The introduction of the Goods and Services Tax (GST) in India marked one of the most significant indirect tax reforms in the nation’s history. Far from being a simple tax rate change, GST fundamentally restructured the entire supply chain, impacting everything from sourcing raw materials to final consumer pricing. For businesses operating in India, mastering their pricing strategy post-GST implementation is crucial for survival and growth. This comprehensive guide details exactly how GST affects business pricing strategy India, providing actionable insights for maintaining competitive advantage and profitability.

Understanding the nuances of the tax structure—especially the mechanism of Input Tax Credit (ITC)—is the first step. Within the first 100 words, it is clear that navigating how GST affects business pricing strategy India requires a deep dive into cost components, supply chain efficiency, and competitive landscape analysis.

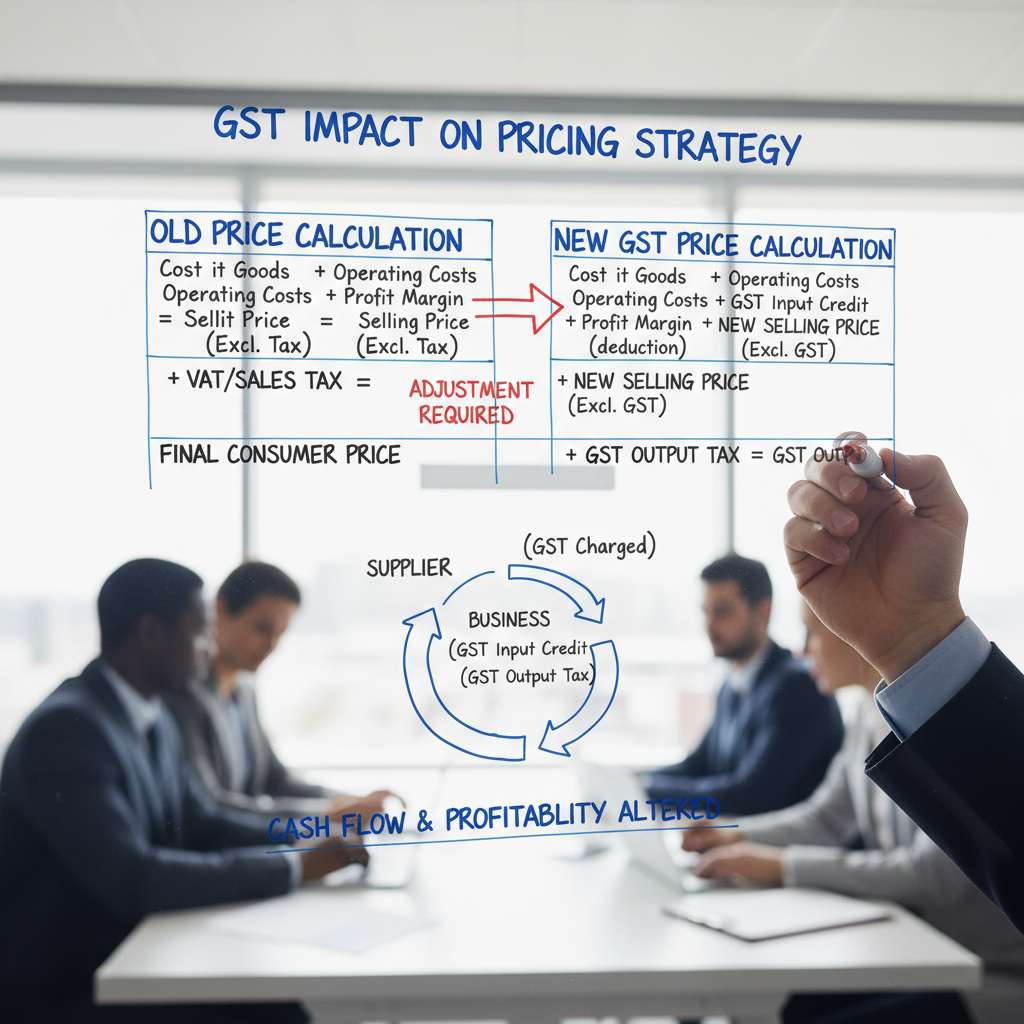

The Core Mechanism: How GST Affects Business Pricing Strategy India through ITC

Before GST, the cascading effect of taxes (tax on tax) was a major headache, inflating final consumer prices unnecessarily. Taxes like VAT, Excise Duty, and Service Tax were levied separately, and credits often couldn’t be seamlessly transferred across different stages of production or state lines. GST eliminated this.

The single most important factor determining how GST affects business pricing strategy India is the availability of the Input Tax Credit (ITC). ITC allows businesses to claim credit for the GST paid on the purchase of goods or services used in the course or furtherance of business.

