to see how many years it takes to double your money. For example, at a 9% return, your money doubles every 8 years (72 ÷ 9 = 8).

Should I focus on paying debt or investing?

Compare the interest rates. If your debt interest rate (e.g., credit card at 19%) is higher than your expected investment return (e.g., market at 8%), the math says pay the debt first. It’s a guaranteed “return” of 19%.