Calculating the Effective Cost Reduction via ITC

When a business purchases inputs, they pay GST. When they sell the final product, they charge GST. They only remit the difference (Output Tax – Input Tax Credit) to the government. This mechanism significantly reduces the effective tax burden on the business, leading to two primary strategic opportunities:

- Reducing Prices: Passing the tax savings (from reduced cascading effects) onto the consumer to gain a competitive edge.

- Increasing Margins: Maintaining the existing price point (if competitive pressures allow) and retaining the tax savings as higher profit margins.

For example, a manufacturer whose inputs were previously taxed at 10% (non-creditable) and output at 18% (total tax burden 28%) might now face a uniform 18% GST rate where the input tax is fully creditable. This reduction in the non-creditable tax component directly lowers the operational cost basis.

Pre-GST Cost Structure

Taxes were levied at multiple stages (Excise, VAT, CST). Limited cross-state credit availability led to tax cascading. Logistics costs were higher due to state border checks.

Post-GST Cost Structure

Single tax structure (CGST + SGST/IGST). Full ITC availability eliminates cascading. Efficient supply chain due to streamlined movement, potentially reducing warehousing needs.

Impact on Final Price

The net tax liability often decreases, offering scope for price rationalization or margin improvement, depending on the specific product’s rate and historical tax structure.

Analyzing Cost Components: Understanding how gst affects business pricing strategy india

Pricing is not just about tax rates; it involves analyzing every cost component that feeds into the final selling price. GST has altered three major business costs:

1. Procurement and Input Costs

The GST rate applied to your raw materials and services purchased dictates the ITC available. Businesses must meticulously track the HSN/SAC codes of all inputs to ensure they are claiming the correct credit. If a business deals with non-GST goods (like alcohol or petroleum products), the inability to claim ITC on related inputs will increase the cost base for those specific products.

2. Logistics and Supply Chain Efficiency

The removal of state barriers and the introduction of the e-way bill system have significantly streamlined inter-state movement. This has allowed businesses to consolidate warehouses and optimize their supply chain. Fewer, larger warehouses mean lower rental, staffing, and compliance costs. These operational savings must be factored into the pricing strategy.

“Effective supply chain rationalization under GST often yields cost savings far greater than the direct tax rate changes alone. These savings are critical inputs when determining competitive pricing.”

3. Compliance and Administrative Costs

While GST simplified the tax structure, it increased the frequency and complexity of compliance, particularly for smaller businesses. Monthly or quarterly returns (GSTR-1, GSTR-3B), reconciliation, and adherence to e-invoicing norms require investment in software, training, and specialized accounting staff. These administrative overheads are indirect costs that must be considered when setting prices, especially when analyzing how GST affects business pricing strategy India in the long run.

To ensure accurate calculations, especially when dealing with complex multi-rate inputs, businesses often rely on specialized tools. Using a GST Calculator helps quickly determine the tax component and the net price, ensuring transparency and accuracy in quoting rates to B2B clients or consumers.

Strategic Pricing Adjustments: Competitive Positioning and Profitability

Once the internal cost structure is optimized and the impact of ITC is understood, the next challenge is positioning the product or service competitively in the market. Simply reducing prices might not be the best strategy if competitors are already operating on very thin margins, or if the market expects a higher value proposition.

Maintaining Profitability while Addressing Anti-Profiteering

A key regulatory aspect of GST is the anti-profiteering clause, which mandates that any tax reduction or benefit arising from ITC must be passed on to the consumer. While the enforcement of this clause has evolved, businesses must be able to demonstrate that their pricing changes are justified by changes in their cost structure, not merely attempts to artificially inflate margins.

The decision on whether to reduce the Maximum Retail Price (MRP) or increase the profit margin depends heavily on the industry and market dynamics. Industries with high pre-GST taxes (like hospitality or construction) often saw significant rate reductions, necessitating immediate price adjustments.

The Cost-Plus Strategy

Calculate the new cost base (after factoring in full ITC and logistics savings). Add the desired margin percentage. This works well for services or custom products where costs are clearly defined.

Value-Based Pricing

Focus on the perceived value to the customer, rather than just the cost. If GST compliance allows for faster delivery or better service, the price can reflect this enhanced value.

Competitive Parity Pricing

Monitor key competitors closely. If the competition has reduced prices due to ITC benefits, your strategy must align to maintain market share. This is crucial for mass-market goods.

Differential Pricing

Analyze tax implications for different customer segments (e.g., B2B vs. B2C, or inter-state vs. intra-state). Pricing might need to be optimized based on the recipient’s ability to claim ITC.

Practical Steps for Analyzing how gst affects business pricing strategy india

Transitioning successfully requires a structured approach to analysis and execution. Here are the key steps businesses should undertake:

Step 1: Conduct a Comprehensive Tax Impact Assessment (TIA)

Map the old tax structure (Excise, VAT, Service Tax) against the new GST rates for both inputs and outputs. Quantify the exact financial impact of ITC availability. This is the foundation for determining how GST affects business pricing strategy India specifically for your sector.

Step 2: Re-evaluate Supply Chain Economics

Determine if warehouse consolidation or changes in vendor location (moving from unregistered to registered suppliers to maximize ITC) can generate additional savings. Use data analysis tools to compare costs, ensuring that the savings from logistics efficiency are accurately projected. If you are handling large volumes of data for analysis, tools that assist in data processing and conversion can be helpful, although the specifics of tax data analysis often require dedicated financial software.

Step 3: Model Multiple Pricing Scenarios

Create models that forecast profitability under different pricing strategies (e.g., 5% price reduction vs. 5% margin increase). This must account for potential volume changes based on market elasticity. For B2B sales, clarify whether the price quoted is inclusive or exclusive of GST, as the recipient will claim the credit.

Step 4: Communicate Transparently with Stakeholders

Clearly communicate any pricing changes to consumers and B2B partners. Transparency helps manage expectations and builds trust, especially regarding statutory compliance requirements like the anti-profiteering clause. The Government of India, through the Central Board of Indirect Taxes & Customs (CBIC), provides extensive resources and notifications that businesses should monitor rigorously to ensure compliance. You can find official circulars and updates on the CBIC website.

Digital Transformation and Accounting Practices

The digitization inherent in the GST framework — e-invoicing, GSTR-2A reconciliation, and digital return filing — demands robust accounting systems. Manual errors can lead to missed ITC claims, which directly inflate the cost of goods sold. Investing in reliable ERP systems or accounting software is no longer optional; it’s essential for accurate pricing.

Furthermore, businesses dealing with international trade must understand the implications of IGST on imports and exports. Exports are typically zero-rated (meaning the exporter can claim a refund of input tax paid), which significantly affects their global competitiveness and pricing structure compared to domestic sales.

The impact of GST extends beyond mere calculation; it requires a strategic overhaul of how businesses perceive value creation and cost management. By diligently analyzing ITC benefits, optimizing supply chains, and adhering to compliance standards, businesses can harness the potential of this reform to either offer more competitive prices or achieve healthier profit margins, mastering how GST affects business pricing strategy India in the dynamic Indian market.

For more detailed economic analysis on the impact of GST on various sectors and broader fiscal policy, authoritative sources like the Reserve Bank of India (RBI) often publish reports detailing macroeconomic shifts post-implementation.

FAQs

ITC reduces the tax liability on your purchases, meaning the cost of your raw materials or inputs decreases. This cost saving can either be used to lower your final selling price (making you more competitive) or retained to increase your profit margin, depending on your market strategy and competition.

While not an absolute mandate for every single transaction, the GST framework includes an anti-profiteering clause. This clause requires businesses to pass on the benefit of any reduction in the tax rate or input tax credit to the consumer through a commensurate reduction in prices. Failure to do so can lead to legal action, making price rationalization a critical compliance requirement.

The biggest challenge is accurately quantifying the cumulative impact of ITC across the entire value chain, especially when dealing with complex services or multi-stage manufacturing. Businesses often struggle to factor in indirect cost savings resulting from supply chain efficiency (like reduced logistics costs) into the final price calculation.

Businesses dealing with mixed supplies (taxable and exempt) face complexity in ITC claims. They can only claim full ITC on inputs used for taxable supplies. Inputs used for exempt supplies or for non-business purposes require proportional reversal of ITC. This increases the effective cost base of the exempt goods, requiring careful pricing adjustments for those specific products.

Yes, often. In B2B transactions, the buyer is usually registered under GST and can claim full ITC on the purchase. Therefore, the focus is on the price exclusive of GST. In B2C transactions, the consumer cannot claim ITC, so the price inclusive of GST is the critical factor. Transparency in pricing and clear communication regarding ITC benefits are essential for B2B pricing strategy.

Read Also:

- Histogram Generator

- Mastering the Meta Tag Generator: How to Create Optimized Meta Descriptions

- Minesweeper Game

- Pneumococcal Vaccine Dosage Calculator

- QR Code Generator: Boost Business Growth in 2024

- Lap Time Calculator: Find Your True Race Pace in 2026

- The Ultimate Guide to Finding Your SBI IFSC Code Search by Branch and Bank Details – Visual Story

- PAK to BIN Converter Online: The Ultimate 2026 Safety Guide

- 60 Hz to Watts: The 2026 Guide to What Really Matters

- Casetext Review 2026: 7 Features Changing Legal Practice

- Essay Title Generator: The Strategic Guide for A+ Titles in 2026

- Your 2026 Guide to Online Converter Tools

- 9 Essential Insights on Using a Watermark Remover for Flawless Images – Visual Story

- SRM CGPA Secrets 2026: Master Your Score

- Torque Conversion Calculator: The Ultimate 2026 Pro Guide

- Microgram per Liter to PPB: The 2026 Guide to 1:1 Conversion

- Trapezoid Volume Calculator: The Definitive 2026 Guide

- Viscosity Unit Conversion: The Expert Guide for 2026

- MozRank: Your 2026 SEO Secret Weapon